IMAX as a Box Office Multiplier: Understanding True Incremental Impact

Framing the Analysis

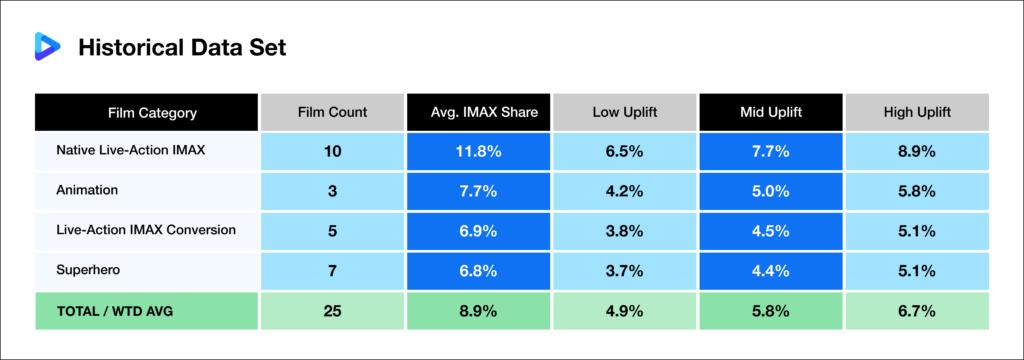

To better understand the real impact of IMAX on theatrical performance, we analyzed 25 major films from 2015 to 2025 with confirmed IMAX revenue data. These titles were grouped into four categories: Native Live-Action IMAX, Animation, Live-Action IMAX Conversion, and Superhero. The objective is to isolate how much IMAX revenue is truly incremental rather than simply shifted from standard screens.

Native vs Conversion: Why It Matters

Native IMAX films are shot using IMAX cameras and designed for premium viewing. Examples include OPPENHEIMER, SINNERS, and F1: THE MOVIE. These films consistently generate higher IMAX share and stronger incremental demand.

IMAX conversions are films shot traditionally and later optimized for IMAX screens, such as MISSION: IMPOSSIBLE – FALLOUT and JURASSIC WORLD: FALLEN KINGDOM. These benefit from IMAX exposure but typically generate lower incremental impact.

Superhero films are analyzed separately due to their scale and built-in demand, where IMAX primarily acts as a premium upsell rather than a core driver of incremental audience.

From IMAX Share to True Uplift

The core relationship used in the model is: IMAX Uplift = IMAX Share × α. IMAX share reflects the % of total box office from IMAX, while α represents the portion of IMAX demand that is truly incremental.

The α factor is derived from observed ticket price premiums and estimated admissions that would not have occurred without IMAX. This produces low, mid, and high scenarios that serve as practical forecasting ranges.

Key Distinction: Share vs True Contribution

IMAX share measures where revenue is captured, while IMAX uplift measures how much of that revenue is truly created. A film may generate 10% or more of revenue from IMAX, but only a portion of that reflects incremental audience demand rather than substitution from standard formats.

Historical Context and Benchmarks

Across the dataset, Native IMAX films average just under 12.0% IMAX share of total revenue. Superhero films average closer to 7.0%, reflecting strong baseline demand independent of format.

These benchmarks are critical for contextualizing forward-looking assumptions and identifying outliers driven by franchise strength or format-specific positioning.

Applying the Model: Dune vs Avengers

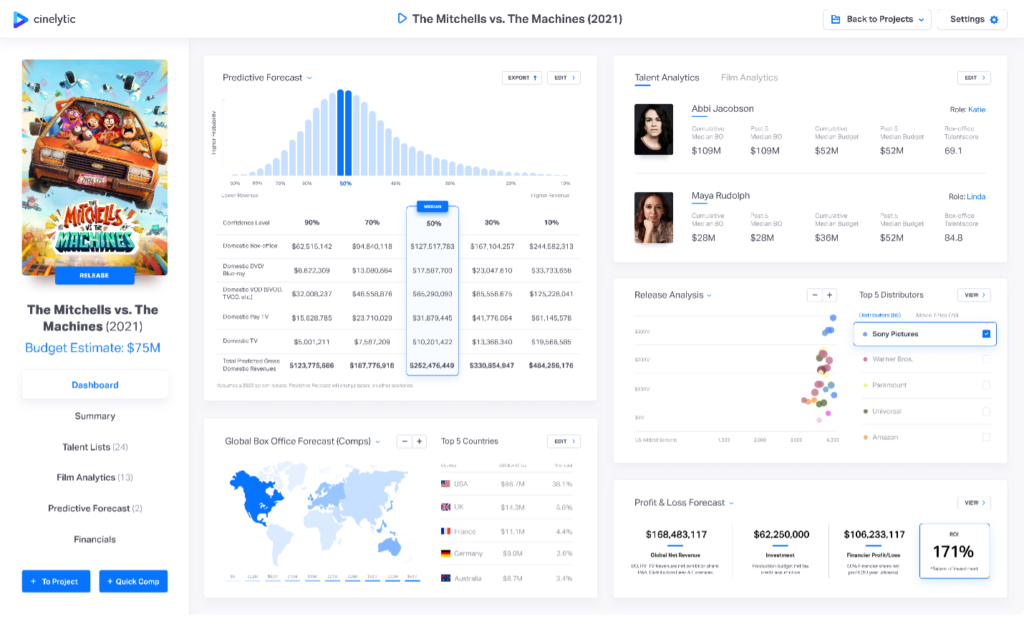

Using the Cinelytic predictive forecasting platform, we applied this framework to two major same-date releases: DUNE: PART THREE and AVENGERS: DOOMSDAY. The release timing introduces a key structural dynamic, with Denis Villeneuve’s sci-fi epic expected to secure approximately three weeks of IMAX exclusivity.

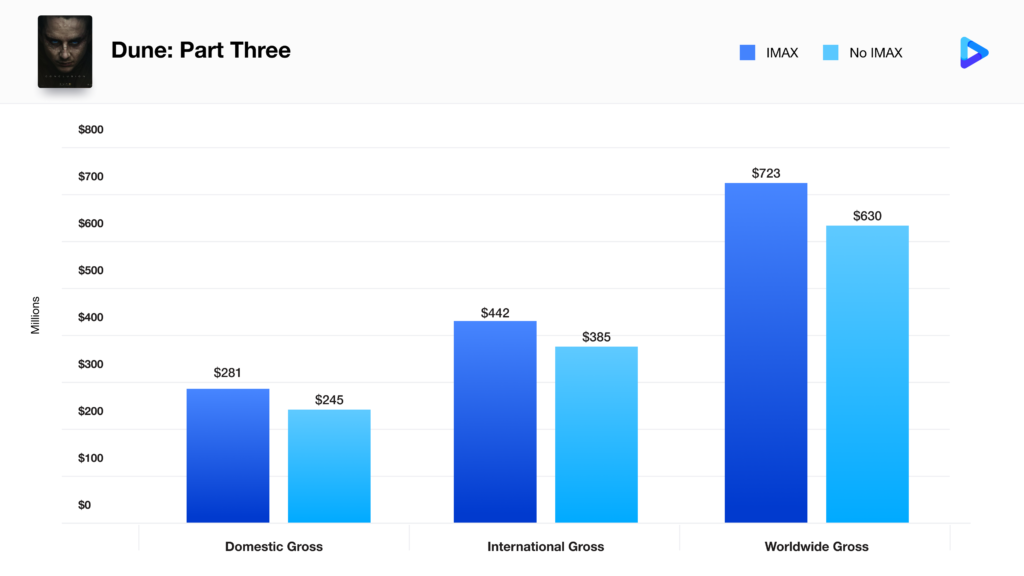

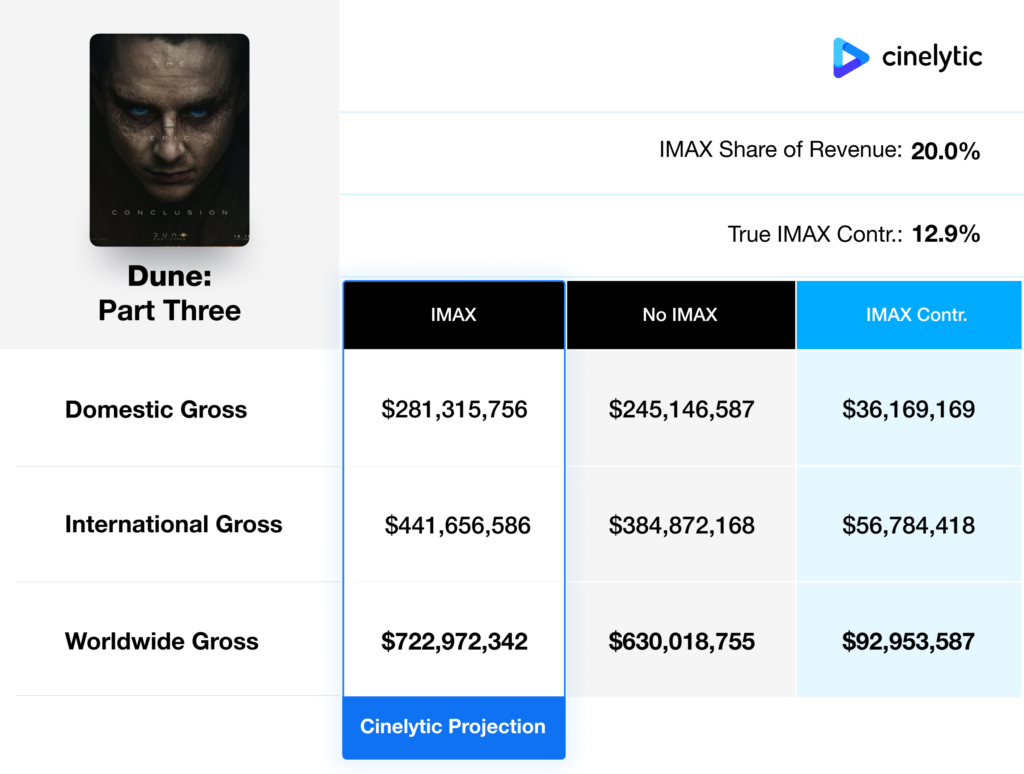

Dune: A True IMAX-Driven Event

For DUNE: PART THREE, IMAX is central to the theatrical experience. The model assumes a 20% IMAX share, significantly above the historical Native IMAX average of 11.8%, reflecting the franchise’s established premium format demand.

With IMAX included, projections reach US$281.3m domestic and US$441.7m international.

The true IMAX contribution is estimated at +12.9%, above the historical mid-range uplift of approximately 7.7% and closely aligned with DUNE: PART TWO (~13.2%). This elevated contribution is further supported by the extended IMAX exclusivity window.

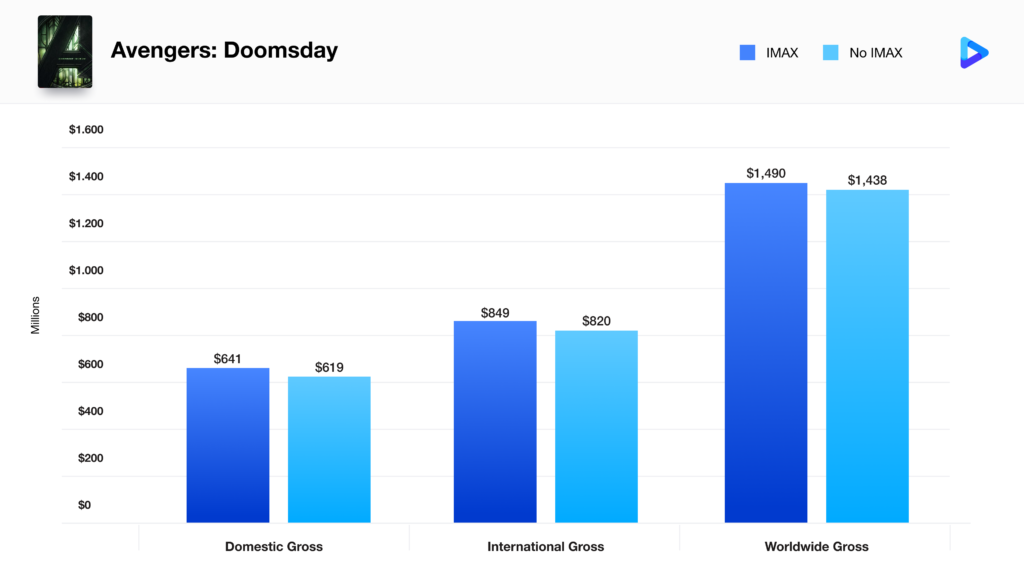

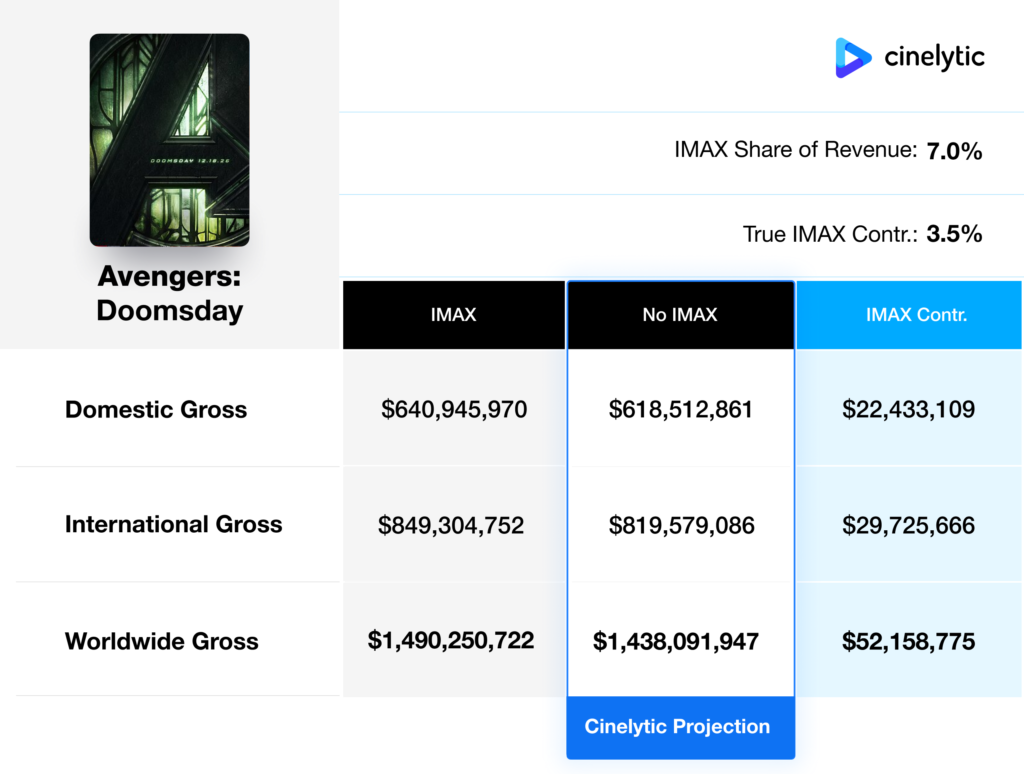

Avengers: A Premium Upsell, Not a Driver

For AVENGERS: DOOMSDAY, the model assumes a 7% IMAX share, consistent with historical averages for superhero titles.

Without relying on IMAX contribution, projections reach US$618.5m domestic and US$819.6m international.

The true IMAX contribution is estimated at +3.5%, slightly below the historical low-range uplift for superhero films. This is justified by the lack of IMAX access during the first three weeks of release, when the majority of box office is typically realized, and by the film’s positioning as a broad-demand event rather than a format-driven spectacle.

The Bigger Picture

The analysis highlights a clear pattern: IMAX-driven films generate meaningful incremental demand, while franchise blockbusters primarily leverage IMAX to enhance pricing and viewing experience rather than expand total audience size.

Final Takeaway

IMAX is not a one-size-fits-all multiplier. Its impact depends on how a film is produced, marketed, and released. Understanding these dynamics is essential for accurate forecasting, release strategy optimization, and maximizing premium format value.