The May box office, kicking off the summer movie season, is off to a very strong start, driven in large part by a pair of standout hits in MICHAEL and THE DEVIL WEARS PRADA 2.

Together, they’ve set the tone early, reinforcing the importance of front-loaded momentum and proving that when the right titles connect, the market responds immediately.

Before getting into what’s ahead, it’s worth grounding this summer in context.

Last summer reinforced a now-familiar pattern. The market was driven by recognizable IP, established franchises, and culturally embedded brands. Titles like THUNDERBOLTS, MISSION: IMPOSSIBLE – THE FINAL RECKONING, JURASSIC WORLD REBIRTH, SUPERMAN, FANTASTIC FOUR: FIRST STEPS, LILO & STITCH, and HOW TO TRAIN YOUR DRAGON anchored the season and delivered the bulk of box office volume.

At the same time, a handful of breakout titles proved there’s still room for upside outside pure franchise dependence. Films like 28 YEARS LATER, F1, and WEAPONS generated additional momentum and, in some cases, overperformed.

But the flip side remained just as clear. Several releases, including ELIO, SMURFS, I KNOW WHAT YOU DID LAST SUMMER, and BALLERINA, struggled to break through, reinforcing the reality that awareness alone is no longer enough. Positioning, timing, and perceived “event status” now matter more than ever.

That backdrop sets the stage for 2026.

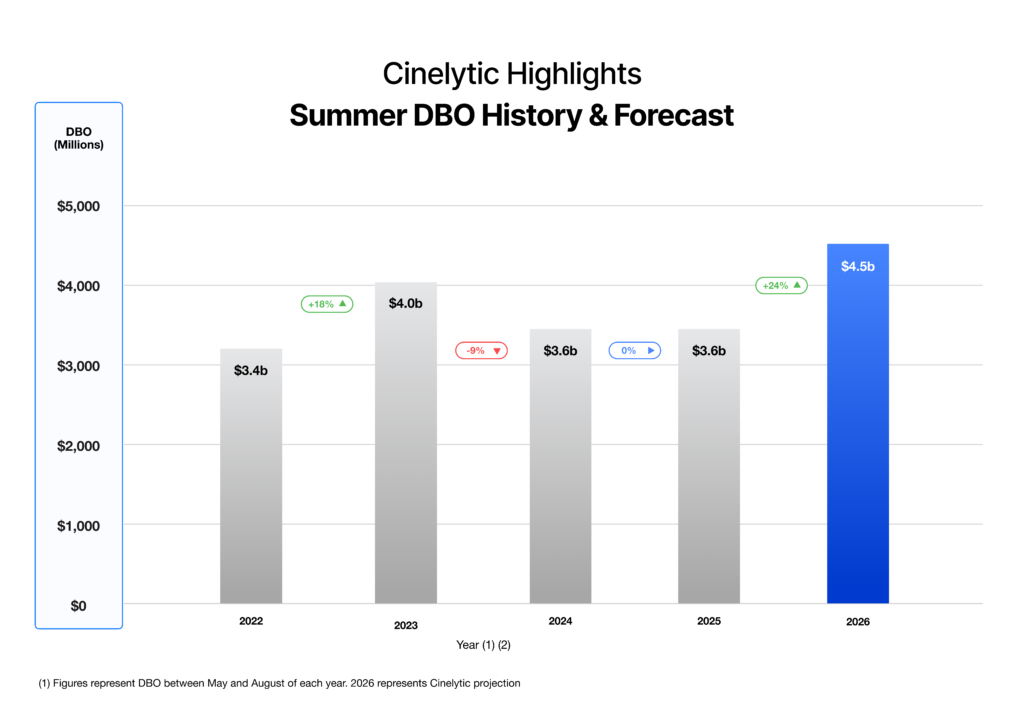

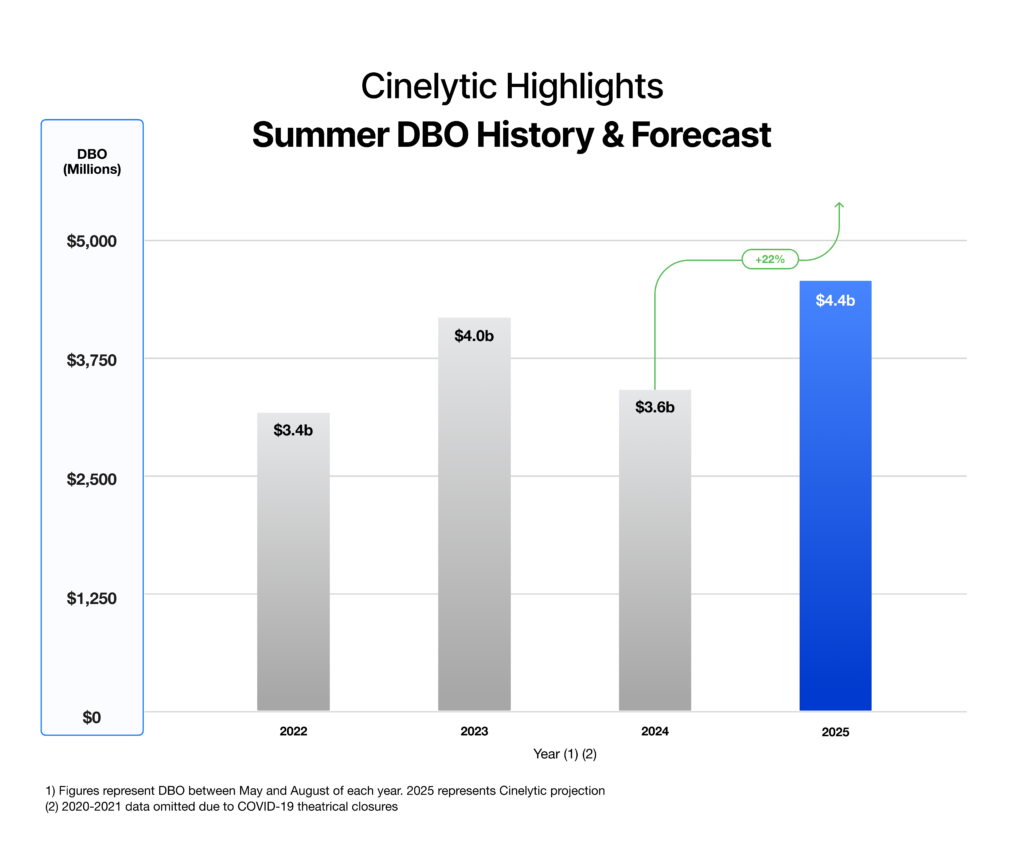

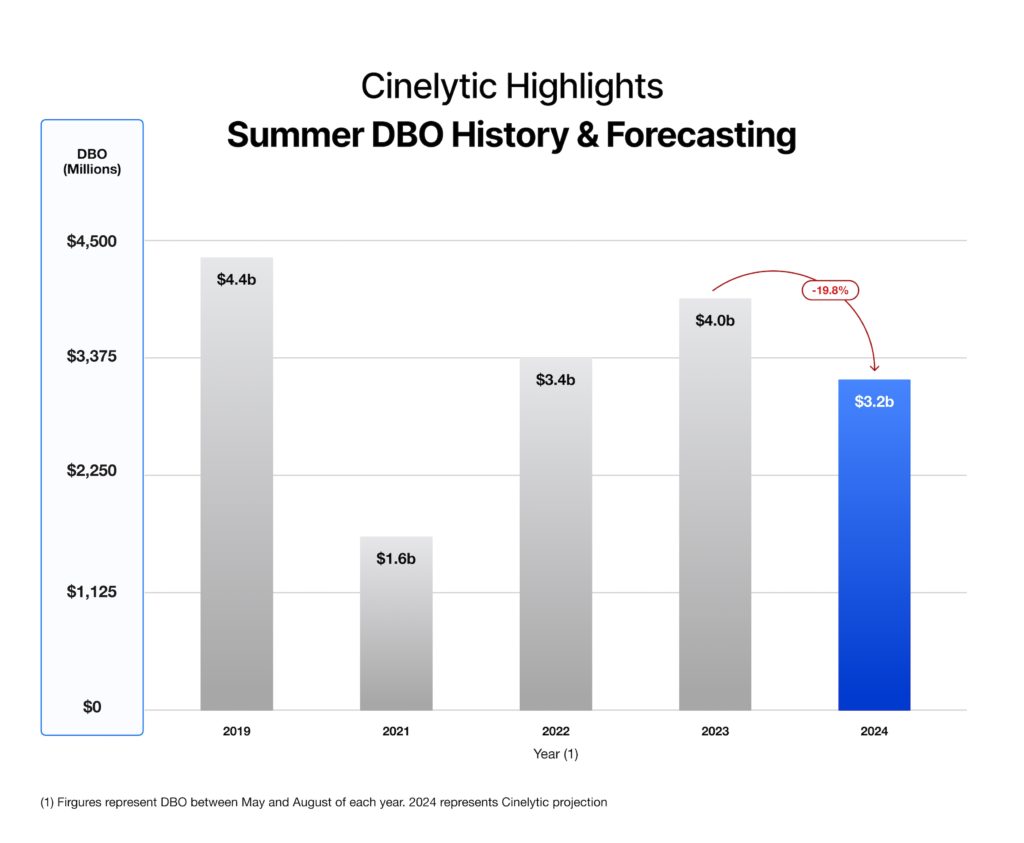

Summer DBO History

From a big-picture standpoint, the direction of the market is transparent. After the initial rebound in 2023 and a more stable yet underwhelming couple of years in 2024 and 2025, this summer feels different.

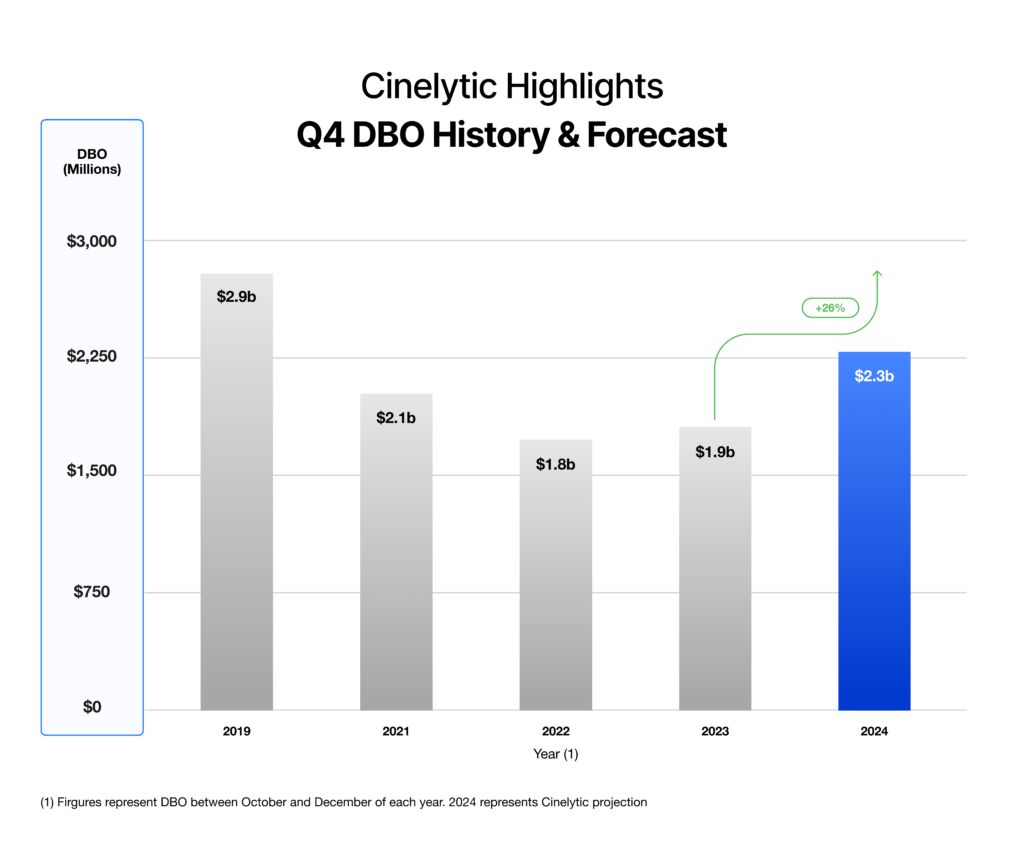

Based on projections from our Cinelytic box office predictive platform, made back in November ’25, the 2026 summer is tracking toward US$4.5b, which would mark a 24% jump from last year and the strongest summer since 2016, a period that featured titles like FINDING DORY, CAPTAIN AMERICA: CIVIL WAR, SUICIDE SQUAD, and THE SECRET LIFE OF PETS all hitting at scale. For a look at how this projection breaks down monthly, please see the graphic below:

What’s behind that isn’t just “more movies” or even bigger budgets. It’s a lineup that feels intentionally built around clear audience moments. The biggest films are positioned to feel like events, release dates are more strategically spaced, and there’s a healthy mix of franchise familiarity and broad audience appeal that allows multiple titles to succeed without stepping on each other.

So, if 2026 is lining up to match some of the strongest summers we’ve seen in the modern era, the real question becomes: what titles are projected to power a season back to those historical highs?

Upcoming Standouts

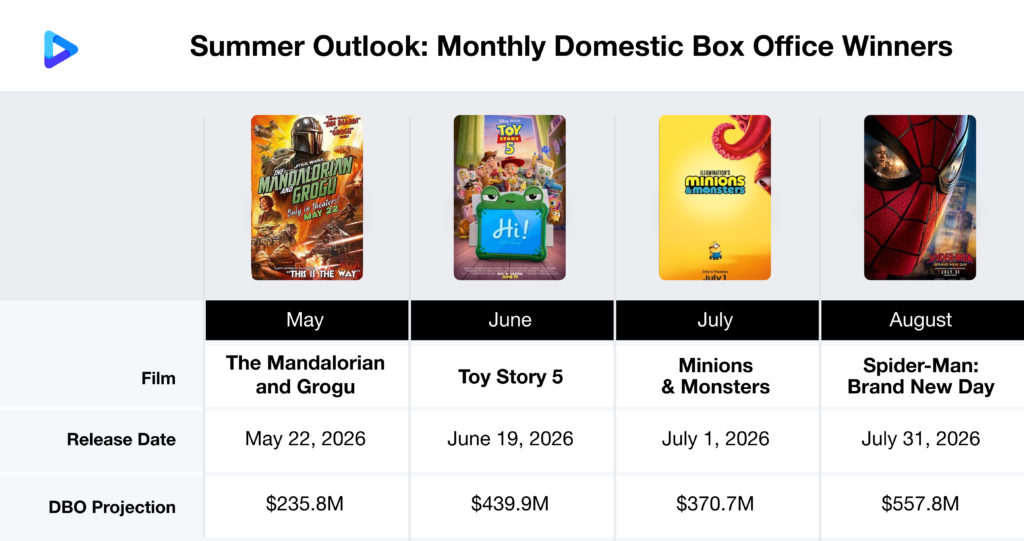

While May will be anchored by THE MANDALORIAN AND GROGU, it won’t be doing the work alone, with support from several strong performers still in theaters like the aforementioned MICHAEL and THE DEVIL WEARS PRADA 2, and even short tail-end contributions from PROJECT HAIL MARY and THE SUPER MARIO GALAXY MOVIE carrying over.

June is defined by TOY STORY 5, a proven franchise with broad four-quadrant appeal that is expected to dominate its window. July continues the trend with MINIONS & MONSTERS, reinforcing the strength of animated event titles in peak summer positioning. August, rather than tapering off, is carried by SPIDER-MAN: BRAND NEW DAY, extending the high point of the season deeper into the calendar.

What emerges is a pattern where each month is effectively led by a single high-conviction release. These titles are projected to be the biggest earners across their respective windows, but they are far from the only contributors shaping the summer.

Alongside these anchors sits a deep bench of immensely anticipated major releases between May and August, featuring some of the most high-profile talent in the industry. Titles like DISCLOSURE DAY, SUPERGIRL, MOANA, and of course Christopher Nolan’s star-studded epic THE ODYSSEY all have the potential to command significant attention. A few additional releases could also break through and make noise, including MORTAL KOMBAT II, JACKASS: BEST AND LAST, THE END OF OAK STREET, and INSIDIOUS: OUT OF THE FURTHER.

The result is a summer that is both top-heavy and deep, where standout tentpoles define each moment, but a broader mix of high-interest titles ensures sustained momentum across the full corridor.

All to Say…

The takeaway is clear. Summer 2026 is not just about a handful of big films performing well, it’s about a season that is operating at full strength, driven by the right combination of scale, timing, and audience engagement. When the slate is this well balanced, with clear event anchors supported by a deep bench of compelling releases, theatrical doesn’t just hold steady, it has room to accelerate. If the current trajectory continues, this summer has a real opportunity to match the strongest seasons we’ve seen and offer a clearer sense of where the ceiling for the modern box office might be.

The film industry’s ability to predict commercial performance has undergone a quiet revolution. What once required months of analyst work and educated guesswork can now be modeled in seconds — with accuracy rates that are changing how studios greenlight, finance, and release films.

The Old Way: Why Traditional Box Office Forecasting Fell Short

For most of Hollywood’s history, forecasting a film’s commercial potential was more art than science. Studio executives relied on a combination of historical comparables, instinct honed over decades, and expensive third-party tracking studies that arrived weeks — sometimes months — after key decisions had already been made.

The limitations were significant. Comparable title analysis (“comps”) depended on an analyst’s subjective interpretation of which past films were truly similar to the project at hand. Market research surveys captured audience intent at a single moment in time but couldn’t model how that intent might shift as cast, marketing, or release timing changed. International territory projections were often handled separately, if at all, with little systematic integration of how a film’s performance in one market might correlate with another.

Most critically, meaningful forecasting could only begin once a film was close to release — when a trailer existed, when cast was locked, when marketing had begun. At the greenlight stage, when the most consequential financial decisions are made, decision-makers were operating largely in the dark.

The result: an industry with notoriously high financial risk, where even well-resourced studios routinely absorb nine-figure write-downs on films that seemed commercially viable at the time of investment.

What Changed: The New Science of Box Office Forecasting

The convergence of three developments transformed what was possible: the accumulation of granular historical performance data across global markets, advances in machine learning capable of identifying patterns across thousands of variables simultaneously, and the computing infrastructure to run complex models in real time.

Modern forecasting platforms don’t simply look at how similar films performed in the past. They model the specific combination of factors that will shape a given project’s commercial trajectory — and they do it dynamically, updating projections as inputs change.

Film performance is not determined by any single variable in isolation. Machine learning excels precisely at this kind of multi-variable interaction analysis — identifying which combinations of factors have historically predicted strong performance, and weighting them accordingly.

A mid-budget action film starring an A-list actor with strong international appeal will perform very differently depending on whether it opens in August against major competition or in a January window with clear runway. Add IMAX screens and the revenue profile changes again. Change the director, alter the rating, shift the release to a streaming-first strategy — each variable interacts with the others in ways that simple spreadsheet models cannot capture.

Trained on thousands of historical titles with verified performance data across theatrical, home video, television, and streaming windows, modern forecasting models can identify which combinations of factors have historically predicted strong performance — and weight them accordingly when evaluating a new project.

The Key Variables Modern Forecasting Models Factor In

Sophisticated box office forecasting platforms integrate a wide range of project-specific criteria to generate their projections. Understanding these variables is useful both for interpreting forecast outputs and for structuring projects to optimize commercial performance.

Production Budget. Budget is both an input and a signal. It shapes the scale and quality of the final product, determines the minimum marketing spend required to recoup investment, and signals to the market what kind of film it is. Modern models use budget not just as a cost figure but as a contextual variable that interacts with genre, talent, and release strategy.

Genre and Sub-Genre. Genre is among the strongest predictors of audience demand, but genre alone is insufficient. A horror film targeting a young female demographic performs differently from a supernatural thriller with broad crossover appeal, even if both are categorized as “horror.” Modern models use granular sub-genre classifications and audience demographic targeting to refine projections beyond top-level genre labels.

Cast and Key Creatives. Talent analytics represent one of the most significant advances in modern forecasting. Leading platforms now maintain detailed performance databases covering hundreds of thousands of actors, directors, writers, and producers — tracking not just their films’ aggregate performance but their specific contribution to different genres, budget ranges, and international territories. This allows forecasters to move beyond simple “star power” assessments and model how a specific pairing of director and lead actor might perform in specific markets.

Franchise and IP Value. Original IP and franchise extensions follow fundamentally different commercial trajectories. Sequel and franchise titles carry built-in audience awareness that reduces marketing costs and provides a floor on opening weekend performance. Modern models account for franchise position, franchise health based on the trajectory of recent installments, and the specific IP’s demographic profile.

Release Timing and Competitive Landscape. The box office is a zero-sum competition for audience attention in a given weekend. Release date selection involves modeling the specific competitive environment a film will enter — not just seasonal demand patterns, but the specific titles it will share the market with, their target demographics, and their likely performance trajectories.

Premium Format Uplift. IMAX, 4DX, Dolby Cinema, and other premium formats now represent a significant and growing share of theatrical revenue. Modern forecasting models account for a film’s suitability for premium exhibition and incorporate premium uplift into territory-level projections.

Release Strategy: Theatrical vs. Platform Rollout. The choice between wide theatrical release, limited platform rollout, and day-and-date streaming release has profound implications for revenue across all windows. AI forecasting platforms can model these scenarios comparatively, allowing decision-makers to evaluate the revenue implications of each approach before committing.

Global Forecasting: The 80-Territory Challenge

Perhaps the most significant limitation of traditional forecasting was its domestic bias. Most historical forecasting infrastructure was built around North American theatrical performance, with international projections added as rough multipliers derived from broad market patterns.

This approach fails to capture the complexity of modern international film distribution. A film’s domestic and international performance are not simply correlated — they interact in ways that depend on specific market factors. Some films dramatically outperform their domestic results in specific territories due to local cultural resonance, cast popularity, or genre preferences that differ markedly from North American audiences.

Modern forecasting platforms now generate territory-level projections across up to 80 markets simultaneously, modeling the specific factors that drive performance in each. Key international markets — China, Japan, South Korea, France, Germany, the UK, and Australia among the most significant — each have distinct audience preferences, competitive dynamics, and seasonal patterns that a global forecasting model must account for independently.

International revenues now represent the majority of theatrical performance for most wide-release films. Territory-level forecasting enables strategic tradeoffs to be evaluated explicitly rather than discovered after release.

Strategic decisions about casting, reshoots, localization, and release timing that are optimized for domestic performance can inadvertently undermine international results — and vice versa. Territory-level forecasting enables these tradeoffs to be evaluated explicitly rather than discovered after release.

Forecasting from the Development Stage: The Greenlight Advantage

The most significant advance in modern forecasting — and the one with the greatest potential to reduce the industry’s financial risk profile — is the ability to generate meaningful revenue projections at the earliest stages of a project’s development.

Traditional forecasting required a completed film, or at minimum a finished trailer and locked cast. Development-stage decisions — which scripts to option, which treatments to develop into screenplays, how to structure a project’s creative elements before significant capital is committed — were made with almost no quantitative guidance.

Modern platforms have changed this. By training on the complete set of factors that have historically predicted commercial performance, they can generate substantive projections from a project description, working title, genre, target budget range, and preliminary cast wishlist. As development progresses and these elements solidify, the model’s confidence intervals narrow and projections become more precise.

The value is not that these models can predict the future with certainty — no model can. The value is that they provide a structured, data-driven framework for evaluating the commercial implications of creative decisions at the moment those decisions are still flexible. Should the budget be increased to accommodate a stronger cast? Would a genre shift improve the international revenue profile without compromising domestic performance? Is a wide theatrical release the right strategy for this project, or would a platform rollout optimize total revenue?

These are questions that studios have historically answered with experience and instinct. Modern forecasting gives them a rigorous quantitative input to inform those conversations — while leaving the final judgment where it belongs: with the decision-makers who understand the full context of the project.

Real-Time Scenario Planning: Testing Before Committing

One of the most practically valuable capabilities of modern forecasting platforms is real-time scenario modeling — the ability to instantly compare the financial implications of different strategic choices without committing to any of them.

A studio executive evaluating a film in development can run scenarios simultaneously: What does the revenue profile look like with the current cast versus an alternative lead? How does a summer release compare to an awards-season rollout? What is the incremental revenue impact of an IMAX-optimized production versus a standard theatrical release? How does a streaming-first strategy affect total revenue across all windows over a three-year period?

In a traditional workflow, generating answers to these questions required weeks of analyst work, multiple rounds of revision, and sequential rather than parallel evaluation. By the time a thorough analysis was complete, the decisions it was meant to inform had often already been made.

Real-time scenario planning collapses this timeline. Projections across all modeled variables update in seconds as inputs change — enabling decision-makers to explore the full strategic space before committing, in the room, during the conversations where decisions are actually made.

Accuracy as a Business Asset: What 88%+ Really Means

Forecasting accuracy is the foundation on which the entire value proposition rests. A model that produces plausible-looking numbers but systematically diverges from actual results provides false confidence rather than genuine decision support.

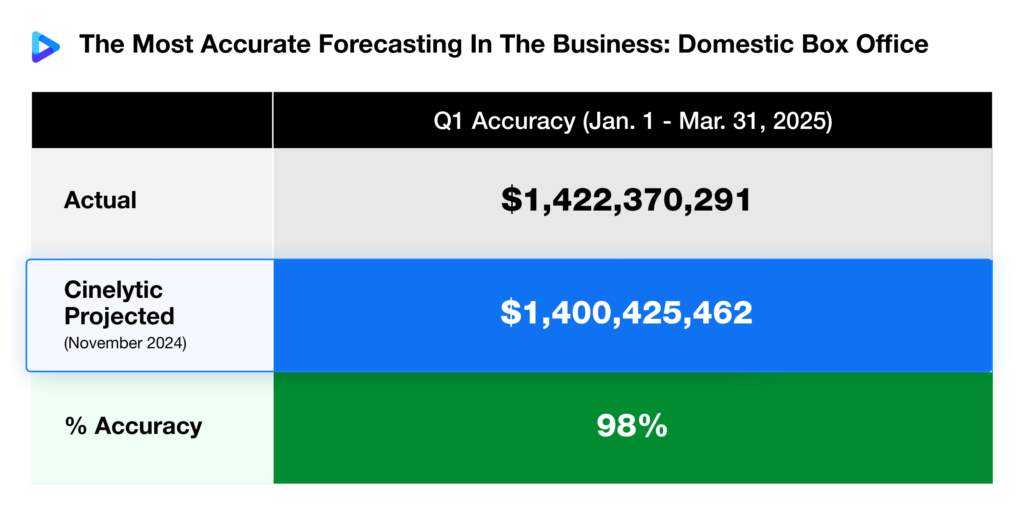

Modern forecasting platforms, when benchmarked against actual box office performance on films modeled at the greenlight stage, now achieve title-level accuracy rates above 88% across a broad range of genres, budget levels, and release windows. For individual titles, this means the model’s median projection typically falls within a narrow band of actual performance — a level of precision that, until recently, was simply not achievable from the development stage.

Consider the difference between a $150 million production greenlit with an 88%+ accurate revenue forecast and the same decision made with the traditional tools available a decade ago. The modern approach doesn’t eliminate risk — no forecast can — but it substantially narrows the range of outcomes the decision-maker is navigating. Catastrophic misallocations of capital become less likely not because modern tools prevent bad creative decisions, but because they provide earlier and more accurate signals about which commercial strategies are likely to succeed.

For independent film companies and distributors operating with tighter margins than the major studios, this accuracy improvement is particularly meaningful. A bad greenlight decision that a major studio can absorb as a write-down can represent an existential threat to a smaller company. Accurate early-stage forecasting reduces that risk significantly.

The Bigger Picture: Forecasting as Part of an Integrated Intelligence Stack

Box office forecasting is one component of a broader decision intelligence infrastructure that the most sophisticated film companies are now building. Financial projections are most valuable when they are connected to the other data flows that inform the content lifecycle — development evaluation, IP management, audience sentiment analysis, and rights sales.

A film that receives strong early-stage revenue projections still needs to navigate development, production, marketing, and distribution decisions that will determine whether it reaches its commercial potential. Each stage generates new information that should update the financial model. And the insights from one film’s performance feed back into the forecasting model, improving its accuracy on future projects.

This is the direction the industry is moving: from isolated analytical exercises to continuous, integrated intelligence that supports every major decision from script evaluation through global distribution — connecting creative ambition with the business strategy required to realize it.

Cinelytic is the entertainment industry’s leading content intelligence platform, providing real-time financial forecasting, talent analytics, and scenario planning across 80 international territories. Learn more at cinelytic.com or request a demonstration at cinelytic.com/contact

Recent industry developments have re-centered the importance of theatrical windows in an evolving distribution landscape.

Recent Announcements:

Most notably, Universal Pictures’ announcement to extend its theatrical window to approximately 45 days for key releases stands out as a clear signal of confidence in the big-screen model, an approach further reinforced at CinemaCon where Steven Spielberg praised the move and suggested longer windows, while David Ellison reaffirmed a commitment to at least 45 day exclusive theatrical runs across Paramount’s slate.

This renewed emphasis comes at a time not long after there were widespread concerns that a potential Netflix acquisition of Warner Bros. Pictures could compress theatrical windows even for major IP releases. Against this backdrop, the relationship between theatrical performance and downstream streaming success has become increasingly critical.

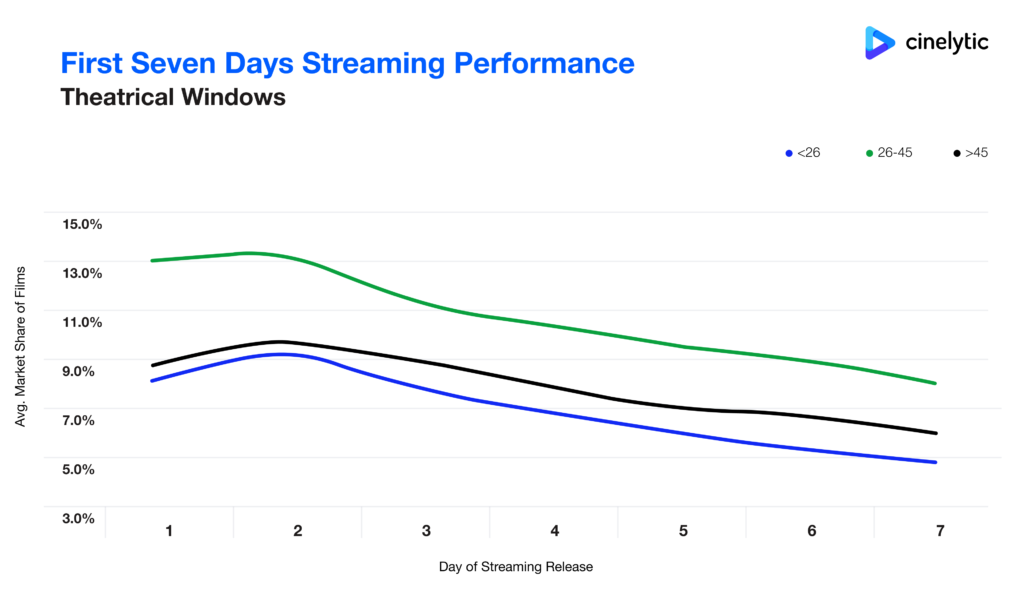

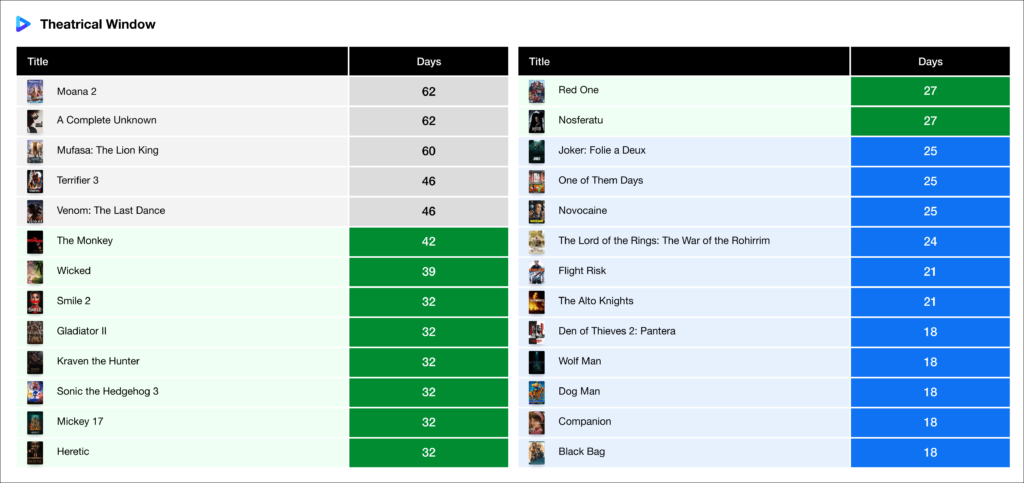

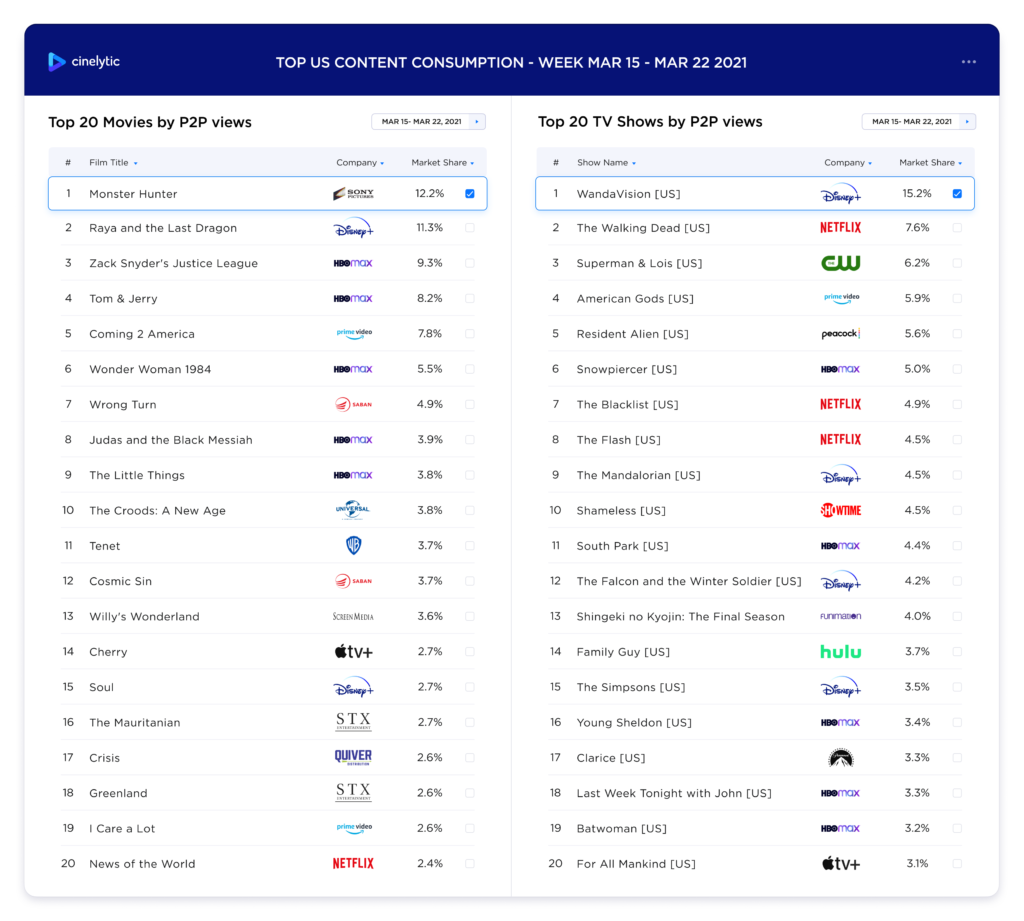

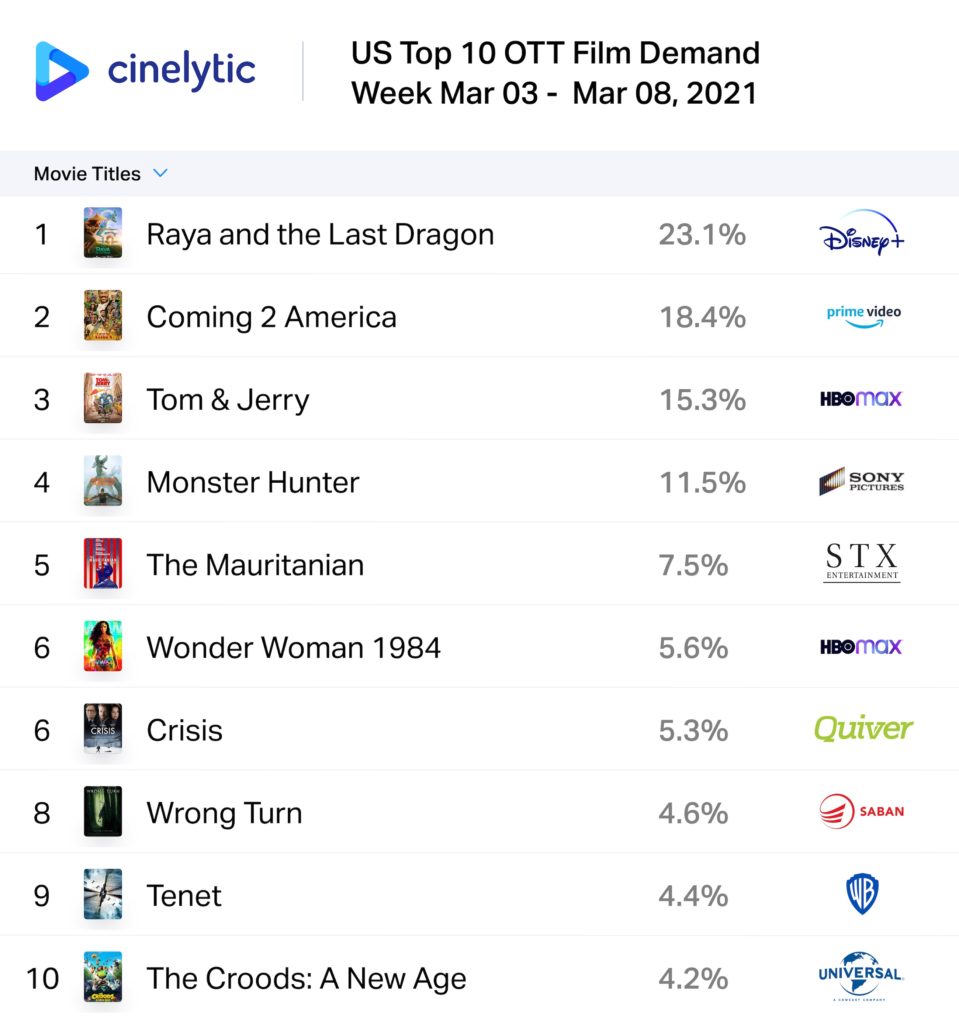

In October 2025, our team conducted an analysis of 30 films that received a theatrical release in 2025 and had completed at least their first week of digital availability. The findings were clear and consistent: films with theatrical exclusive windows of 26-to-45-day delivered the strongest streaming performance, and films that performed “on target” at the domestic box office relative to consensus industry projections also outperformed on streaming.

Now, with Q1 2026 coming to a close, we have expanded this dataset to include more recent major releases bringing the total to 39 titles. This updated analysis includes films that not only completed their theatrical runs across varying levels of success, but also launched on digital platforms since the start of 2026.

Notably, several titles released theatrically between September and December 2025 are excluded from this update, as the focus regarding added titles was intentionally placed on films that debuted on digital platforms in 2026.

Distribution Timing and Box Office Results

Across the 39 films analyzed, 16 films had theatrical windows of 25 days or less, 12 films fell within the 26-to-45-day range, and 11 films exceeded 45 days.

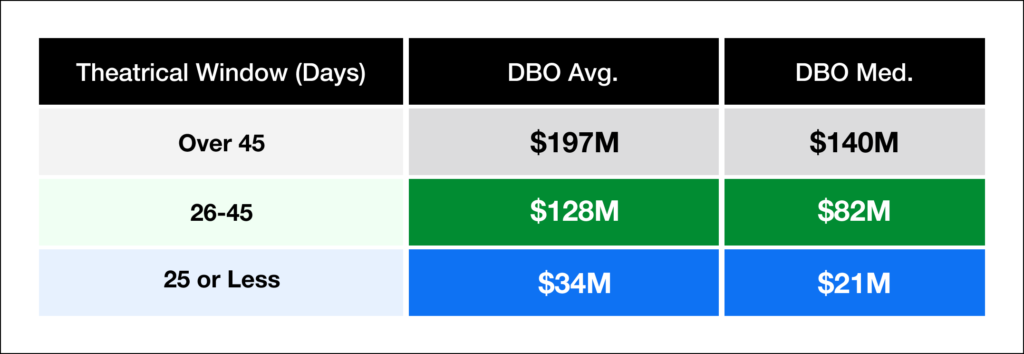

Average domestic box office DBO performance by window shows that films with 25 days or less averaged US$29.7m, films in the 26 to 45 day range averaged US$186.2m, and films with windows greater than 45 days averaged US$192.7m.

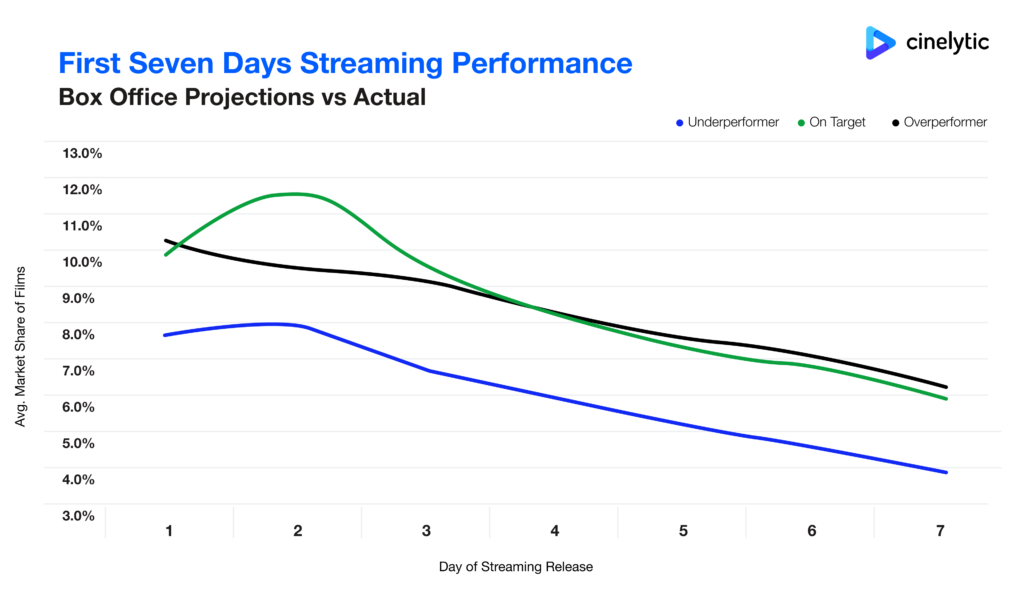

In terms of performance versus expectations, 11 films underperformed, 21 films were on target, and 7 films overperformed.

As expected, films with longer theatrical windows generally achieved higher box office outcomes than those with shorter windows. However, the more compelling insight emerges when examining downstream streaming performance.

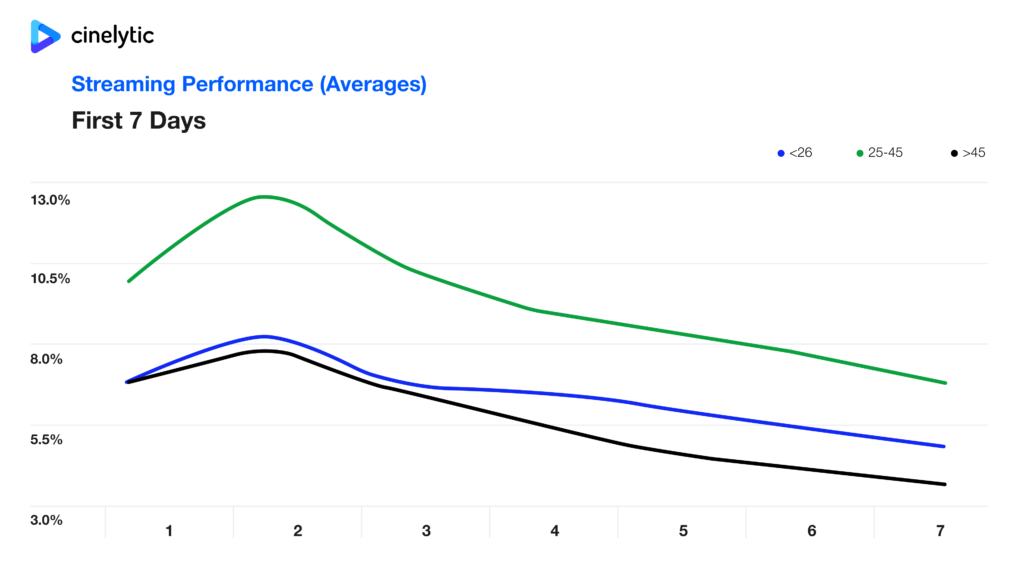

Theatrical Windows vs Streaming

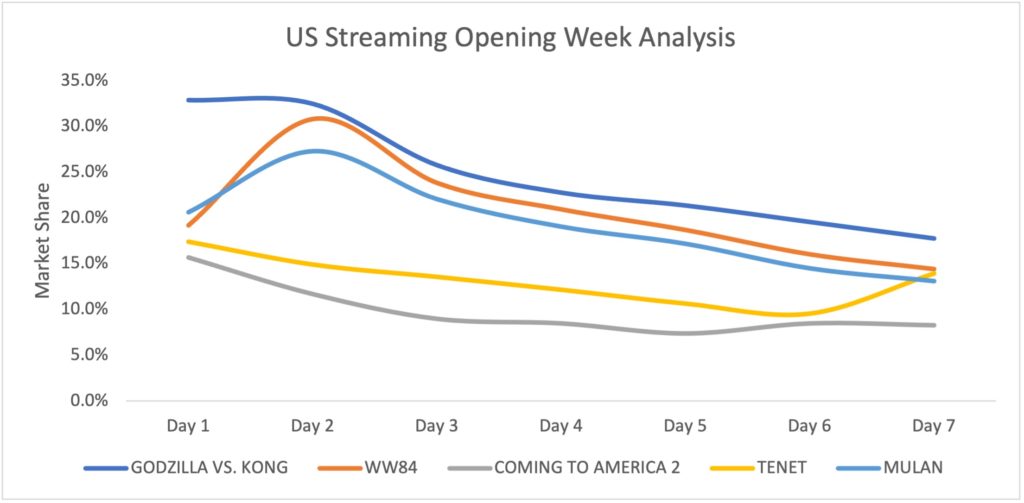

Consistent with prior findings, films in the 26-to-45-day window range significantly outperformed on streaming. These films averaged a 10.5% viewing market share capture in their first seven days against all competing and available digital titles. Films with windows greater than 45 days averaged 7.6%, while films with windows of 25 days or less averaged 6.5%.

Box Office Expectations vs Streaming

The correlation between domestic box office performance and streaming success also remains consistent. Films that performed on target averaged an 8.8% viewing share, slightly ahead of overperforming films at 8.6%. Underperforming films lagged behind at 6.3%.

Why the Mid-Window Strategy Continues to Win

The continued strength of the 26-to-45-day window reflects a critical balance between theatrical momentum and streaming freshness. Films in this range benefit from having enough time in theaters to build awareness and cultural relevance, while still transitioning to digital at a point when audience demand remains high.

Short window titles of 25 days or less often signal weaker theatrical confidence, limiting both box office scale and downstream demand. Conversely, films with longer windows over 45 days, while often successful theatrically, can lose immediacy by the time they reach streaming platforms.

Similarly, films that perform on target at the box office tend to be the most efficiently marketed and accurately positioned, arriving on streaming with strong awareness without the volatility associated with underperformance or overexposure.

All to Say…

With an expanded dataset and the inclusion of 2026 digital releases, the conclusions from the initial 2025 analysis have only strengthened. The 26-to-45-day theatrical window remains the optimal strategy for maximizing streaming impact, and meeting expectations at the box office correlates most strongly with streaming success.

This context makes the commitments by Universal and Paramount particularly notable. By anchoring their strategy around a roughly 45-day theatrical window, the studios are positioning themselves at the upper end of the range that continues to demonstrate the strongest combined performance across both box office and streaming. The data increasingly reinforces that this window length strikes the most effective balance between maximizing theatrical revenue while preserving urgency and demand for digital release.

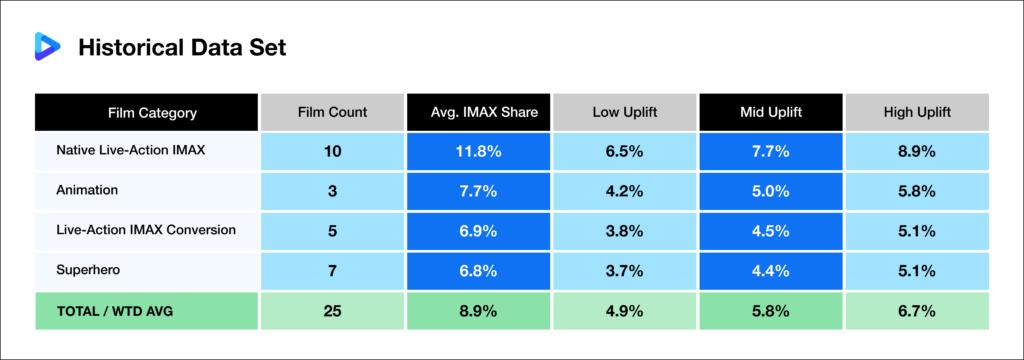

To better understand the real impact of IMAX on theatrical performance, we analyzed 25 major films from 2015 to 2025 with confirmed IMAX revenue data. These titles were grouped into four categories: Native Live-Action IMAX, Animation, Live-Action IMAX Conversion, and Superhero. The objective is to isolate how much IMAX revenue is truly incremental rather than simply shifted from standard screens.

Native vs Conversion: Why It Matters

Native IMAX films are shot using IMAX cameras and designed for premium viewing. Examples include OPPENHEIMER, SINNERS, and F1: THE MOVIE. These films consistently generate higher IMAX share and stronger incremental demand.

IMAX conversions are films shot traditionally and later optimized for IMAX screens, such as MISSION: IMPOSSIBLE – FALLOUT and JURASSIC WORLD: FALLEN KINGDOM. These benefit from IMAX exposure but typically generate lower incremental impact.

Superhero films are analyzed separately due to their scale and built-in demand, where IMAX primarily acts as a premium upsell rather than a core driver of incremental audience.

From IMAX Share to True Uplift

The core relationship used in the model is: IMAX Uplift = IMAX Share × α. IMAX share reflects the % of total box office from IMAX, while α represents the portion of IMAX demand that is truly incremental.

The α factor is derived from observed ticket price premiums and estimated admissions that would not have occurred without IMAX. This produces low, mid, and high scenarios that serve as practical forecasting ranges.

Key Distinction: Share vs True Contribution

IMAX share measures where revenue is captured, while IMAX uplift measures how much of that revenue is truly created. A film may generate 10% or more of revenue from IMAX, but only a portion of that reflects incremental audience demand rather than substitution from standard formats.

Historical Context and Benchmarks

Across the dataset, Native IMAX films average just under 12.0% IMAX share of total revenue. Superhero films average closer to 7.0%, reflecting strong baseline demand independent of format.

These benchmarks are critical for contextualizing forward-looking assumptions and identifying outliers driven by franchise strength or format-specific positioning.

Applying the Model: Dune vs Avengers

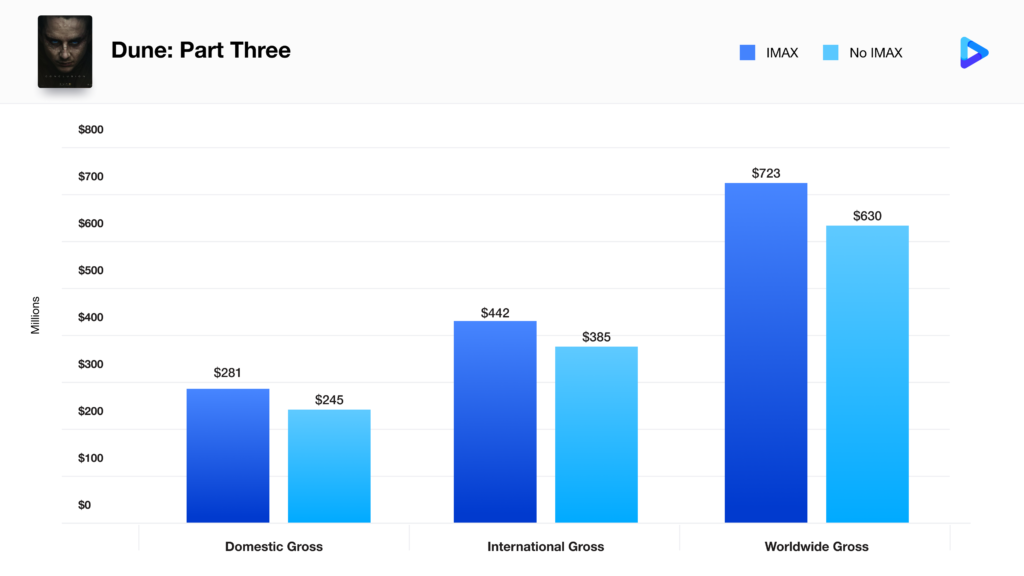

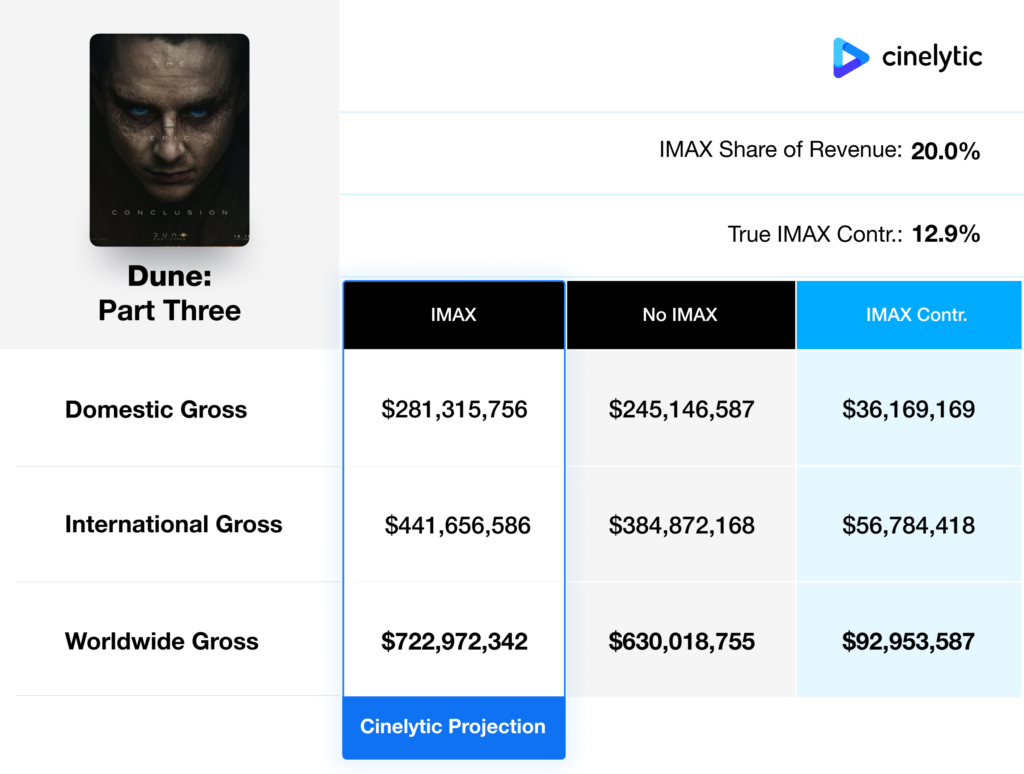

Using the Cinelytic predictive forecasting platform, we applied this framework to two major same-date releases: DUNE: PART THREE and AVENGERS: DOOMSDAY. The release timing introduces a key structural dynamic, with Denis Villeneuve’s sci-fi epic expected to secure approximately three weeks of IMAX exclusivity.

Dune: A True IMAX-Driven Event

For DUNE: PART THREE, IMAX is central to the theatrical experience. The model assumes a 20% IMAX share, significantly above the historical Native IMAX average of 11.8%, reflecting the franchise’s established premium format demand.

With IMAX included, projections reach US$281.3m domestic and US$441.7m international.

The true IMAX contribution is estimated at +12.9%, above the historical mid-range uplift of approximately 7.7% and closely aligned with DUNE: PART TWO (~13.2%). This elevated contribution is further supported by the extended IMAX exclusivity window.

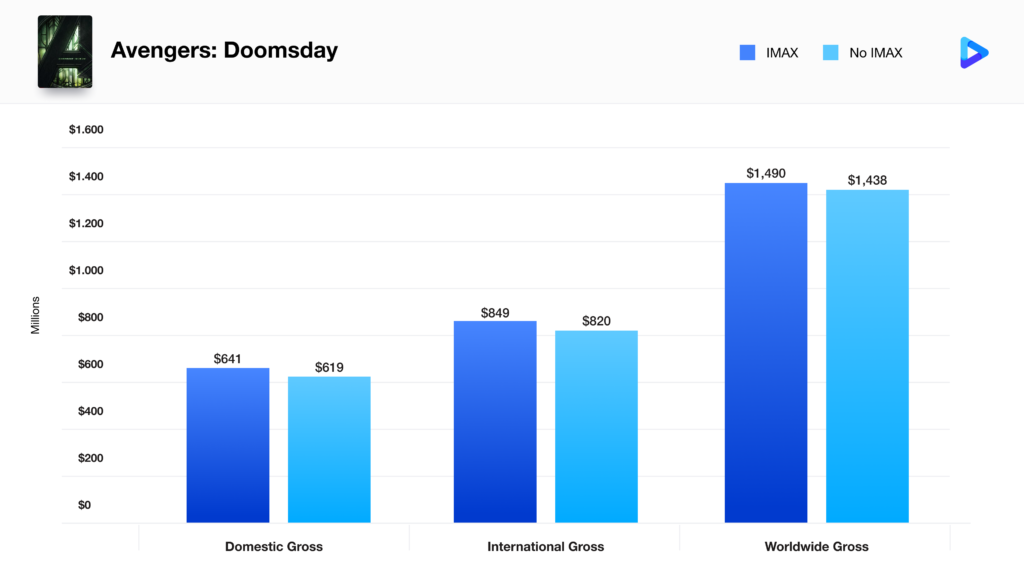

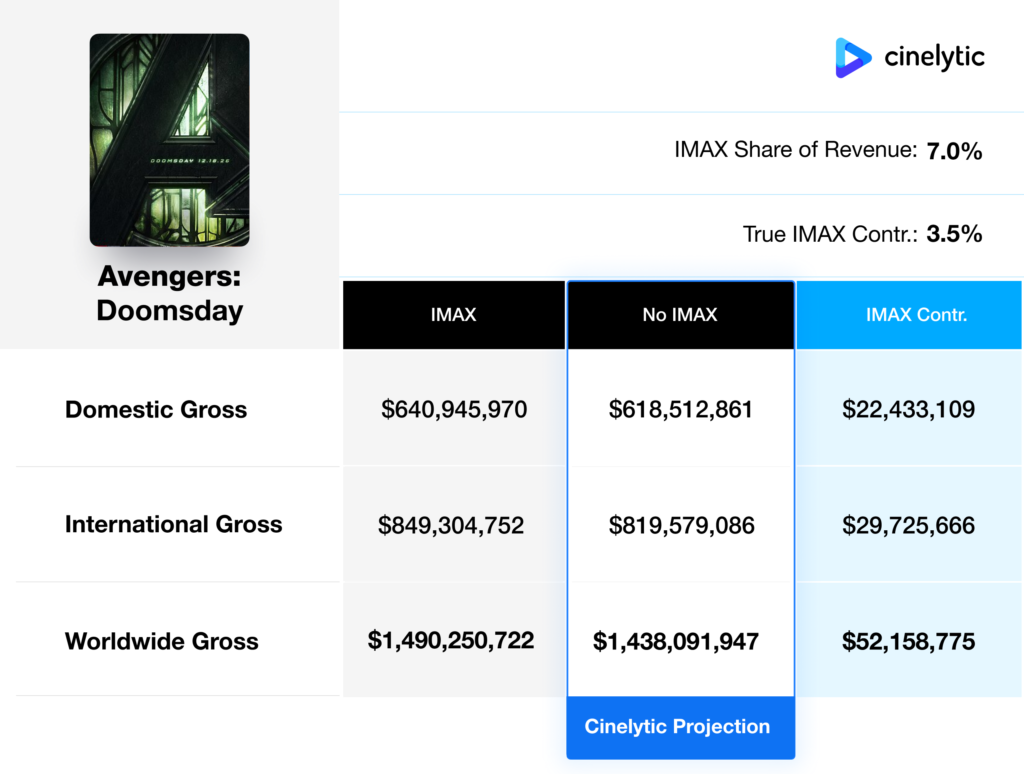

Avengers: A Premium Upsell, Not a Driver

For AVENGERS: DOOMSDAY, the model assumes a 7% IMAX share, consistent with historical averages for superhero titles.

Without relying on IMAX contribution, projections reach US$618.5m domestic and US$819.6m international.

The true IMAX contribution is estimated at +3.5%, slightly below the historical low-range uplift for superhero films. This is justified by the lack of IMAX access during the first three weeks of release, when the majority of box office is typically realized, and by the film’s positioning as a broad-demand event rather than a format-driven spectacle.

The Bigger Picture

The analysis highlights a clear pattern: IMAX-driven films generate meaningful incremental demand, while franchise blockbusters primarily leverage IMAX to enhance pricing and viewing experience rather than expand total audience size.

Final Takeaway

IMAX is not a one-size-fits-all multiplier. Its impact depends on how a film is produced, marketed, and released. Understanding these dynamics is essential for accurate forecasting, release strategy optimization, and maximizing premium format value.

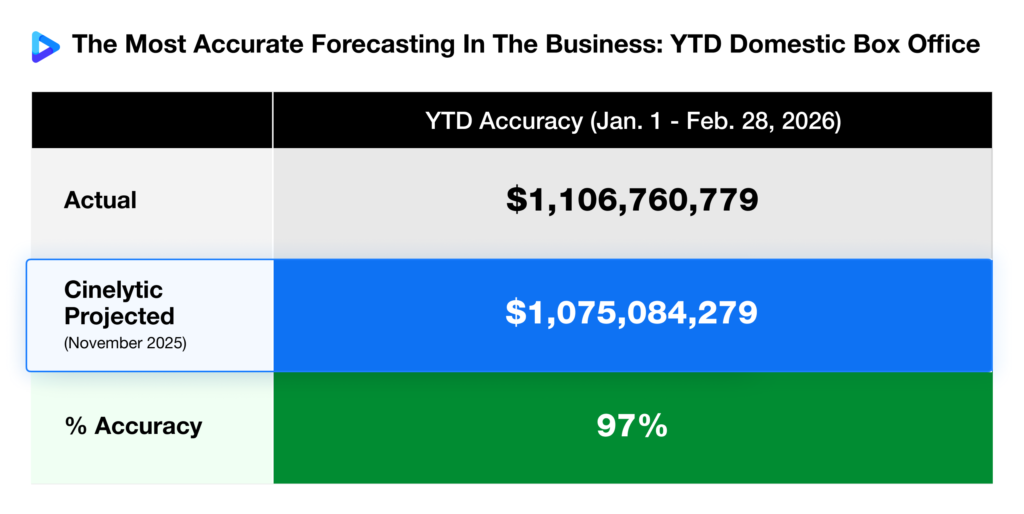

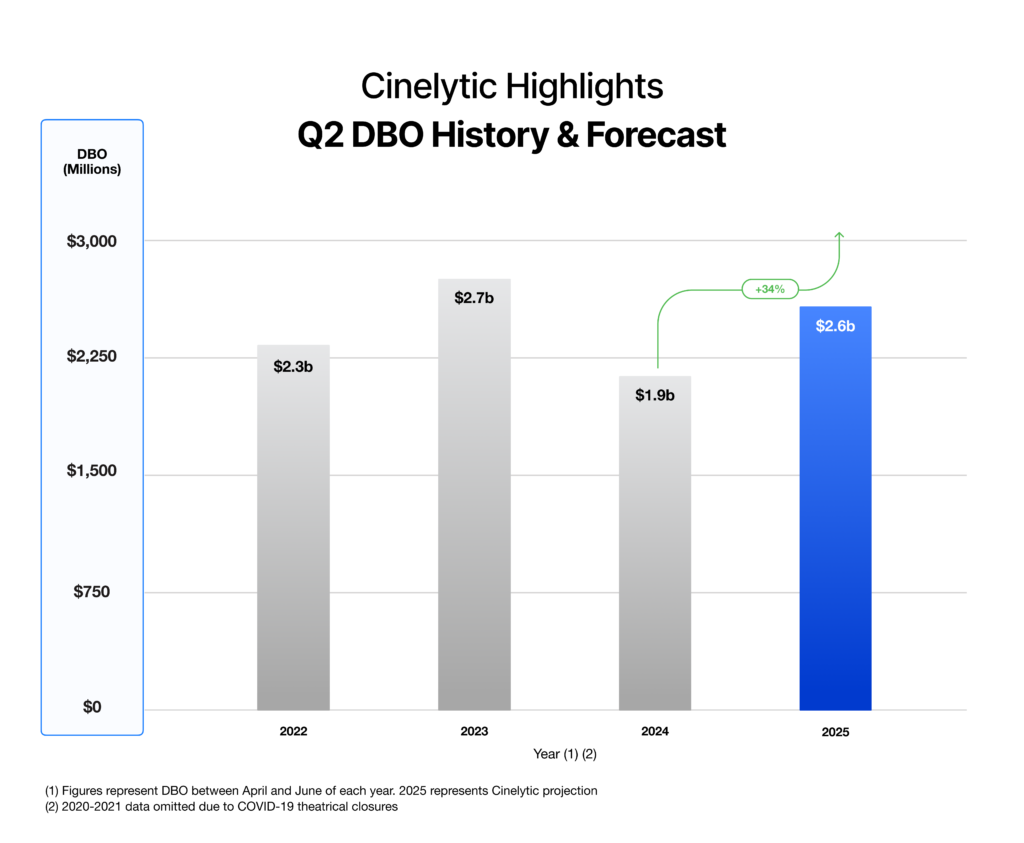

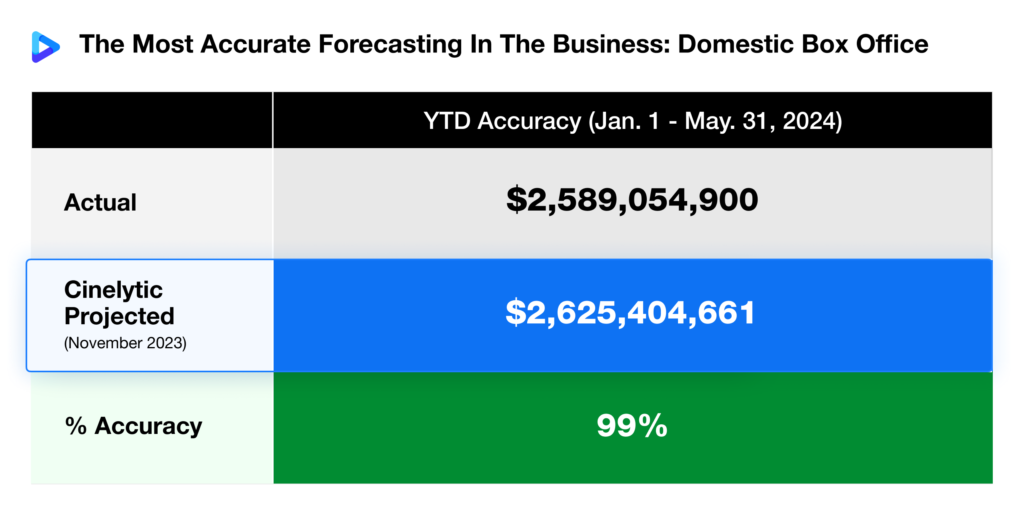

Throughout the year we will continue tracking the performance of the domestic box office (DBO) projections we developed at the end of 2025 and published this past January for the 2026 film slate. As illustrated in the graphic below, through the first two months of the year Cinelytic’s forecasts achieved an impressive 97% accuracy rate:

How Does Q2 Look?

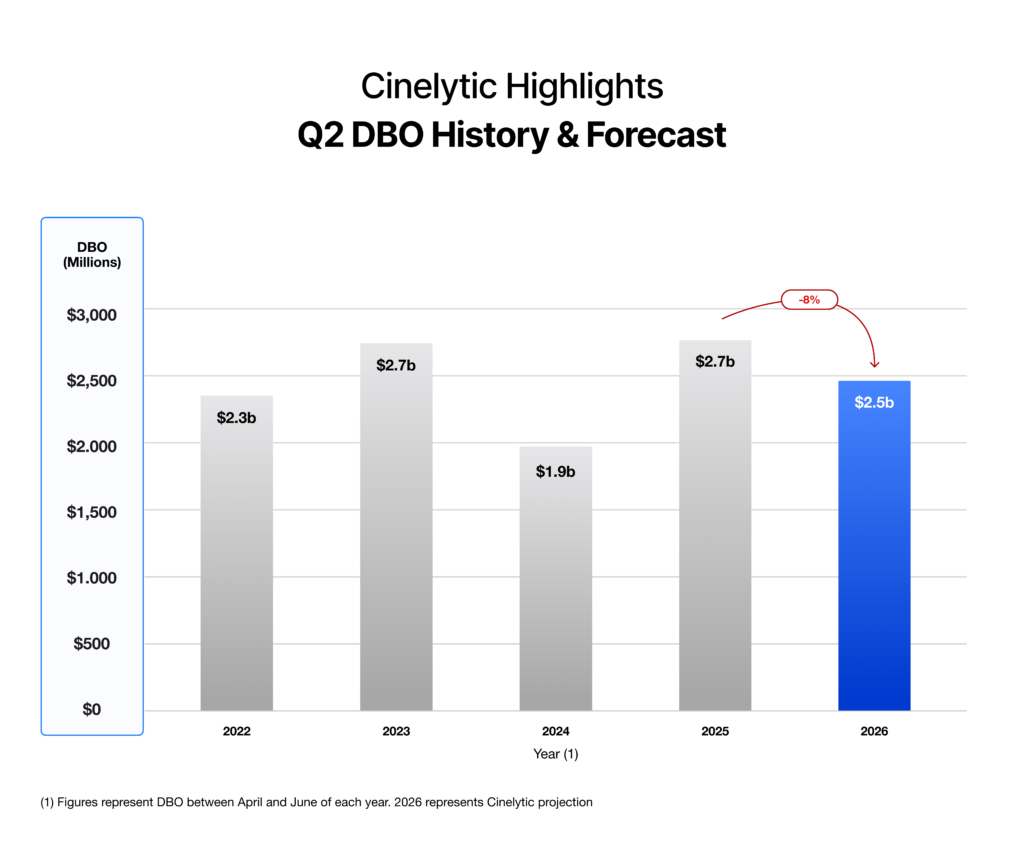

Looking ahead, the theatrical slate in Q2 will largely shape the streaming landscape for mid-2026. Consistent with the forecasting approach we provide, the chart below highlights our projection for Q2 2026 DBO, which currently indicates a modest decline of roughly 8% in comparison to Q2 2025:

At first glance, it may seem unusual to see an approximately 8% decline in the Q2 forecast year over year, particularly given that we projected 2026 to reach a total of around US$9.6b, which would mark the strongest overall DBO since 2019. However, the comparison is largely influenced by the exceptionally strong performance of Q2 2025, which benefited from several titles that significantly outperformed expectations.

Films such as A MINECRAFT MOVIE, SINNERS, LILO AND STITCH, and F1 all delivered results well above early projections. Those overperformers created a particularly high benchmark that makes the 2026 projection of about US$2.47b appear softer despite still representing a healthy seasonal performance.

Importantly, Q2 2026 still includes several releases expected to rank among the highest grossing titles of the entire year, including THE SUPER MARIO GALAXY MOVIE, THE MANDALORIAN AND GROGU, and TOY STORY 5. The quarter is also supported by additional high-profile titles such as Antoine Fuqua’s biopic MICHAEL, the long awaited THE DEVIL WEARS PRADA 2, MORTAL KOMBAT 2, SUPERGIRL, and Steven Spielberg’s UFO thriller DISCLOSURE DAY.

Q1 Streaming Performance

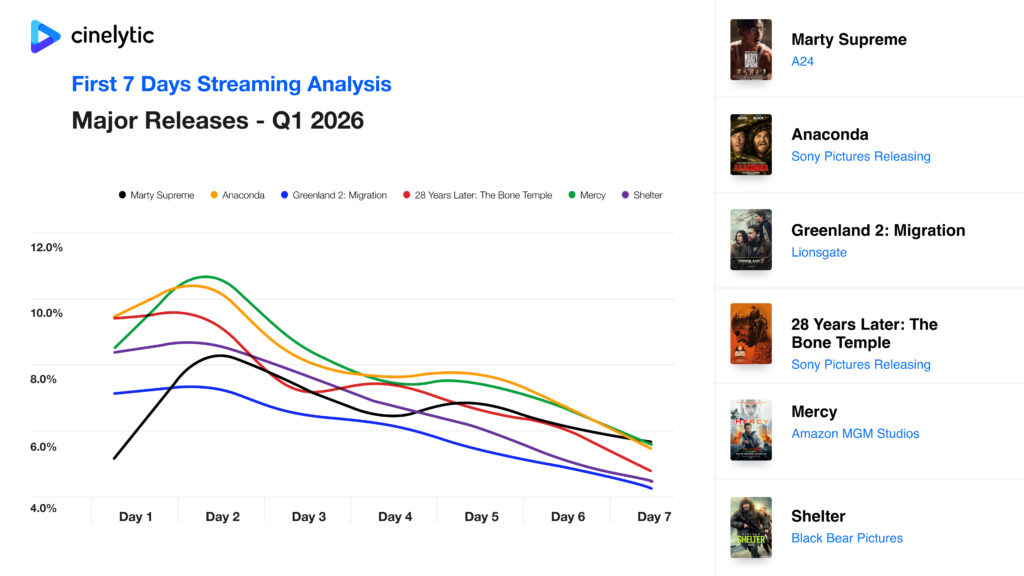

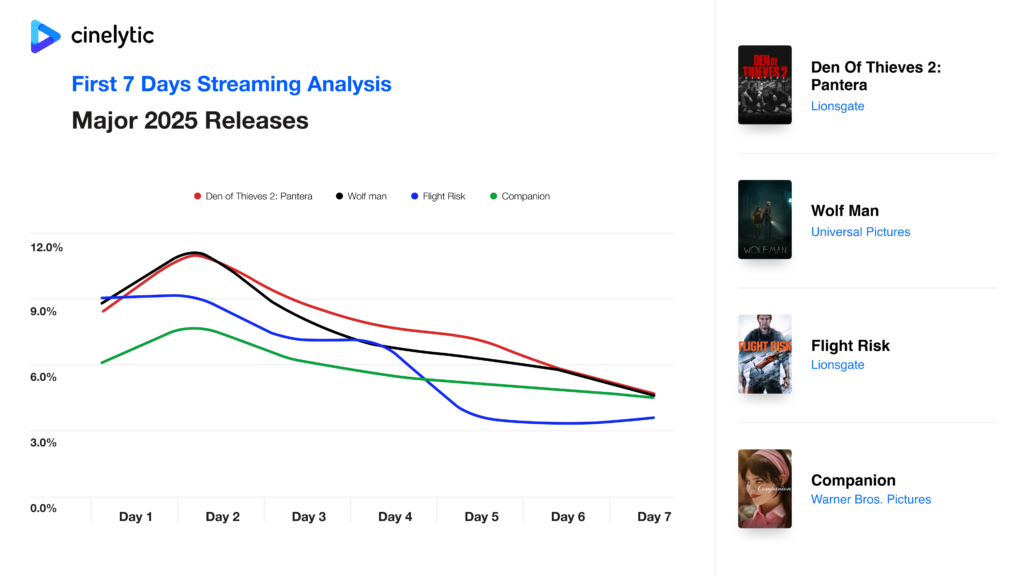

With the theatrical outlook in mind, it is also worth assessing how major recent releases have performed once they reached the digital window. Using our proprietary streaming demand data which tracks 125m daily peer-to-peer (P2P) transactions worldwide and roughly 35b annually, we evaluated the first seven days of digital performance for six major late-2025 and early-2026 theatrical releases: ANACONDA, MARTY SUPREME, GREENLAND 2: MIGRATION, 28 YEARS LATER: THE BONE TEMPLE, MERCY, and SHELTER:

ANACONDA delivered the strongest performance, averaging 8.1% viewing market share capture against all competing and available titles, and peaking above 10% on Day 2 before gradually declining throughout the week. The recognizable legacy IP combined with a beloved lead comedic cast and creature feature premise likely contributed to both strong theatrical awareness and continued streaming engagement.

MERCY performed nearly identically with an 8.0% weekly average and a Day 2 peak just over 10%. Despite being critically panned and underperforming theatrically worldwide, the combination of a familiar action thriller concept and Chris Pratt’s star power encouraged audiences to give the film a chance once it arrived on streaming.

28 YEARS LATER: THE BONE TEMPLE averaged 7.4% across the week after opening near 9.5% on Day 1. As the only title tied to a major franchise, early streaming interest was expected. However, the film significantly underperformed theatrically relative to its predecessor, which was released just seven months ago. The short gap between installments may have led some audiences to feel the follow-up arrived too soon, opting instead to wait and watch it at home.

The remaining titles formed a second grouping. MARTY SUPREME averaged 6.7%, peaking above 8% on Day 2 before steadily declining. As the highest grossing A24 release driven by Timothée Chalamet’s star power and one of the most aggressive marketing campaigns in recent memory, much of the audience likely rushed to see the film in theaters, leaving less immediate demand for home viewing.

SHELTER averaged 6.9% and maintained relatively steady engagement before tapering late in the week. While the film underperformed in theaters relative to typical Jason Statham action releases, that style of straightforward action often performs well on streaming where audiences gravitate toward familiar and easily watchable titles.

Finally, GREENLAND 2: MIGRATION recorded the lowest weekly average at 6.1%. Arriving six years after the original with minimal marketing and releasing the same day on streaming as ANACONDA, the film struggled to generate the same level of attention both in theaters and at home.

All to Say

Taken together, these early indicators highlight the evolving balance between theatrical and streaming performance. While 2025 proved to be a challenging year, and Q2 2026 is currently projected to show modest year-over-year decline, the broader trajectory remains positive.

At the same time, streaming performance demonstrates that films which fall short theatrically can still generate meaningful audience engagement once they reach the home window. Titles such as 28 YEARS LATER: THE BONE TEMPLE and MERCY illustrate how recognizable IP or star power can drive strong digital viewing even after underwhelming theatrical runs. Others, like ANACONDA, occupy a middle ground, performing solidly at the box office relative to budget while also sustaining strong digital engagement.

Conversely, certain films achieve the majority of their audience during the theatrical window itself. MARTY SUPREME, driven by awards buzz and strong pre-release momentum, concentrated much of its demand in theaters, leaving less residual demand for repeat viewing on streaming, especially due to its 149-minute runtime. And as always, some titles struggle to find a meaningful audience across either window, as seen with GREENLAND 2: MIGRATION and SHELTER. In short, while theatrical performance remains the primary indicator of industry health, streaming data increasingly reveals where audience demand ultimately settles. Together, these windows reinforce the broader takeaway for 2026: even in quarters where box office growth appears modest or temporarily soft, total audience engagement across platforms continues to support what we already predicted will be strongest theatrical year since the pre-pandemic era.

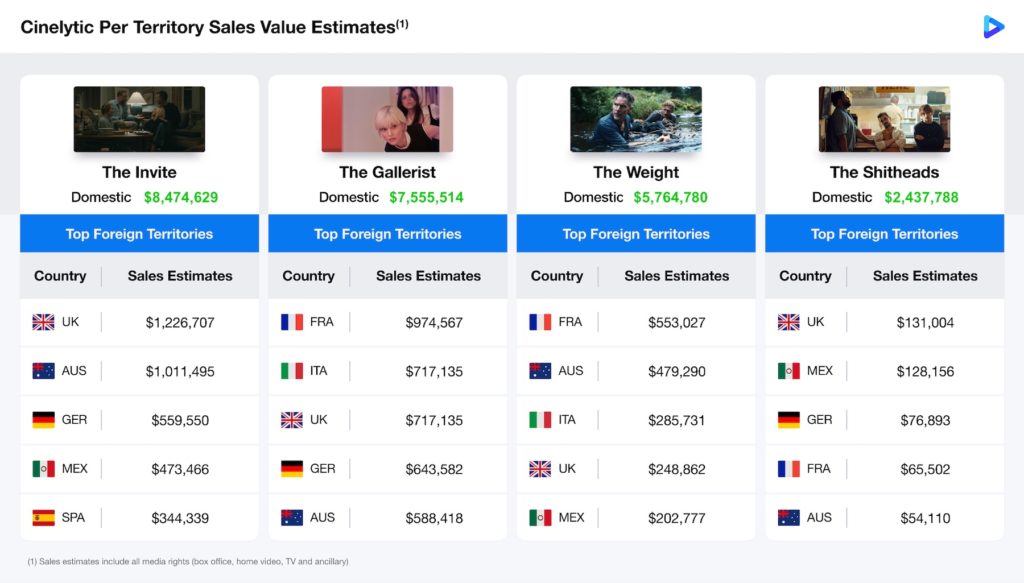

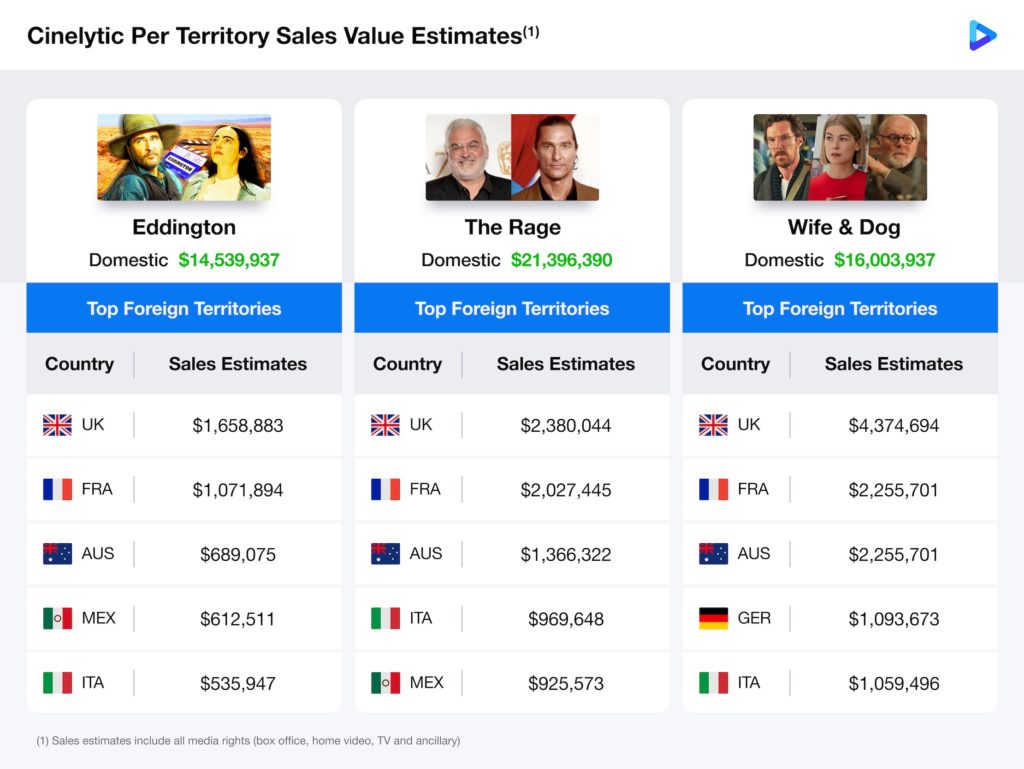

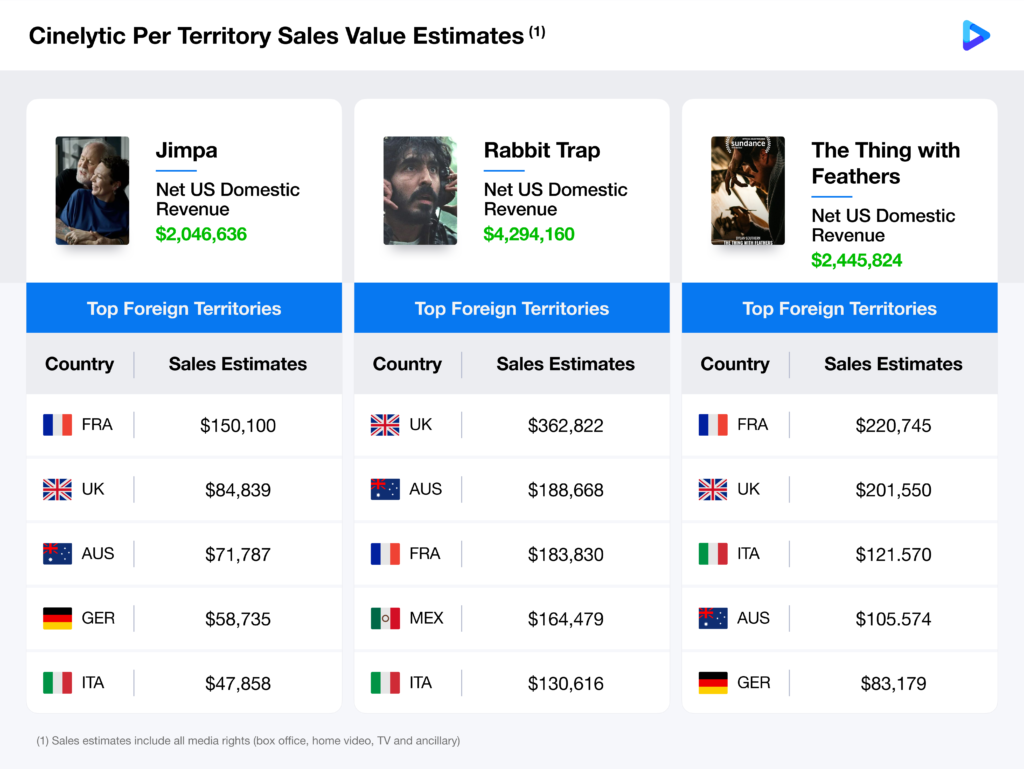

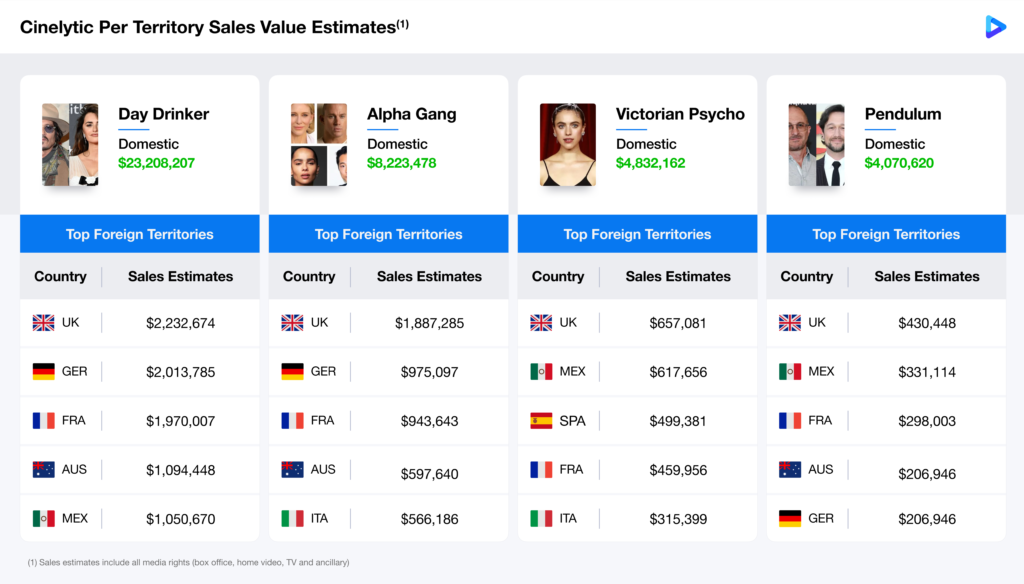

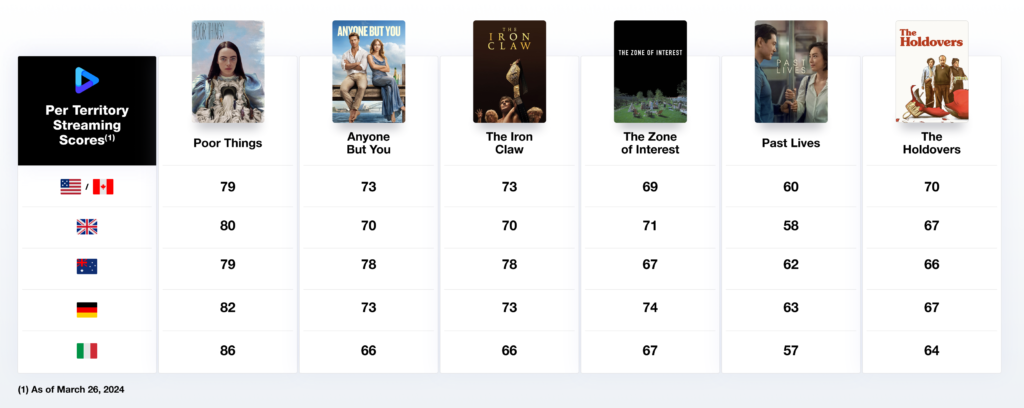

With the 42nd annual Sundance Film Festival just around the corner, we at The Cinelytic Group are again putting our forecasting tools to work, this time spotlighting several upcoming releases attracting attention on the festival circuit as “hot sales titles” seeking distribution at this year’s ceremonies: THE INVITE, THE GALLERIST, THE WEIGHT and THE SHITHEADS.

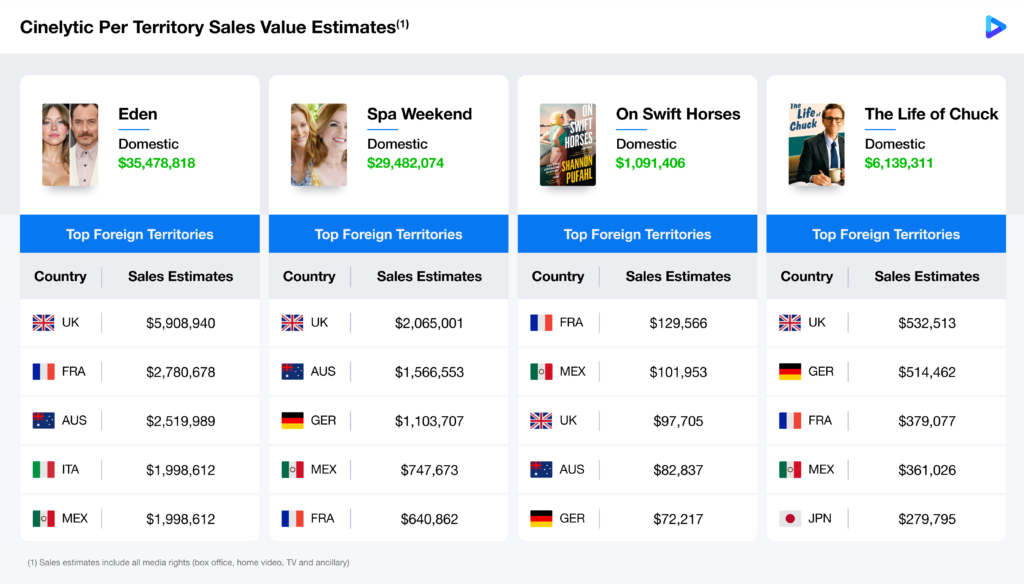

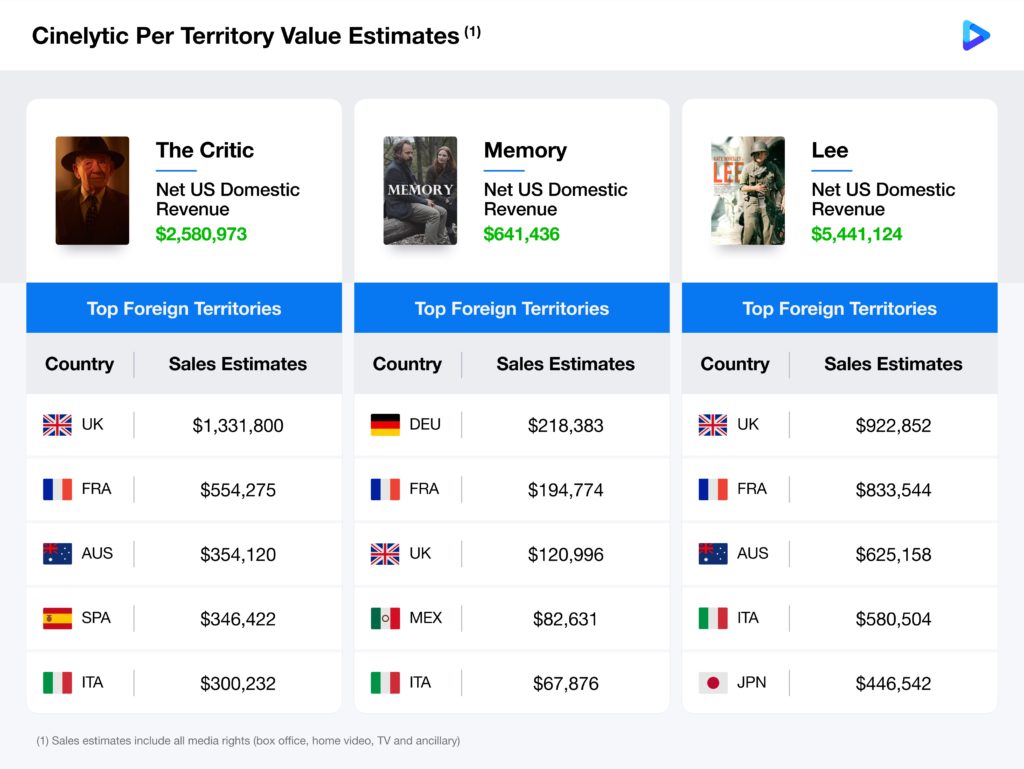

Our signature ROI forecasting, discussed later in these Insights, is particularly valuable for financiers, producers, and equity providers. However, our sales estimates tool offers a different advantage that enables both buyers and sellers at festivals like Sundance to assess the per-territory value of a title across all media rights (box office, home video, TV, and ancillary).

As shown in the graphic below, this tool is especially useful for those in a market setting who are working to determine the appropriate price for each territory’s rights:

From actress-director Olivia Wilde, THE INVITE is a sharp, sex-infused comedy of manners built around a dinner party gone hilariously wrong. Starring Wilde opposite Seth Rogen, Penélope Cruz, and Edward Norton, the film blends Wilde’s keen observational wit with ensemble chaos, positioning it as one of Sundance 2026’s most buzzed-about crowd-pleasers.

THE GALLERIST comes courtesy of BIRDS OF PREY writer/director Cathy Yan, presenting itself as a darkly funny thriller set against the manic spectacle of the Miami Art Basel art world. Anchored by Natalie Portman and Jenna Ortega with help from from Zach Galifianakis, Catherine Zeta-Jones, Sterling K. Brown, Da’Vine Joy Randolph, and Charli XCX, the film skewers market mania with sharp satire and high-wire ensemble energy.

A gritty period thriller from director Padraic McKinley, THE WEIGHT stars Ethan Hawke and Russell Crowe in a Depression-era tale of survival and redemption. Set in 1930s Oregon, the film follows a widowed laborer entangled with gold smugglers and moral peril as he fights to reunite with his daughter.

Rounding out the group is THE SHITHEADS from acclaimed indie filmmaker Macon Blair, a raucous buddy comedy that turns a simple job into mayhem and stars Dave Franco, O’Shea Jackson Jr., and Mason Thames.

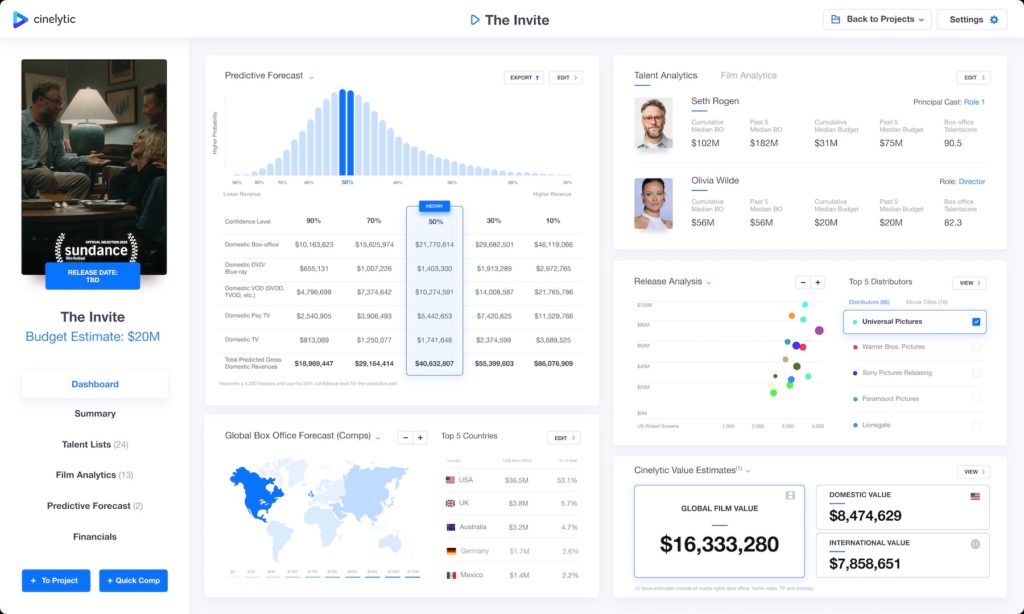

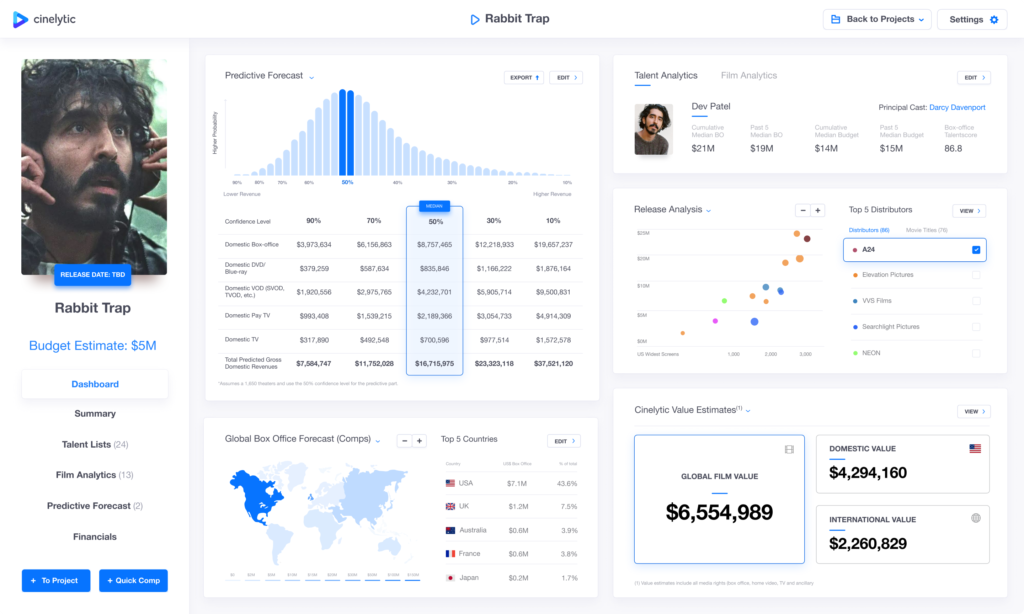

Revenue Forecasting: Spotlight – THE INVITE

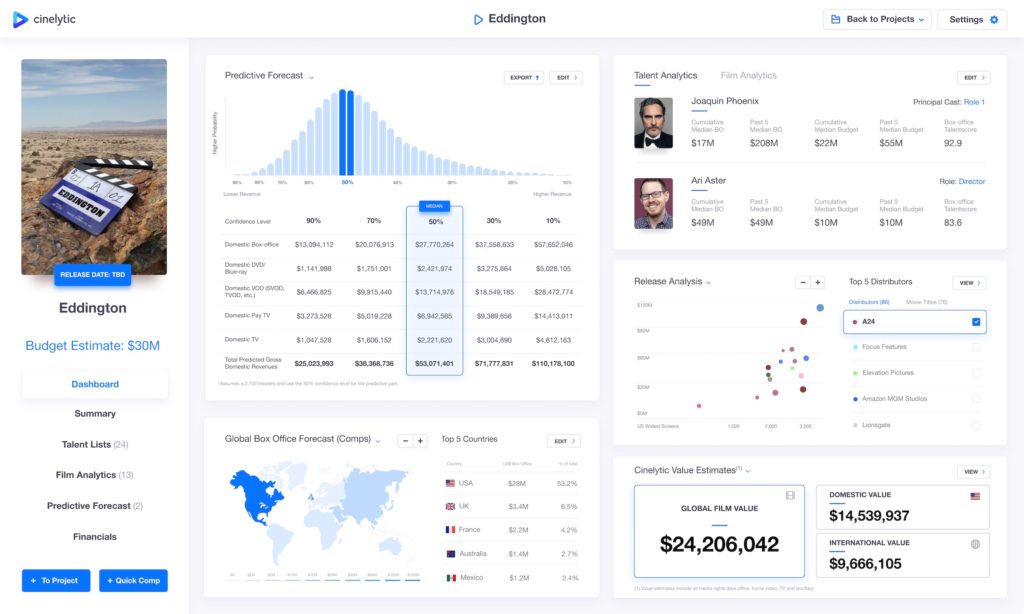

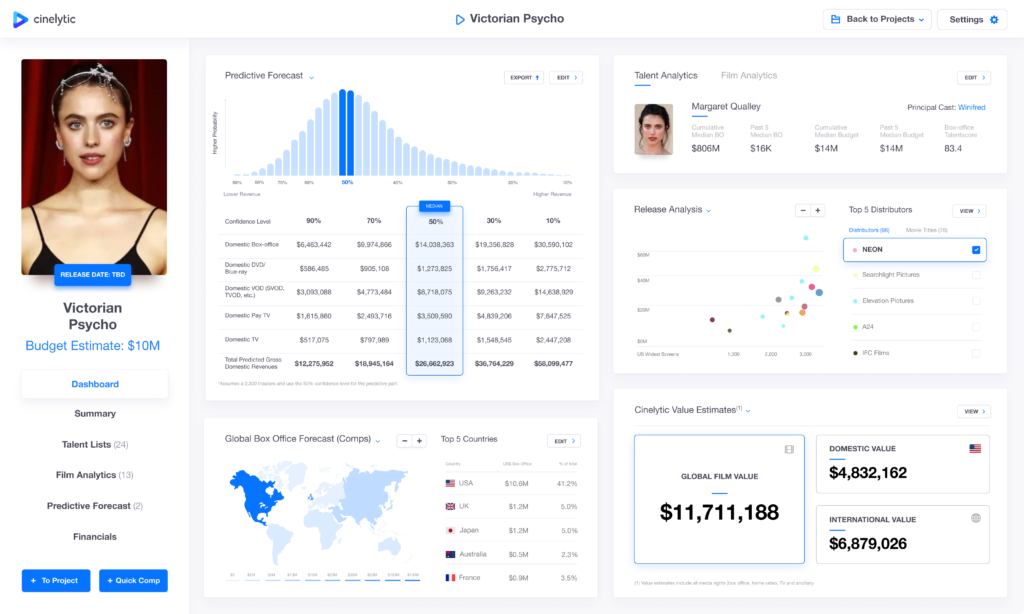

In order to provide a sample of our detailed projections, we chose to highlight THE INVITE and run it through our predictive tool to showcase what may lie ahead for these types of releases in terms of revenue.

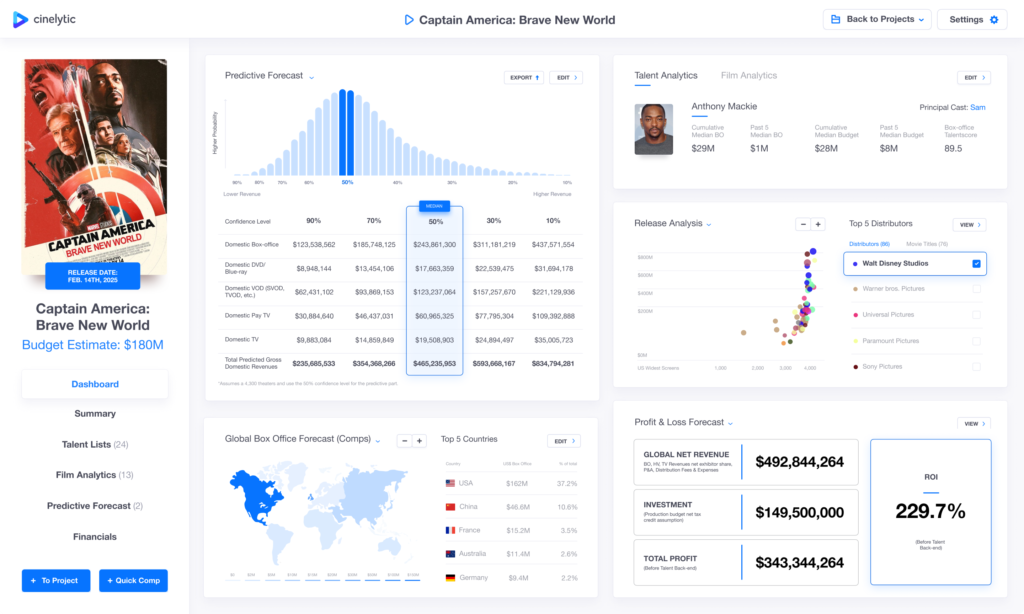

This tool takes into consideration 19 material input attributes to determine a full-performance waterfall, P&L and ROI. We estimated a budget of US$20m, an additional US$32m in global P&A costs and proposed a theatrical release strategy of 2,500 screens with Seth Rogen in the lead. The Cinelytic platform predicts a DBO of roughly US$21.8m, domestic gross revenues (BO, HV, TV) that total US$40.6m, and international gross revenues totaling US$35.7m:

Streaming Success?

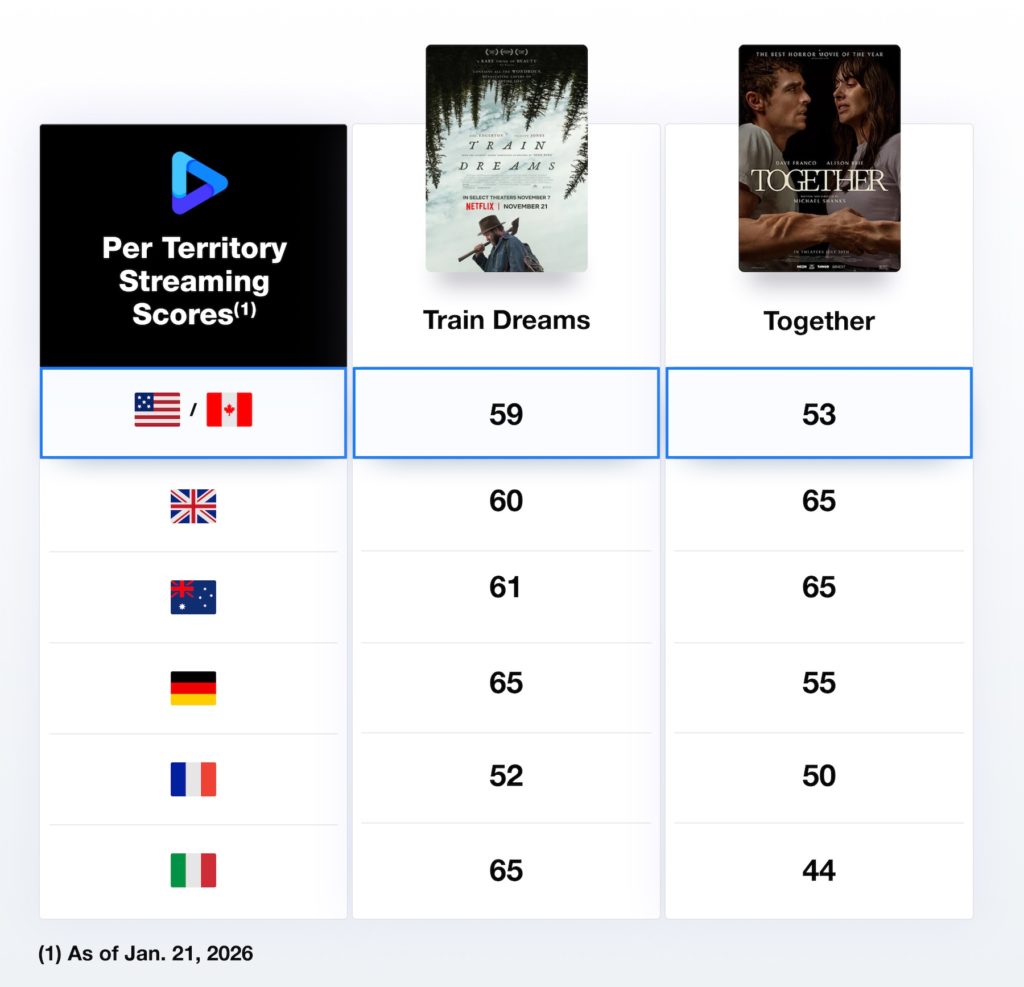

Box office potential is no longer the only driver of sales negotiations at festivals such as Sundance. With streaming platforms (VOD and SVOD) now serving as a major revenue source for festival titles, the focus has shifted toward understanding and analyzing audience consumption patterns.

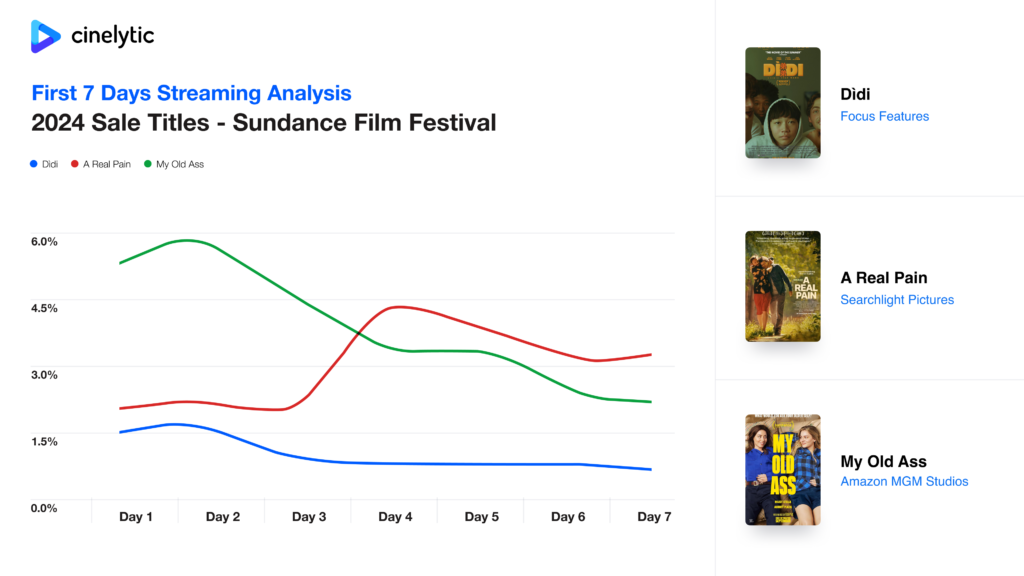

Specifically, we examined both the domestic and international streaming performance of two films that represented arguably the most high-profile sales at least year’s festival: TRAIN DREAMS and TOGETHER. To do this, we utilized our innovative tool, the “Cinelytic Streaming Store,” which predicts and tracks digital content consumption on a per-title basis across various platforms and countries, offering valuable insights through a proprietary viewing score.

This system also removes platform and subscription bias by normalizing performance and isolating true viewing demand rather than raw reach driven by subscriber scale, homepage placement, or algorithmic promotion.

Within that framework, TRAIN DREAMS, bought and released by Netflix, still outperformed Neon’s acquisition TOGETHER, particularly in the domestic market, indicating stronger intentional demand rather than passive consumption. Viewers were more likely to actively choose TRAIN DREAMS, engage more deeply, and follow through on completion, reflecting the impact of awards buzz, critical validation, and prestige positioning.

The softer demand for TOGETHER is consistent with its broader performance profile: despite a roughly US$17m budget and 2,300 screen domestic release, the film grossed only about US$32m worldwide, suggesting limited upside beyond initial curiosity. Taken together, the data reinforces that TRAIN DREAMS generated higher-quality, purpose-driven demand, even after removing platform-related advantages.

All to Say…

Forecasting film performance will never be an exact science, especially in a festival market like Sundance. However, the 2026 titles highlighted here show how data-driven analysis can meaningfully sharpen decision-making around valuation, sales strategy, and release planning. By assessing per-territory demand across all revenue streams, Cinelytic helps buyers, sellers, and financiers better understand where real audience interest exists and how it varies by market.

From Bust to Bounce Back: Our Bottom-Up 2026 Domestic Box Office Forecast

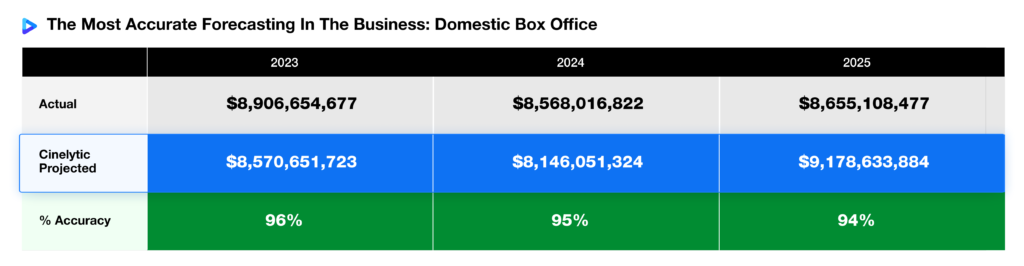

After a year that ultimately did not perform the way most of the industry expected, 2025 closed with little to no meaningful improvement over the year prior. Domestic box office (DBO) totals once again landed at roughly US$8.6b, marking the second consecutive year at that level and underscoring how stubborn the recovery has been despite a fuller release slate and improved theatrical conditions.

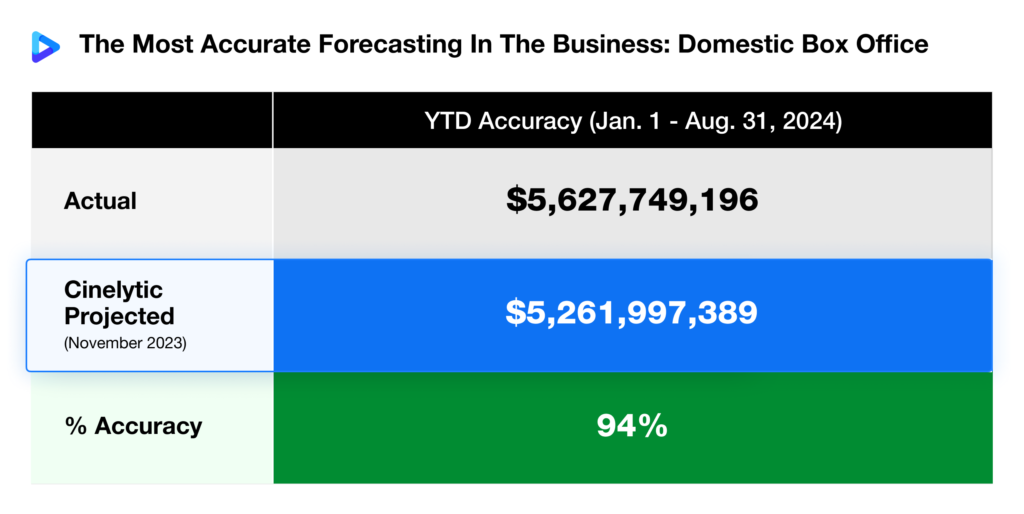

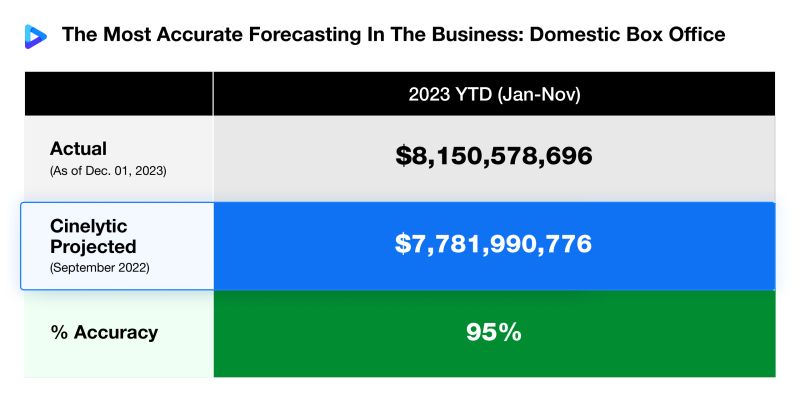

That said, the team at Cinelytic once again stood firmly behind the projections we published at the close of 2024, finishing the year with an overall forecast accuracy of approximately 94%. As the graphic below highlights, this continues a successful trend, with our DBO forecasts consistently landing between 94% and 96% accuracy for three consecutive years, a level of precision we take real pride in as we now turn our focus to the 2026 outlook:

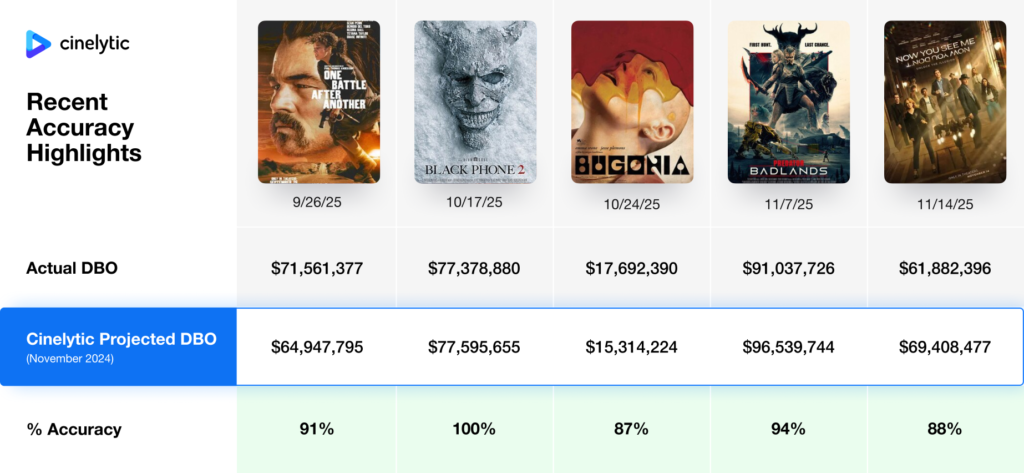

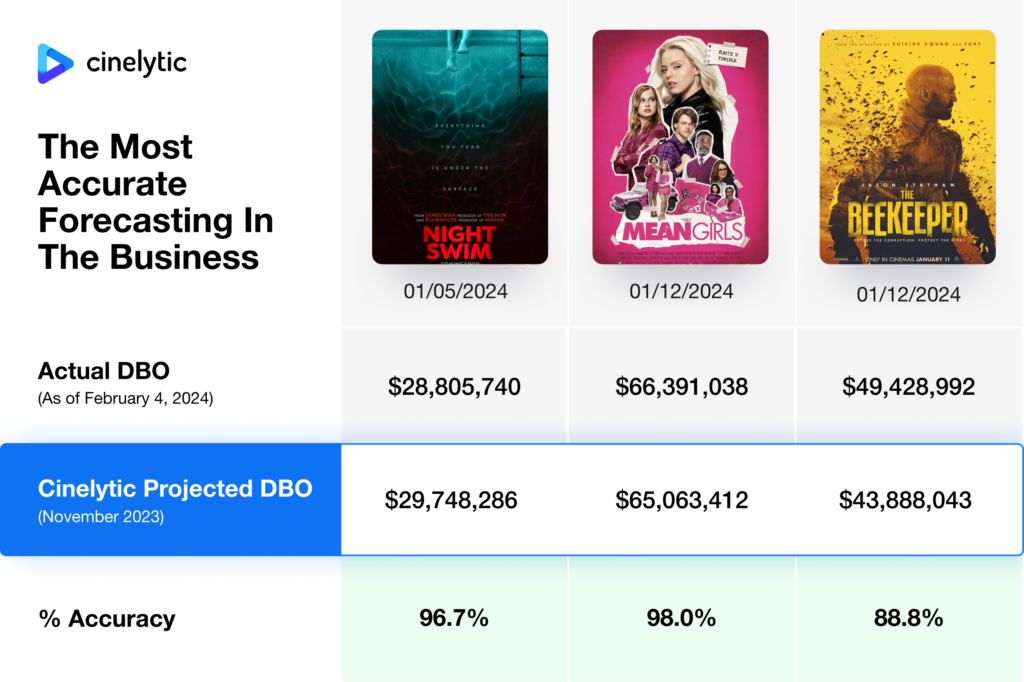

For a sneak peek at how these projections played out on a title-by-title basis, the visualization that follows highlights several recent releases from the final months of 2025, showcasing select accuracy wins as those films completed their theatrical runs:

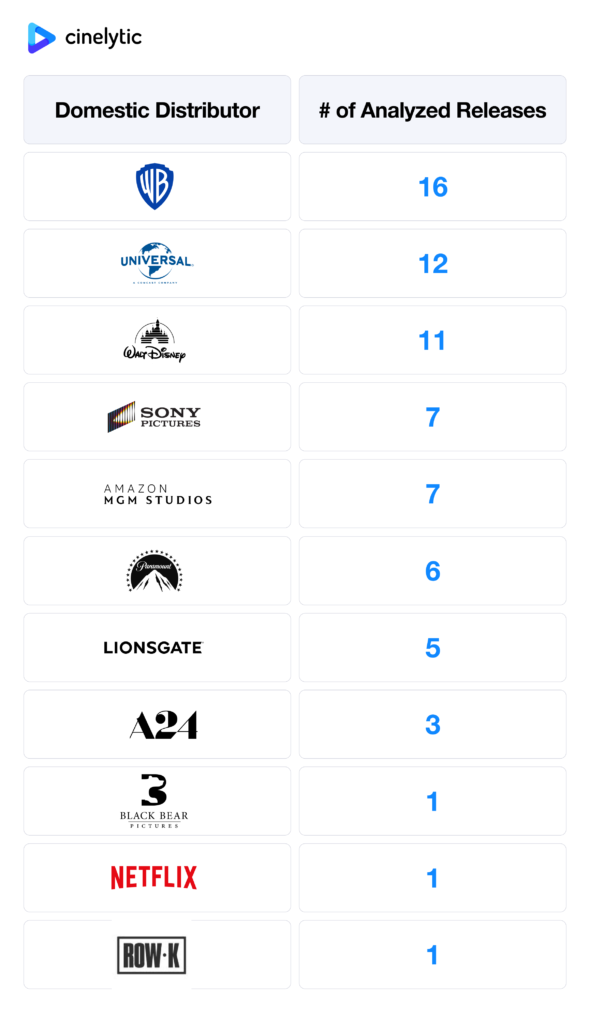

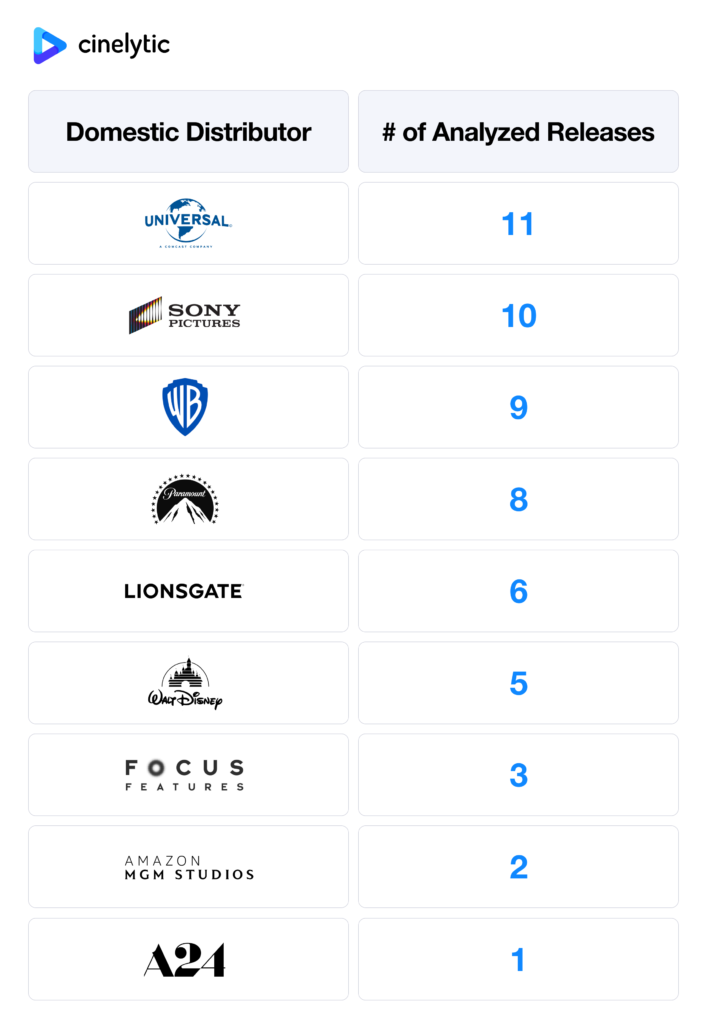

To kick-off the new year, we’ve once again leveraged our powerful bottom-up approach to deliver an early, in-depth look at what’s ahead for the domestic theatrical market. Last November, our team meticulously analyzed the full slate of 2026 major releases, running advanced projections to forecast both annual and monthly DBO performance. This comprehensive analysis covered 70 major titles set for wide release, with a breakdown of releases by distributor as follows:

2026 Forecasts

After 2025 delivered just a 1% increase over the prior year, 2026 is shaping up to represent a far more meaningful step forward. While we do not yet see the market reclaiming the US$10.0b threshold, the trajectory is undeniably improving as we head into what will likely be the strongest DBO year of the post-2020 era.

At Cinelytic, our latest data-driven forecast calls for approximately US$9.6b in 2026 DBO revenue, representing an 11% year-over-year increase from last year’s stagnant results. Our detailed monthly and quarterly projections show momentum building across the year, with Q3 and Q4 projected to deliver the strongest performances for those periods in the post-COVID state of industry. Below, you’ll find the quarterly breakdown alongside a snapshot of recent annual box office performance compared with our 2026 forecast:

How Do We Do This?

The Cinelytic platform harnesses the power of 19 key project attributes, using our proprietary algorithms and machine learning to perform advanced predictive analyses on major titles. As part of our standard approach, we’ve also incorporated late 2025 major releases that are expected to continue driving box office revenue into the first quarter of this year.

This includes factoring in a projected share of early 2026 DBO revenue from high-profile year-end titles such as ZOOTOPIA 2, AVATAR: FIRE AND ASH and MARTY SUPREME, among others.

What’s Fueling the 2026 Recovery?

The projected 11% lift in 2026 is driven by two primary factors. First, several major titles were pulled from the 2025 release calendar at late notice and repositioned into 2026, including high-profile examples such as MORTAL KOMBAT II and THE BRIDE! from Warner Bros. Pictures.

More importantly, however, 2026 marks a meaningful return of large-scale, historically proven IP and franchise filmmaking. This includes a notable resurgence from Marvel, which has not delivered a true breakout hit since DEADPOOL & WOLVERINE in 2024, but returns this year with SPIDER-MAN: BRAND NEW DAY and AVENGERS: DOOMSDAY, both backed by the full force of Disney’s global marketing engine and franchises that rank among the highest-grossing of all time.

The slate is further bolstered by a deep bench of recognizable, high-upside titles such as THE SUPER MARIO GALAXY MOVIE, SCREAM 7, SUPERGIRL, THE DEVIL WEARS PRADA 2, THE MANDALORIAN AND GROGU, TOY STORY 5, MINIONS 3, a live-action MOANA, JUMANJI 3, and DUNE: PART THREE.

Complementing these franchises is a strong lineup of large-scale, non-franchise films generating strong early momentum from elite filmmakers, including PROJECT HAIL MARY from Phil Lord and Chris Miller, DISCLOSURE DAY from Steven Spielberg, and THE ODYSSEY from Christopher Nolan, just to name a few.

Taken together, this mix of delayed tentpoles, franchise-heavy releases, and premium original filmmaking underpins our confidence in a materially stronger DBO performance in 2026.

All to Say…

As the industry moves deeper into a data-driven era, the divergence between intuition-led forecasting and analytically grounded decision-making has never been clearer. In an environment defined by shifting audience behavior, evolving release strategies, and heightened financial scrutiny, tools that can deliver consistent, transparent, and repeatable insights are no longer optional.

At The Cinelytic Group, our ability to model performance from the ground up, validate forecasts with proven accuracy, and adapt in real time to market changes is what allows our partners to plan with confidence. As 2026 shapes up to be a pivotal year for theatrical recovery, rigorous analytics will remain essential to separating signal from noise and turning opportunity into measurable results.

If you’ve opened any news or social media recently, you’ve likely seen all the headlines that have dominated the industry conversation. The story is everywhere, and rather than rehash what’s already been exhaustively covered, we’ll keep our commentary light here.

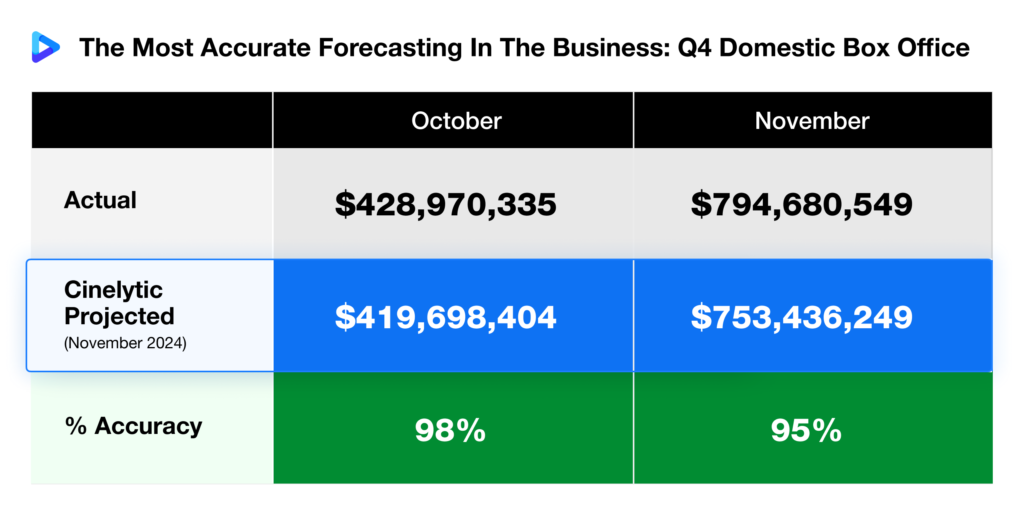

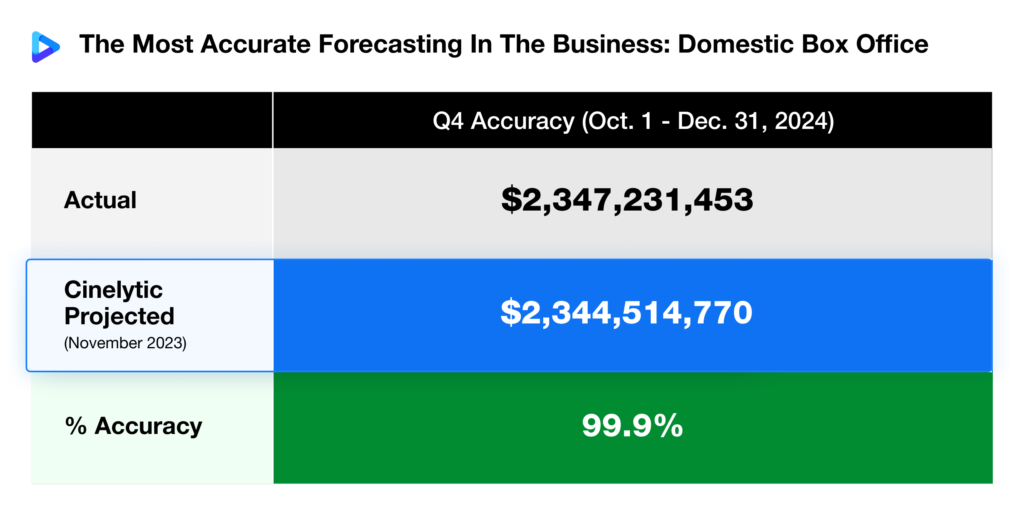

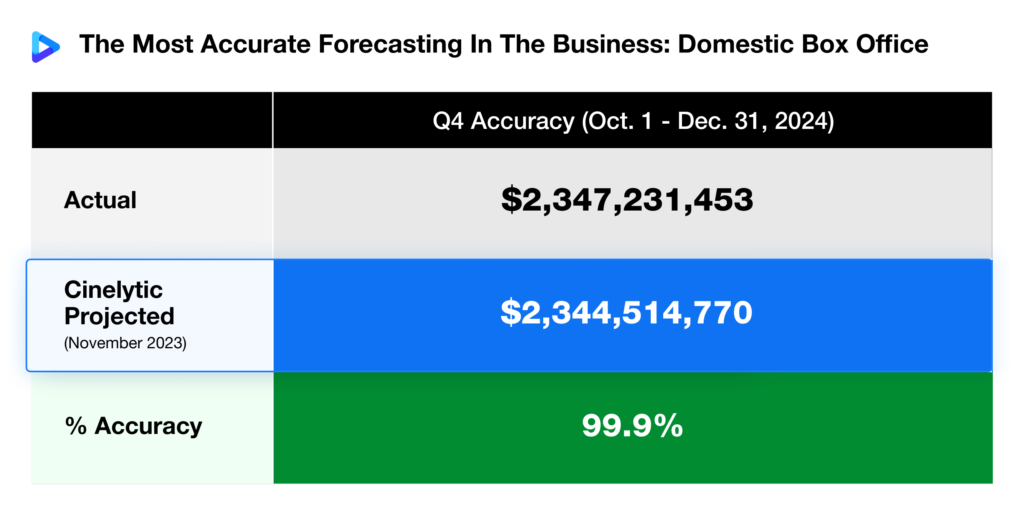

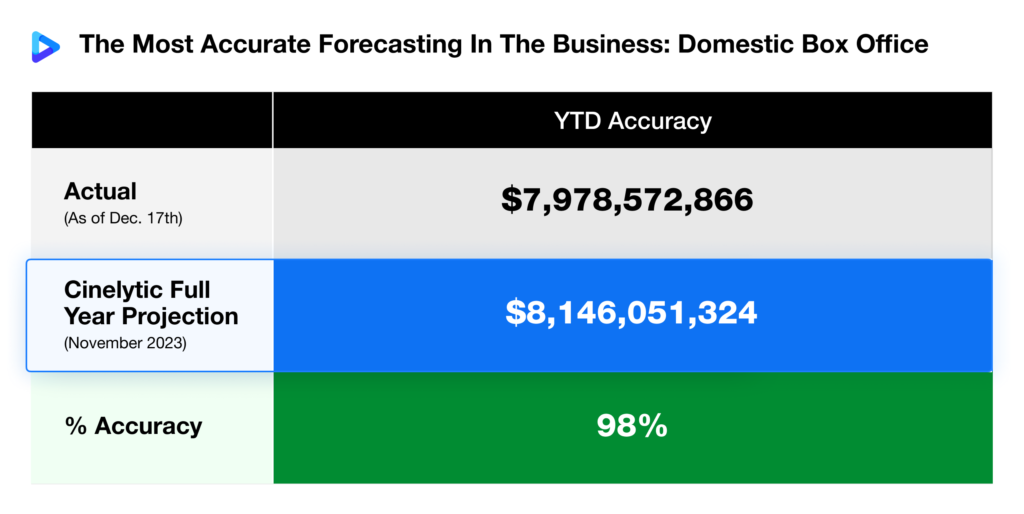

But before circling back to the broader Netflix vs. Warner Brothers Discovery (WBD) discussion, a quick update on something closer to home. As we enter the final stretch of the year, we wanted to share a brief update on our domestic forecasting accuracy so far in Q4, achieved through The Cinelytic Group’s predictive analytics platform, which projected the entire 2025 theatrical slate back in November 2024.

This early-stage forecasting model enables accurate predictions not only for domestic and global box office, but also for home entertainment and television revenues, offering studios, distributors, and financiers a powerful, multi-layered decision-making tool well ahead of release.

As the graphic below illustrates, our projections for the first two months of the quarter have been extremely strong, averaging 96% accuracy:

Rather than repeating the details of a historic potential acquisition, we thought it would be more interesting (and more fun) to look at how Netflix and WBD have actually performed thus far this year in the streaming ecosystem.

In the graphics below, we evaluated and compared the streaming performance of both original films and television series from each company using our proprietary OTT demand data.

This dataset captures approximately 125 million digital content consumption transactions per day worldwide, aggregating to roughly 35 billion annually, offering a clear window into global audience behavior and IP preference.

Importantly, our methodology removes platform bias. We do not rely on subscriber counts or self-reported metrics such as total minutes viewed, which tend to disproportionately favor longer-form content or platforms with larger installed user bases. Instead, we normalize consumption behavior across all major streaming platforms, isolating actual consumer demand during each title’s peak performance week.

This approach enables a true apples-to-apples comparison, regardless of platform size, exclusivity, or release strategy, and better reflects a title’s cultural and commercial resonance.

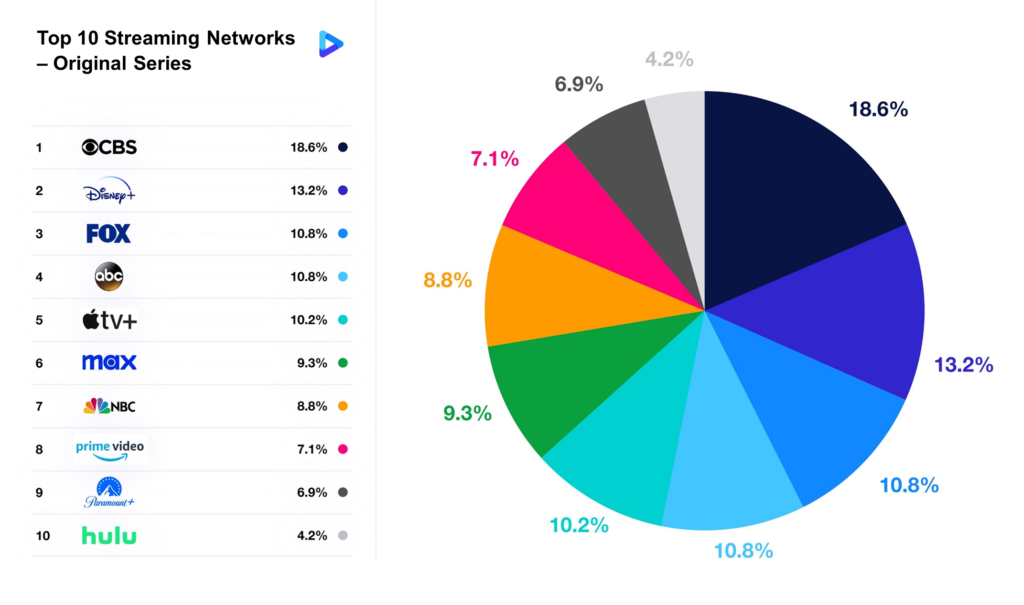

Let’s start with television

As shown above, Netflix’s standout television performers included the first part of the final season of STRANGER THINGS, WEDNESDAY, and breakout critical darling ADOLESCENCE. Counting titles not shown, Netflix logged 13 series that ranked within the Top 100 for the year thus far.

WBD, by comparison, placed 16 total titles, benefiting from a multi-channel distribution footprint that extends beyond HBOMax to include Adult Swim, TNT and TBS. Their key highlights included THE LAST OF US, RICK AND MORTY, and THE WHITE LOTUS.

The summary graphic below illustrates the cumulative impact of each company across episodic television on digital platforms. While WBD’s diversified channels drive volume, Netflix holds a noticeable overall lead, one that is likely to widen further with upcoming debuts before year-end, including the next season of EMILY IN PARIS and Part II of the STRANGER THINGS finale:

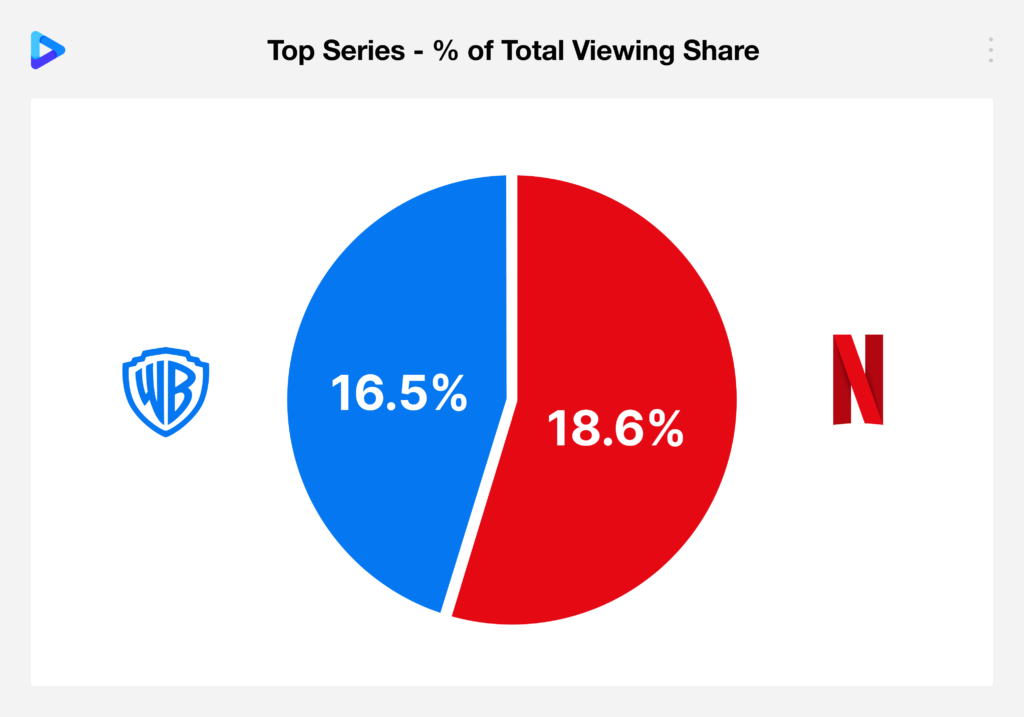

Netflix’s 18.6% makes it the top performing digital distributor of TV series, while WBD ranks third and just behind Apple TV+.

Films: A Much Tighter Race

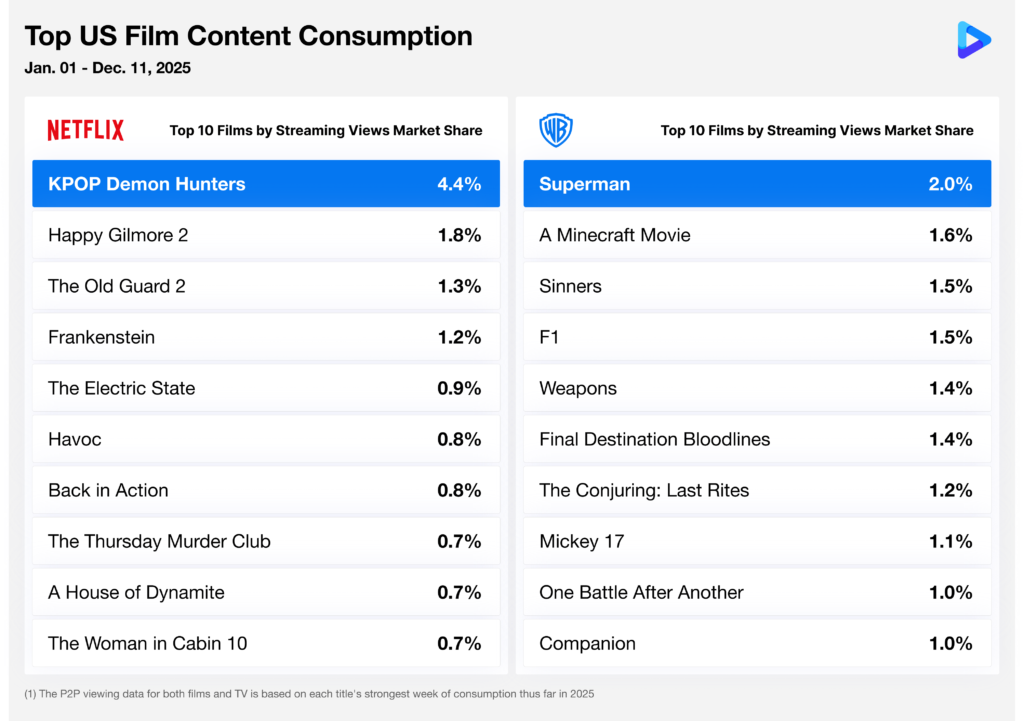

Turning to films, Netflix and WBD each placed exactly 10 among the Top 100 most-watched titles of the year thus far.

Netflix achieved what is widely recognized as the most streamed digital film of the year across all platforms, KPOP DEMON HUNTERS, alongside strong performers such as HAPPY GILMORE 2 and FRANKENSTEIN.

WBD, meanwhile, found significant streaming success despite substantial theatrical runs for all of the titles shown. Highlights included SUPERMAN, SINNERS, ONE BATTLE AFTER ANOTHER and F1, demonstrating continued audience appetite for premium theatrical IP once it transitions to digital platforms. F1’s performance is particularly notable given that this impact was generated prior to the film’s Apple TV+ debut just last week; viewing on Apple TV+ this late in the year is unlikely to surpass the scale of its original digital release as a WBD title, underscoring the strength of its initial streaming run:

The summary graphic below suggests that WBD currently holds the edge in film performance. However, context matters. WBD has no remaining major film titles scheduled for digital release before the end of December. Netflix, by contrast, continues to benefit from occasional breakout films—event-level titles that can meaningfully outperform on an individual basis, as seen earlier this year with K-POP DEMON HUNTERS. That said, Netflix’s film performance has been less consistent across genres, while WBD’s broader slate strength and IP diversity have driven more reliable aggregate results, allowing WBD to maintain its current position in the rankings.

Looking ahead, Netflix is positioned to regain momentum before year-end with the recent release of the third entry in the highly popular KNIVES OUT franchise, which is already projecting strongly and is expected to push Netflix ahead in the final weeks of December:

As it stands, this puts WBD in third place behind Walt Disney Studios in second and Universal Pictures in the top spot, with Netflix close behind in fourth and ahead of Paramount and Sony.

All to Say…

Taken together, this snapshot underscores why the broader industry conversation around a potential Netflix and WBD combination has captured so much attention. On paper, the aggregation of their respective film and television portfolios would represent an unprecedented concentration of premium IP and audience reach, one that would almost certainly eclipse competitors in total market share across both episodic and feature content on digital platforms. At the same time, the data reinforces a more nuanced reality. While it is no surprise that Netflix is likely to outperform WBD overall on streaming this year, a normalized view of performance reveals that the gap—particularly in film—is narrower than prevailing narratives often suggest. When assessed against the full competitive landscape rather than in isolation, Netflix and WBD display distinct strengths, release strategies, and consistency profiles that shape their real-world impact. Evaluating these dynamics through a standardized lens provides clearer insight into where each company truly stands today, how they compare to peers, and why disciplined, data-driven analysis remains essential as the industry continues to evolve.

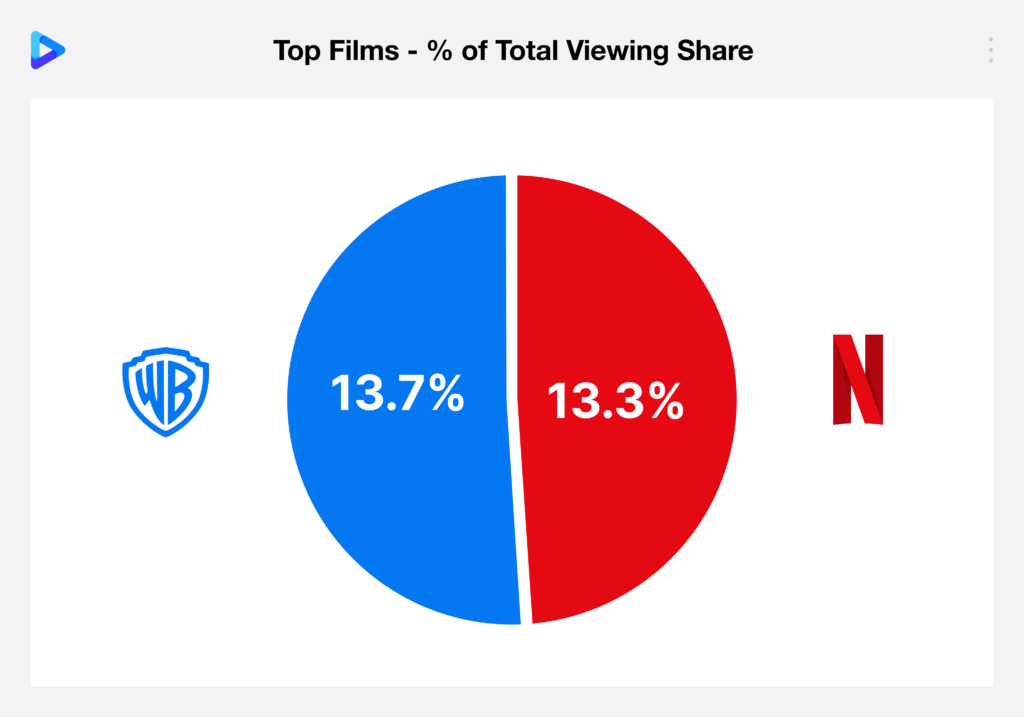

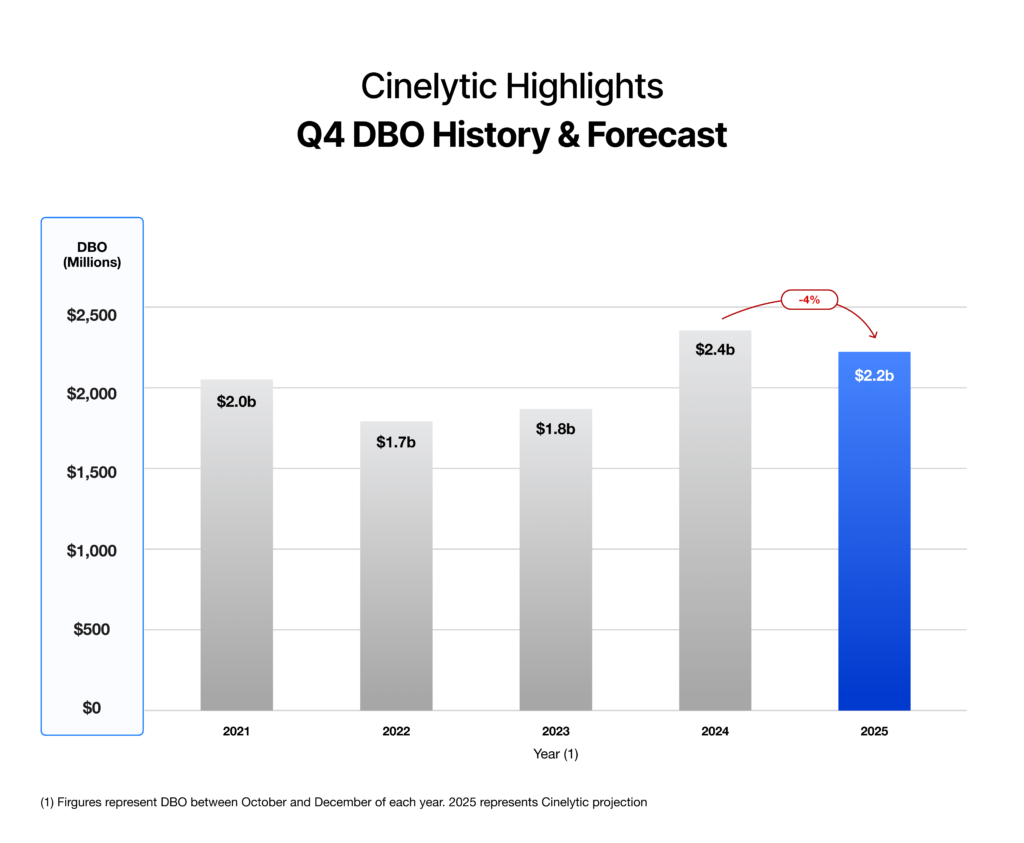

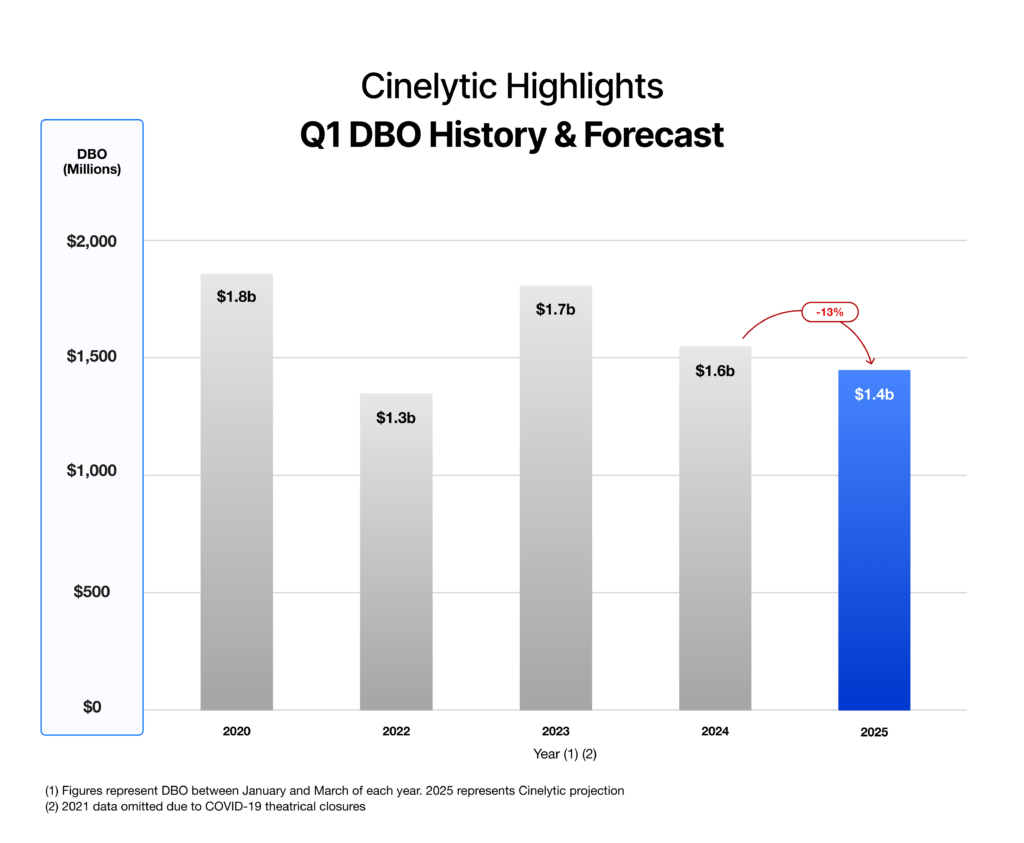

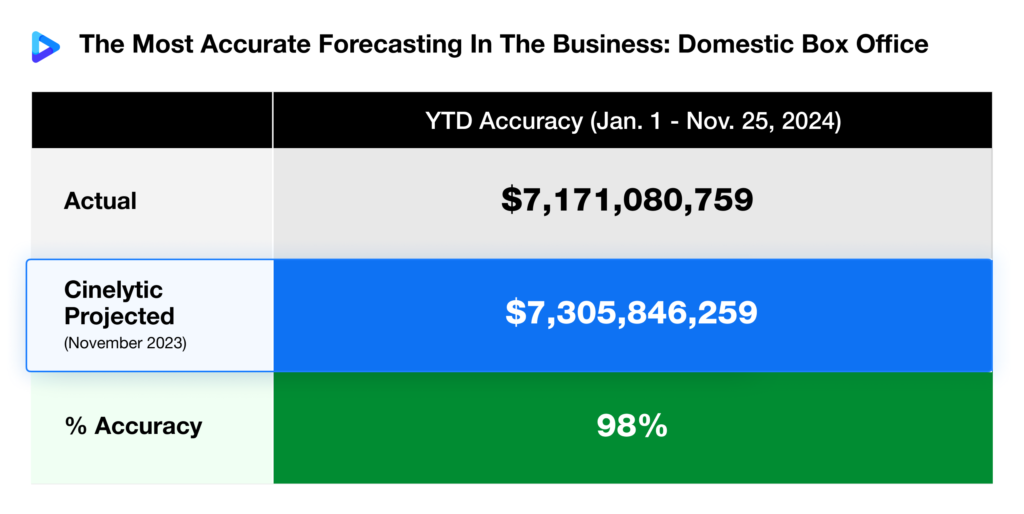

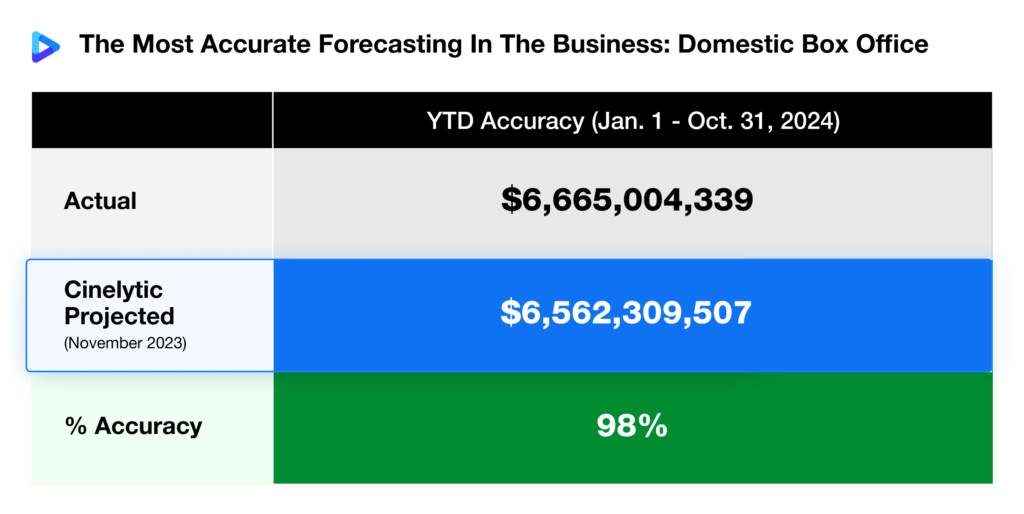

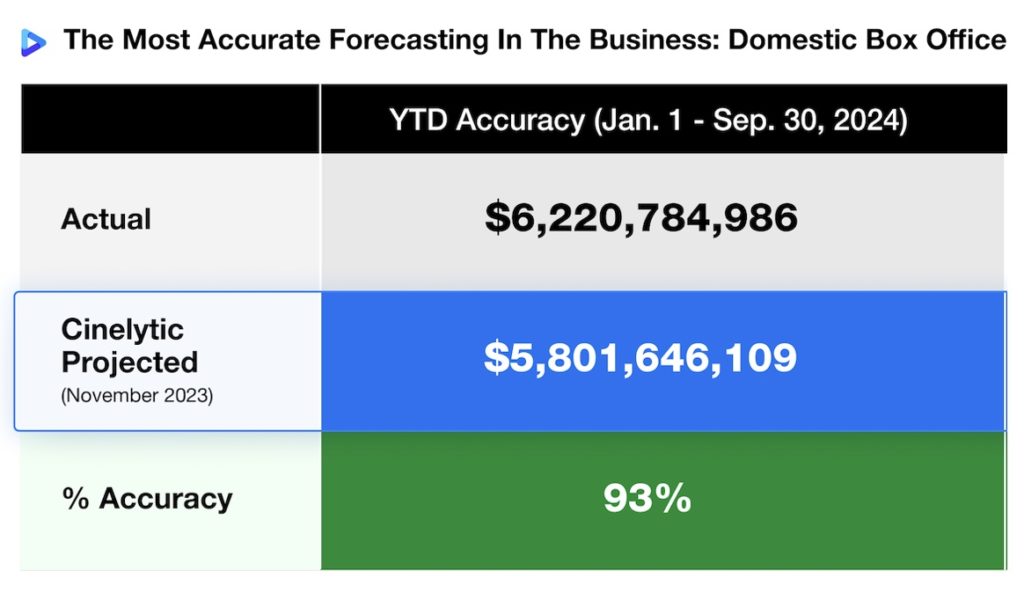

All year long we have been benchmarking the predictions we published at the end of 2024 for the 2025 film slate. With a historically low October domestic box office (DBO) now closed and totals finalized, it is worth noting that Cinelytic’s forecasts for the month landed at a 98% accuracy rate, almost exactly one year after they were published. The chart below highlights just how closely actual performance aligned with our original projections:

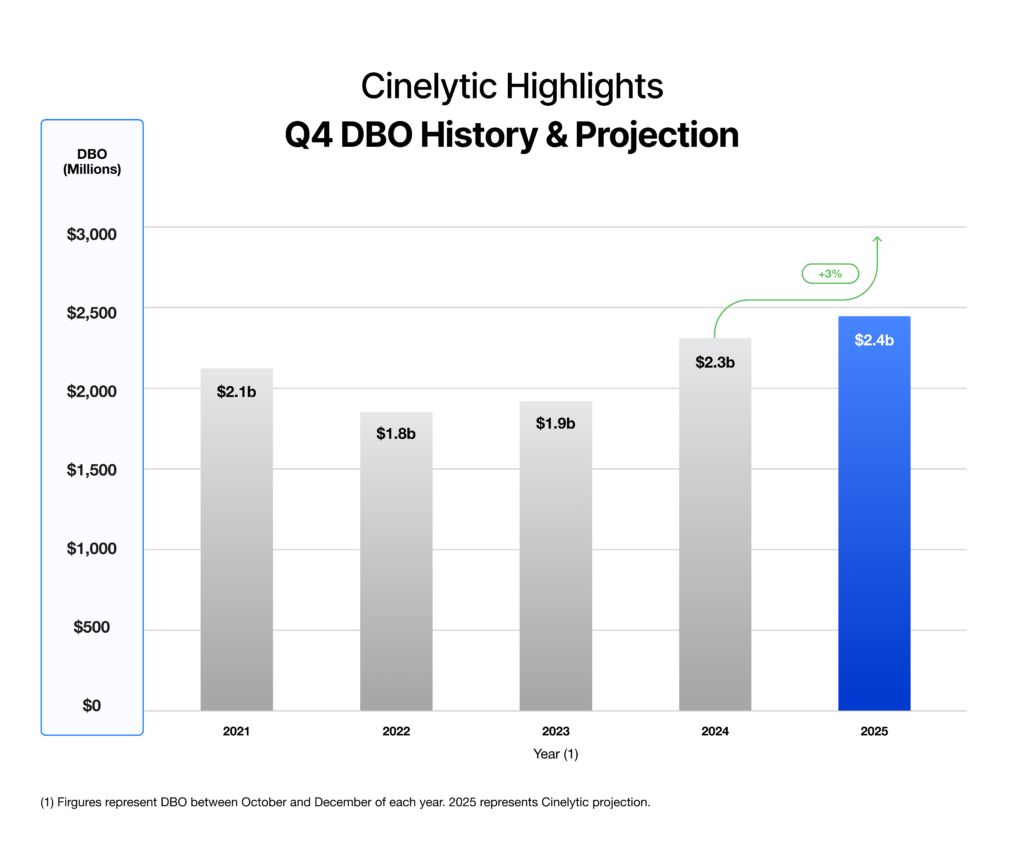

As we move into the final quarter of the year, many will recall the Q4 DBO outlook we shared in our September Insights. At that time, we projected roughly US$2.4b in total Q4 revenue, a modest 3% improvement over the same period in 2024.

Since then, several highly anticipated releases have shifted into 2026. Major projects, including THE BRIDE! and MORTAL KOMBAT II from Warner Bros. Pictures, were among the moves forcing a recalibration of calendar expectations. As a result, we have updated our Q4 2025 forecast to just over US$2.2b, instead representing a 4% year-over-year decline:

While this drop is notable, it remains relatively small when compared with the sharp 26% surge in Q4 2024. If anything, the contrast underscores a broader trend. Rather than preparing for big spikes or sudden drops, the industry appears to be settling into a more predictable cadence after several years of volatility. The domestic market may finally be shaping into a post-COVID equilibrium, with fewer extremes and steadier theatrical behavior from both distributors and audiences.

This revised projection also of course affects our total domestic haul for 2025. We originally pegged the year at US$9.35b in box office revenue, a sizable 9.1% increase over a soft 2024. With the slate adjustments, our updated estimate now sits at US$9.18b. The new number still reflects growth, though at a more measured pace of 7.1%.

What About Next Year?

Even with these revisions, 2025 remains positioned to deliver the strongest theatrical performance of the post-COVID era, though not quite to the degree many across the industry had hoped for during earlier planning cycles. The bigger picture may simply be a settling period, where the market rebuilds gradually rather than surging all at once.

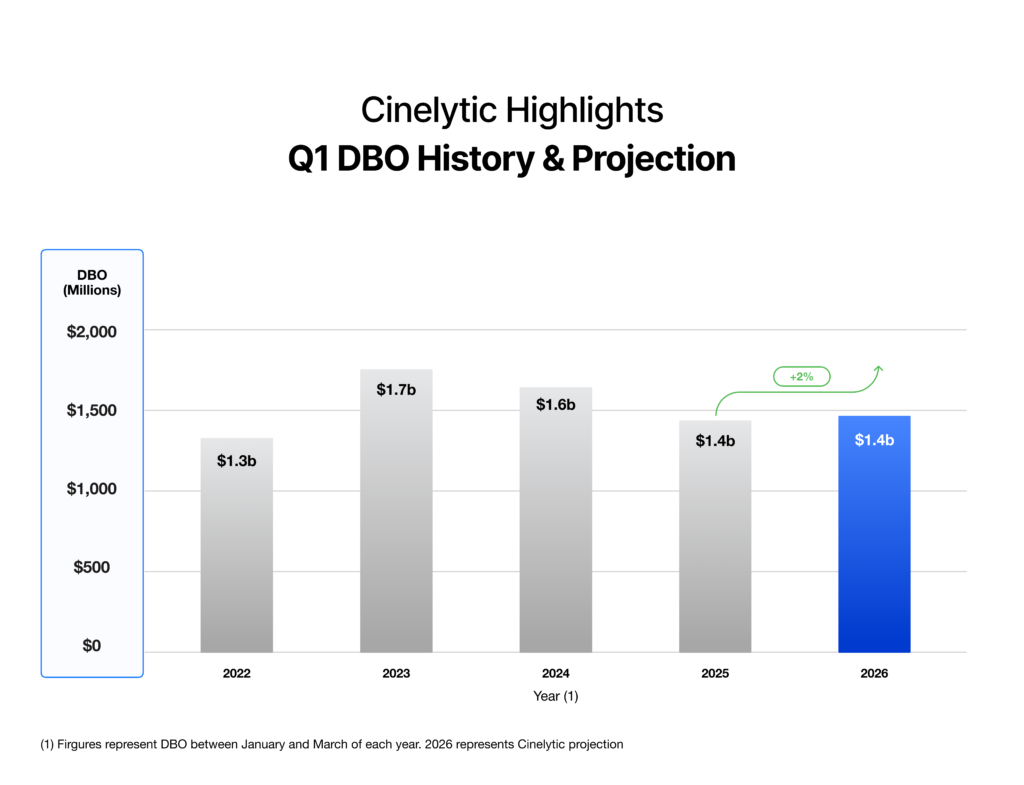

Looking ahead, we ran the Q1 2026 slate through Cinelytic’s predictive forecasting platform, which utilizes AI and 19 key attributes to generate highly accurate models of domestic and global box office projections, along with home entertainment and television revenues.

As shown in the graphic below, our full Q1 forecast for 2026 reflects only a subtle change from the prior year, projecting a 2% increase in DBO totals to just over US$1.4b:

What’s Driving Q1?

The early months of 2026 also mirror the general scenario observed in Q1 2025, not only due to the lack of major franchise tentpoles, but because both quarters benefited from residual box office carryover tied to massive prior releases.

In 2025, that meant continued revenue from titles such as WICKED, MOANA 2 and MUFASA: THE LION KING, all of which helped bolster performance beyond the films actually debuting during the quarter. Similarly, Q1 2026 will see additional earnings from late-year blockbusters including WICKED: FOR GOOD, ZOOTOPIA 2 and AVATAR: FIRE AND ASH, providing a comparable boost to early-year totals.

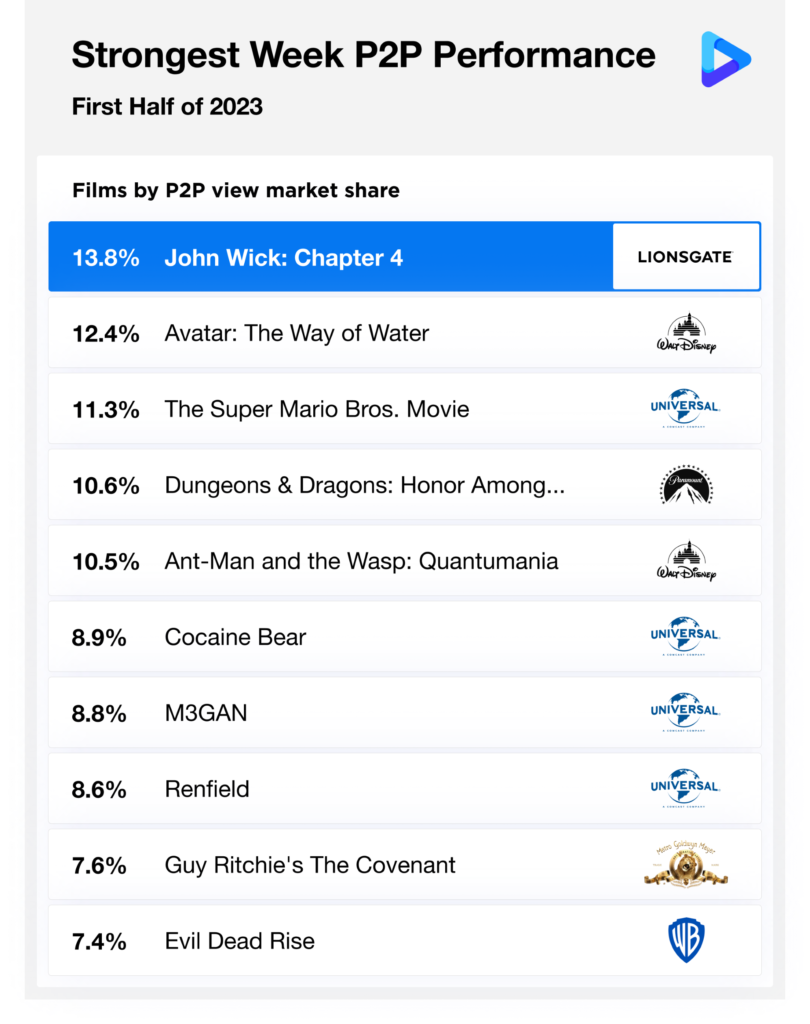

When looking strictly at films that opened during their respective windows, the contrast becomes even clearer. The first quarter of 2024 delivered heavyweights such as DUNE: PART TWO, GHOSTBUSTERS: FROZEN EMPIRE, KUNG FU PANDA 4 and GODZILLA X KONG: THE NEW EMPIRE. A year earlier, audiences were offered franchise staples like ANT-MAN AND THE WASP: QUANTUMANIA, CREED III and JOHN WICK: CHAPTER 4.

The performance narrative for Q1 2025 offers a more useful comparison point. That quarter consisted largely of lower-profile films performing either on target or below expectations, leaving the quarter without a clear breakout success. Examples included DEN OF THEIVES: PANTERA, WOLF MAN, FLIGHT RISK, CAPTAIN AMERICA: BRAVE NEW WORLD, MICKEY 17 and SNOW WHITE.

In the same vein, the first quarter of 2026 features no mega-IP like we saw between 2023 and 2024. While films like 28 YEARS LATER: THE BONE TEMPLE and SCREAM 7 are franchise titles that will appeal to loyal fans, they do not carry the same momentum as the aforementioned films.

Some of the other major releases that may define the quarter include Amazon MGM’s MERCY and PROJECT HAIL MARY, WUTHERING HEIGHTS from Warner Bros., and Pixar’s HOPPERS.

As we look toward Q1 2026, there is cautious optimism that a few less hyped titles could punch above their weights. Projects like GREENLAND: MIGRATION, SHELTER and THE DOG STARS may bring welcome sleeper success if early word of mouth and marketing traction align.

Is This Indeed the New Norm?

With 2025 now tracking to close very near our updated projection and in the US$9.1b range, and with both 2023 and 2024 exhibiting totals within a similarly narrow bracket, it is reasonable to consider that this figure may represent the new stable zone for the domestic theatrical market.

This level reflects roughly a 22% reduction from the averages seen in 2018 and 2019, underscoring the long-term impact of shifting theatrical habits, evolving tastes, streaming competition, and evolving production strategies.

Whether the next few years deliver surprise over-performance or simply reinforce this new threshold, one thing is clear: accurate forecasting and strategic greenlighting will be more important than ever. Tools such as Cinelytic’s AI-powered Predictive Forecasting platform will increasingly guide studios, financiers, distributors and production companies as they assess investment windows, compare ROI benchmarks and build smarter slates in an era of measured growth rather than explosive spikes.Stay tuned for our full DBO Forecast for 2026, which we will be publishing very soon. The data is already telling quite a story.

As this month comes to a close, the film industry is poised to witness what’s tracking to finish as the worst October at the domestic box office (DBO) since 1997 (discounting the 2020 COVID shutdown). That year’s October total came in just above US$381m, while the broader 1997 slate was defined by major blockbusters like MEN IN BLACK and THE LOST WORLD: JURASSIC PARK, with TITANIC on deck to redefine box office history by year’s end.

As the graphic below demonstrates, Cinelytic’s predictive platform continues to show remarkable accuracy in forecasting market outcomes, including this very slowdown, which our models projected back in Q4 2024 as a similarly and historically soft month for theatrical performance:

It wouldn’t be fair to single out October alone, as 2025 has been filled with a wide spectrum of theatrical outcomes. From ambitious tentpoles that missed the mark to steady performers that met expectations and a handful of overachievers that defied the odds, the year so far has delivered no shortage of lessons about audience behavior and release strategy.

Underperformers, On Target and Overperformers

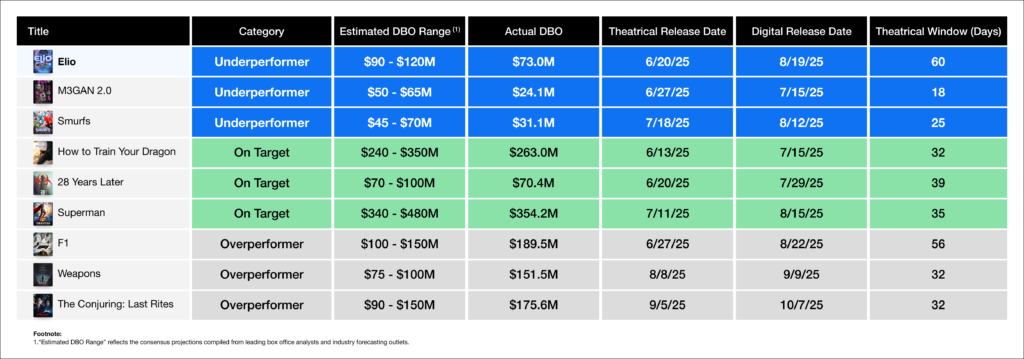

To explore this dynamic further, Cinelytic identified nine high-profile titles released theatrically since June, distributed evenly across three categories based on their actual box office results versus pre-release industry consensus:

Among the underperformers, ELIO struggled to connect with families amid heavy competition and a crowded animated slate, M3GAN 2.0 leaned too heavily on the viral appeal of its predecessor and displayed overconfidence with a borderline genre shift, and the SMURFS reboot failed to overcome brand fatigue despite a family-friendly window.

The on-target performers each fell within expected forecast ranges, driven by strong brand recognition, loyal fanbases, and well-timed marketing pushes.

Meanwhile, the overperformers outpaced expectations thanks to a mix of star power, smart positioning, and franchise momentum that carried them through late summer and into early fall.

It’s worth noting that WEAPONS and THE CONJURING: LAST RITES, both spooky, horror-driven releases, would almost certainly have helped October avoid its “historically bad” label had Warner Bros. held them just a bit longer.

The studio’s reasoning, however, was clear: late-summer windows offered less competition, more premium-screen availability, and the ability to build sustained buzz leading into Halloween rather than competing directly with crowded late-October schedules.

In the end, those strategic early releases performed exceptionally well but also left a noticeable void in what has otherwise been the weakest October in nearly three decades.

Correlation to Streaming

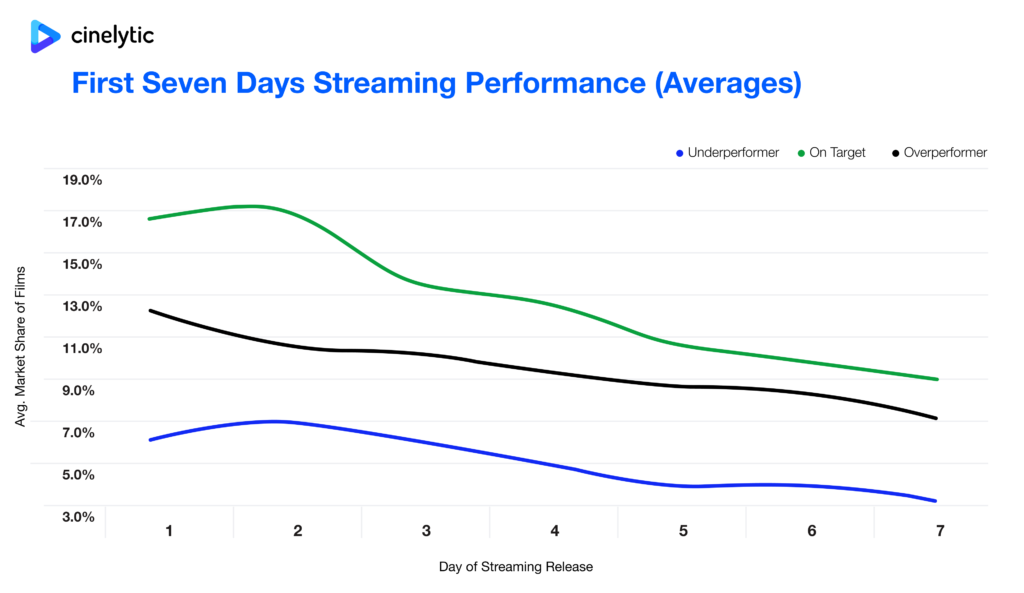

To understand the bigger picture, we turn to streaming. The chart below is powered by Cinelytic’s proprietary Streaming Demand Dataset, which tracks over 125 million daily peer-to-peer (P2P) transactions worldwide. This graphic illustrates digital market share capture during the first seven days of post-release for these nine same titles:

The results reveal an interesting correlation between box office performance and early digital traction. Films that performed on target in theaters achieved the highest first-week streaming capture, averaging 12.8% of total digital market share.

Those that overperformed theatrically still translated well to streaming, though at a lower average of 9.5%, suggesting that much of their audience demand had already been met during their theatrical run.

Meanwhile, underperformers mirrored their box office struggles in the digital space, averaging just 4.9% in their first week.

What are the Key Takeaways?

While this pattern reinforces the idea that films aligning most closely with audience expectations tend to thrive across both windows, the most valuable insight comes from the fact that the theatrical outperformers did not outperform on streaming.

Today’s consumers are highly informed about what films are worth seeing in theaters, at home, or skipping altogether. Going to the cinema is expensive and requires extra effort compared to the comfort and convenience of home viewing. However, audiences still flock to theaters for truly cinematic experiences. These are films that demand a big screen, benefit from the shared energy of a live audience, or deliver that premium theatrical feel. These titles tend to outperform at the box office but often see softer results on streaming, as most interested viewers have already watched them in theaters.

The next tier consists of strong films that offer a positive theatrical experience but aren’t considered “must-see in theaters.” While they draw respectable attendance, many viewers choose to wait for their streaming release, driving strong digital performance as a result. These are films audiences want to see but don’t feel compelled to spend extra money or effort on a theatrical trip.

Finally, there are films that fail to engage audiences either in theaters or at home. These typically suffer from weak execution or concepts that don’t resonate. In an entertainment landscape that is currently crowded with sports, gaming, and social media, consumers are selective with their time, and these titles simply don’t break through.

All to Say…

Ultimately, insights like these underscore why Cinelytic’s platform and suite of tools have become an essential tool for today’s entertainment decision-makers. By unifying real-time box office tracking, audience sentiment, and global streaming demand into a single data-driven ecosystem, Cinelytic empowers studios, streamers, and financiers to move beyond guesswork.

We provide them with the ability to identify optimal release windows, calibrate marketing spending and accurately forecast revenue potential across every platform. In a marketplace where timing, positioning, and audience connection determine success, Cinelytic gives the industry a measurable advantage by turning data into foresight, and foresight into smarter results.

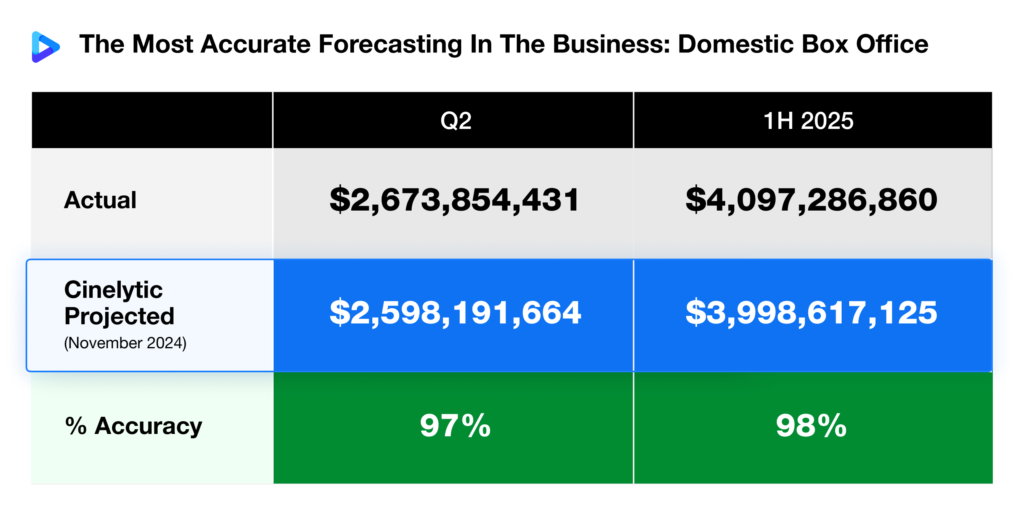

Over the course of this year, we’ve been tracking and revisiting the projections we made at the end of 2024 for the 2025 film slate. Now that the summer box office season has wrapped and the final stretch of releases lies ahead over the next three months, we’d like to share an update on our latest accuracy metrics.

As we await the end of Q3, the graphic below highlights how our Domestic Box Office (DBO) projections have remained remarkably accurate through the first two quarters of the year:

As we head into the final quarter of the year, Cinelytic’s predictive platform anticipates a modest box office lift compared to last year—one that would narrowly surpass 2024’s mark as the most lucrative Q4 since 2019, pre-COVID.

As illustrated in the graphic below, our projections call for a 3% increase in Q4 DBO over 2024, driven largely by a strong year-end showing from Walt Disney Studios. Later in these Insights, we highlight four key titles, each poised to leverage established intellectual property (IP) and the holiday season to extend the ongoing trend of franchise-driven success:

This projected 3% increase may appear modest, especially when compared with the prior year’s 26% surge in Q4 earnings. This contrast further reinforces the notion that the industry is beginning to stabilize into a “new norm” for DBO performance in the post-COVID era—at least for the near future.

Looking at historical context, when comparing the average Q4 performance from the two years prior to the pandemic (2018–2019) with the last two years (2024–2025, inclusive of our projections), revenues are down 19%. This decline closely aligns with the 23% drop in full-year DBO averages across those same periods.

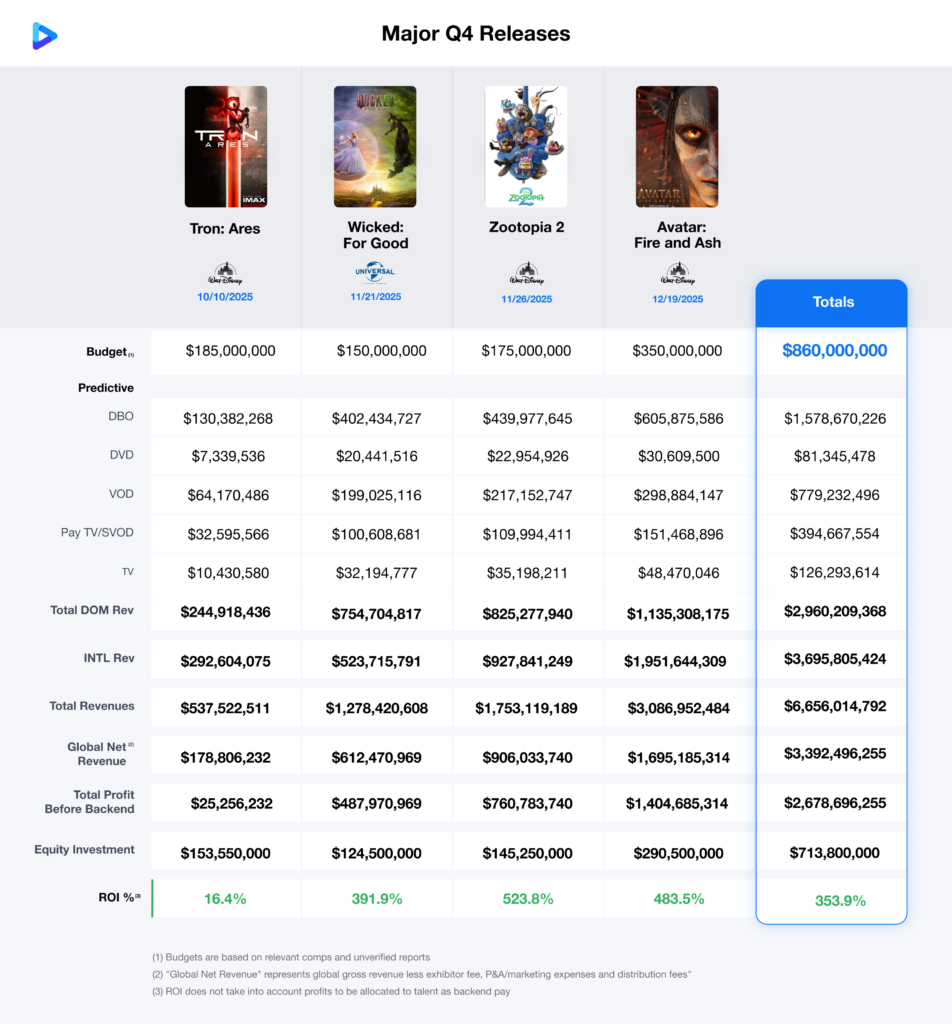

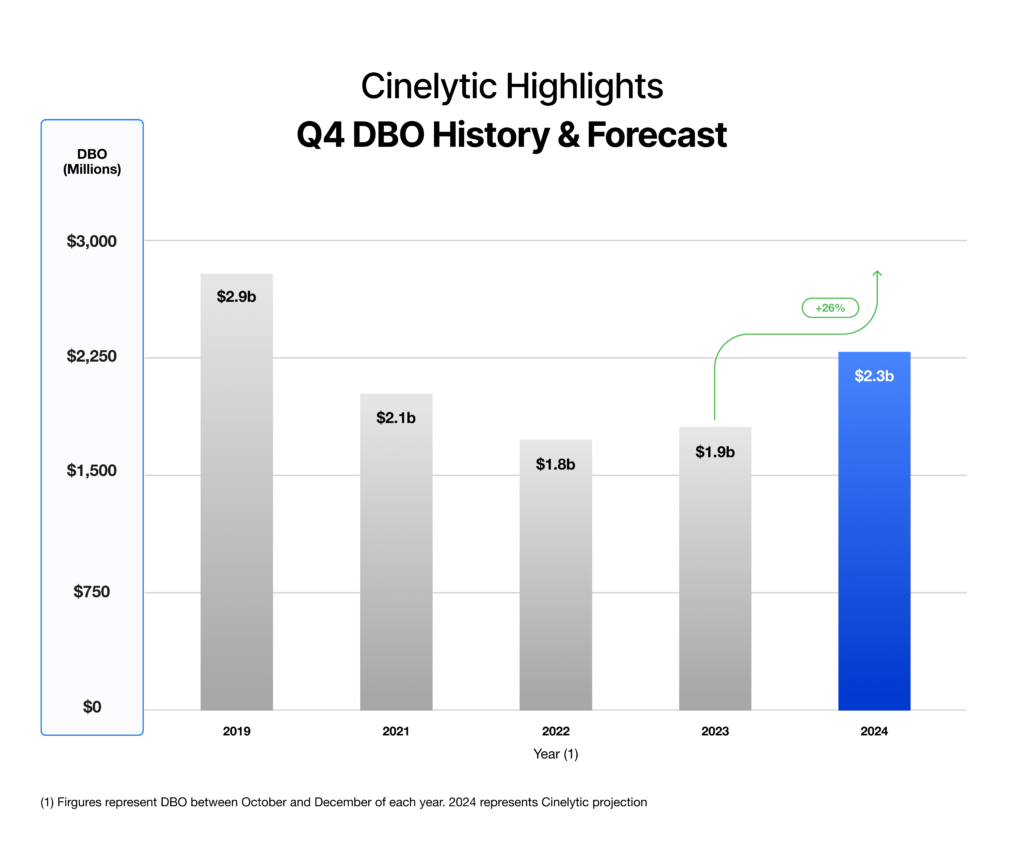

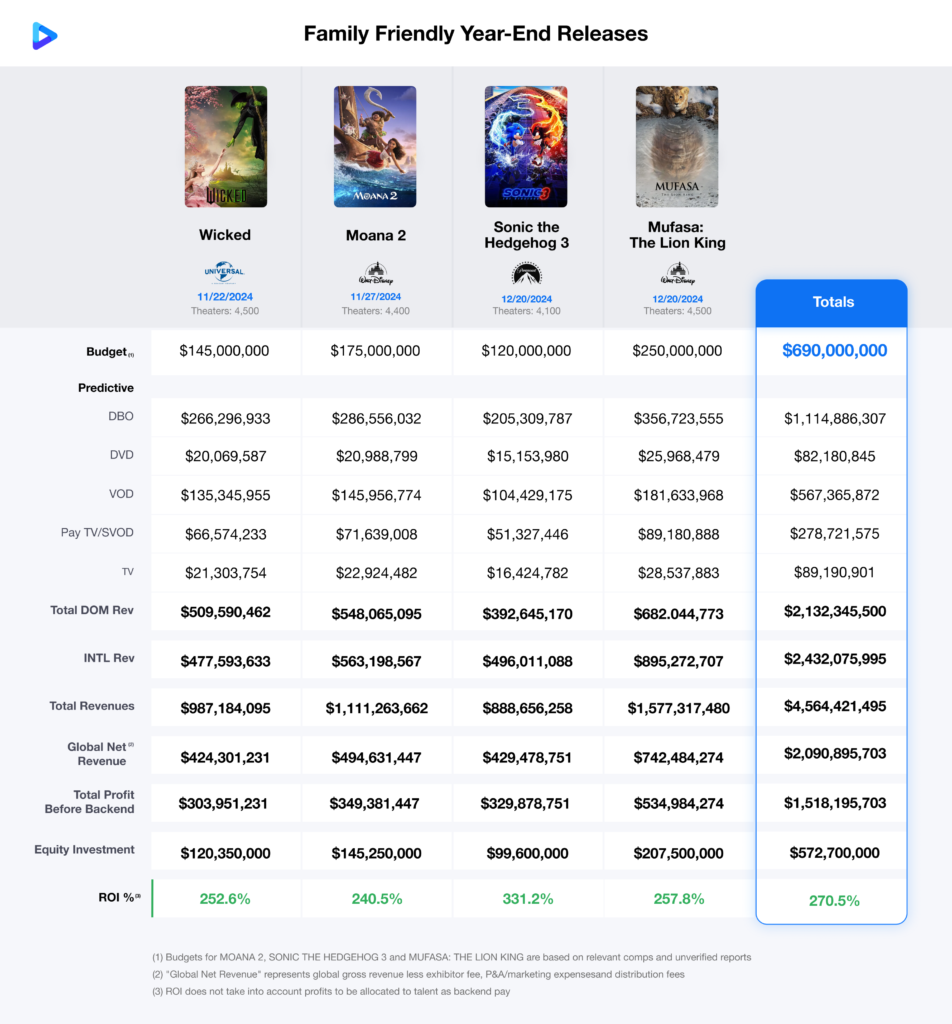

Last year’s Q4 was anchored by four major family-friendly releases—WICKED, MOANA 2, SONIC THE HEDGEHOG 3, and MUFASA: THE LION KING—all based on well-known IP. This year’s slate shifts slightly, with an equal balance of family-oriented titles with large-scale sci-fi action, each one a sequel: TRON: ARES, WICKED: FOR GOOD, ZOOTOPIA 2, and AVATAR: FIRE AND ASH.

These conclusions stem from running the 2025 Q4 slate through Cinelytic’s predictive forecasting platform, which leverages AI and 19 key attributes to model box office performance and ROI. For a closer look at the individual projections, the graphic below highlights these four upcoming releases and offers insight into why they are well-positioned to drive a strong Q4 finish:

TRON: ARES is projected to deliver an ROI of 16% before talent backend payouts, the lowest among the titles we analyzed. The film’s estimated budget is high, and despite its nostalgic appeal, large-scale visuals, and ambitious world-building, the franchise lacks strong recognition with modern audiences—the last film released 15 years ago to only modest critical and financial results. Lead star Jared Leto also has not been consistently tied to box office hits, potentially resulting in further limitations to the film’s draw.

WICKED: FOR GOOD ranked third in our projections but still carries a highly promising and lucrative ROI outlook at 392%. The film is almost certain to be a major success, even if it doesn’t quite match the cultural phenomenon of its predecessor.

Its prospects are supported by the enduring popularity of the original, the short gap between releases, Thanksgiving weekend boost, and the franchise’s broad family-friendly appeal coupled with the kind of in-theater spectacle that continues to drive strong turnout.

In the top spot is another title poised to take advantage of Thanksgiving. ZOOTOPIA 2 is expected to enjoy robust success and an ROI of 524% despite the nine-year gap since the original film’s release. The first installment remains one of Disney Animation’s most acclaimed and highest-grossing titles, with characters and themes that continue to resonate across demographics.

The sequel benefits from built-in family appeal, an active merchandising and streaming presence, and broad four-quadrant reach that positions it as a holiday season favorite. Adding to its potential, 2025 has yet to produce a breakout hit in a fully animated title, further boosting the appeal of a proven IP for family-oriented audiences.

And finally, we come to what is far and away the most prominent holiday release. AVATAR: FIRE AND ASH represents the third installment in James Cameron’s record-breaking franchise, one that already claims two of the top three highest-grossing films in history.

Even if this entry falls short of matching its predecessors, it is still positioned to be this year’s top-earning release at the box office with a projected ROI of 484%, and another likely addition to the upper tier of the all-time rankings for James Cameron. With its established global fan base, reputation for groundbreaking visuals and immersive world-building, and the proven draw of the AVATAR brand as a theatrical event, the film is expected to dominate the box office in late 2025 and early 2026.

All to Say… Taken together, these projections reinforce both the stability and the challenges of today’s theatrical market. While overall growth remains modest compared to pre-pandemic highs, franchise-driven releases anchored in well-known IP are still capable of providing reliable returns and draw audiences back to theaters. As the year closes, the four titles we analyzed here are set to define the quarter, with Disney once again leading the charge and Cinelytic’s platform demonstrating the value of data-driven forecasting in navigating an evolving box office landscape.

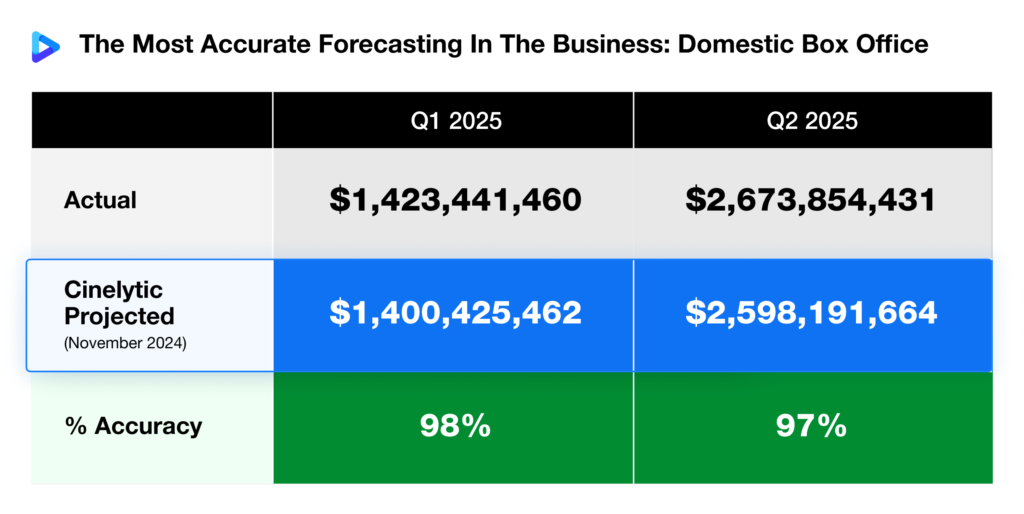

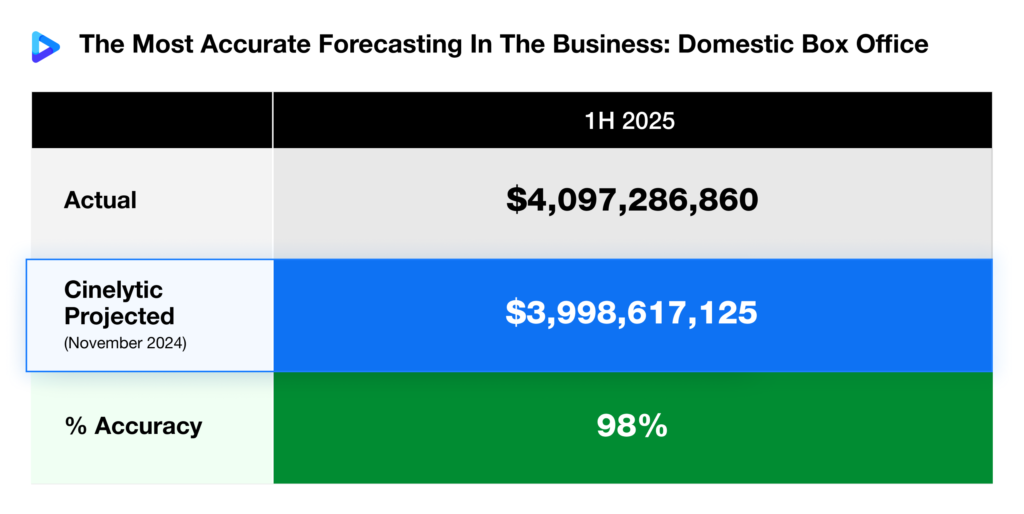

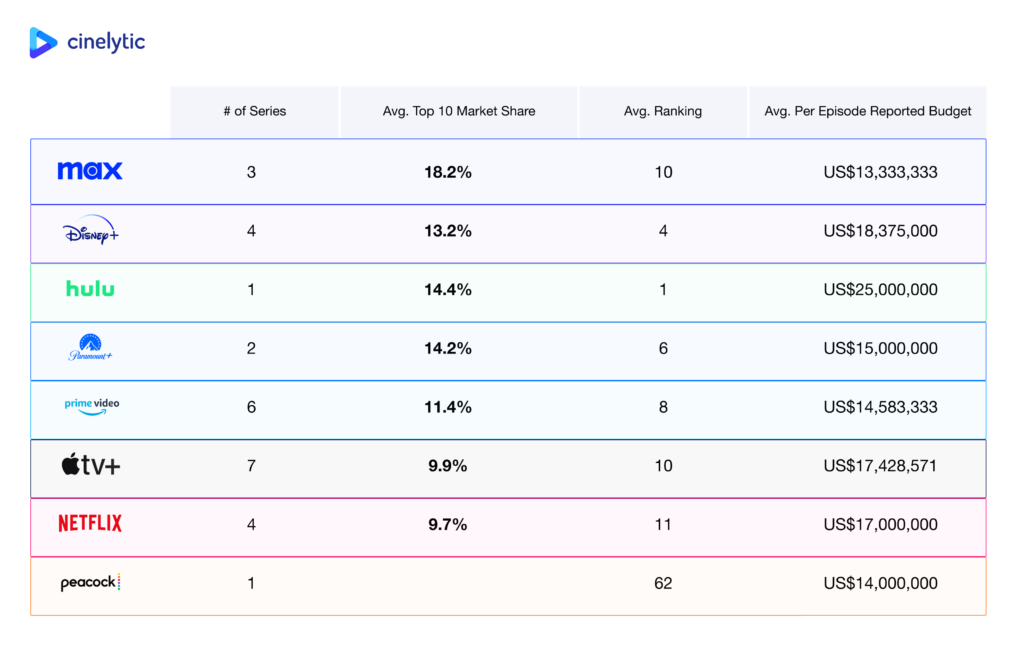

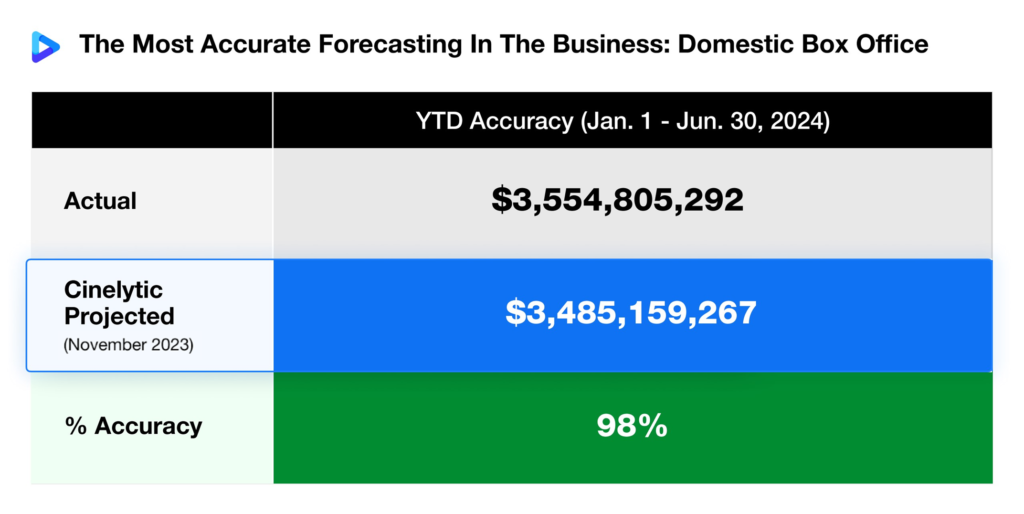

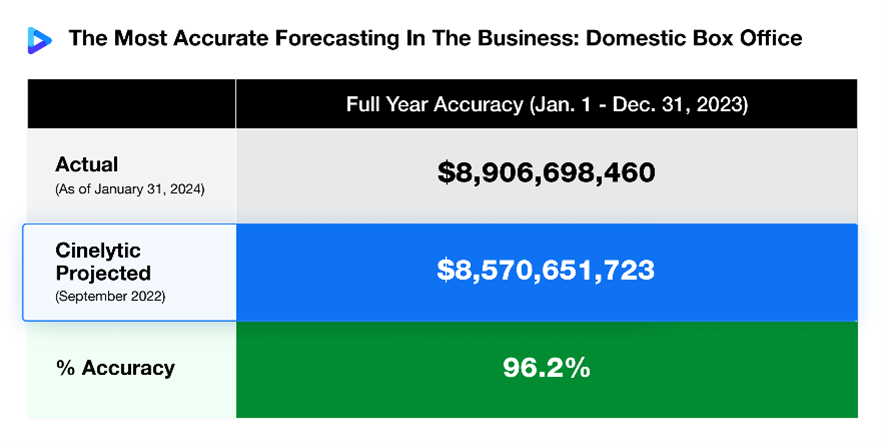

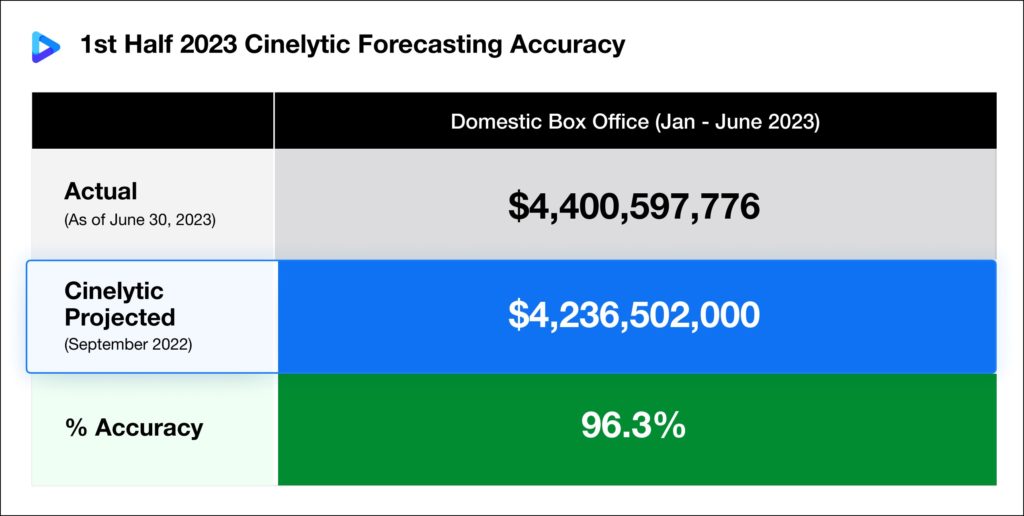

Throughout the year, Cinelytic has been closely monitoring the projections we released in November 2024 for the entire 2025 slate, where we estimated a total domestic gross of US$9.35b.

Our early prediction model not only projects box office revenue but also forecasts home video and TV earnings, providing a valuable resource for the film industry.

As illustrated in the graphic below, our first-half accuracy stands at an impressive 98%—a level of precision that underscores the value of data-driven decision-making:

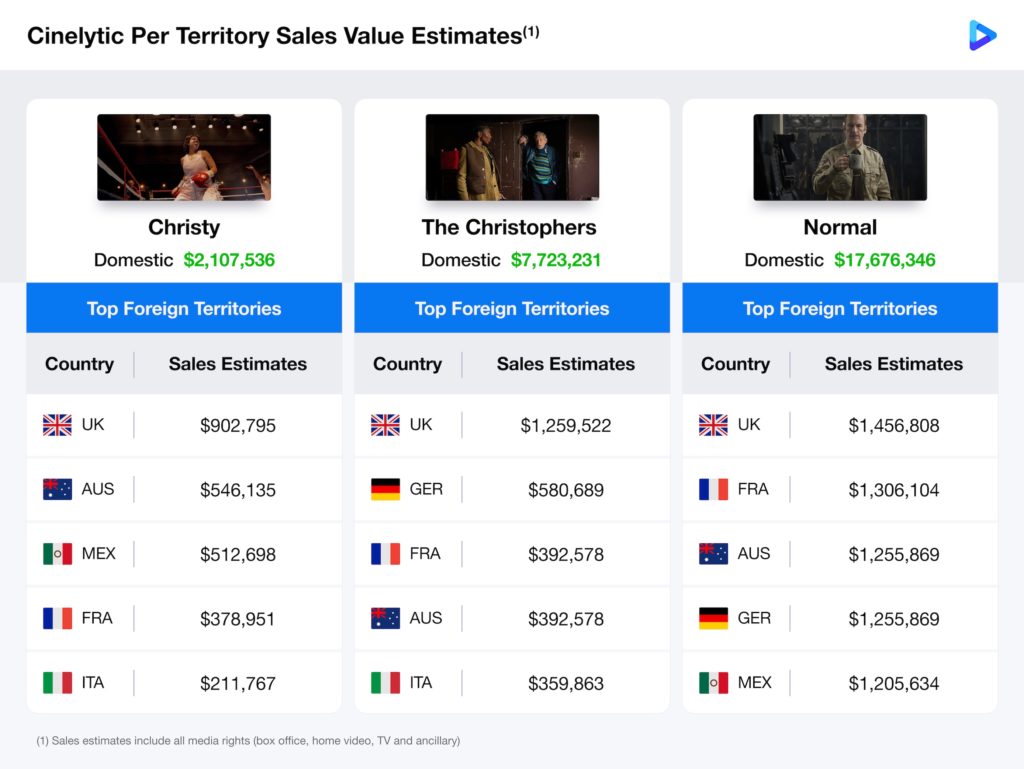

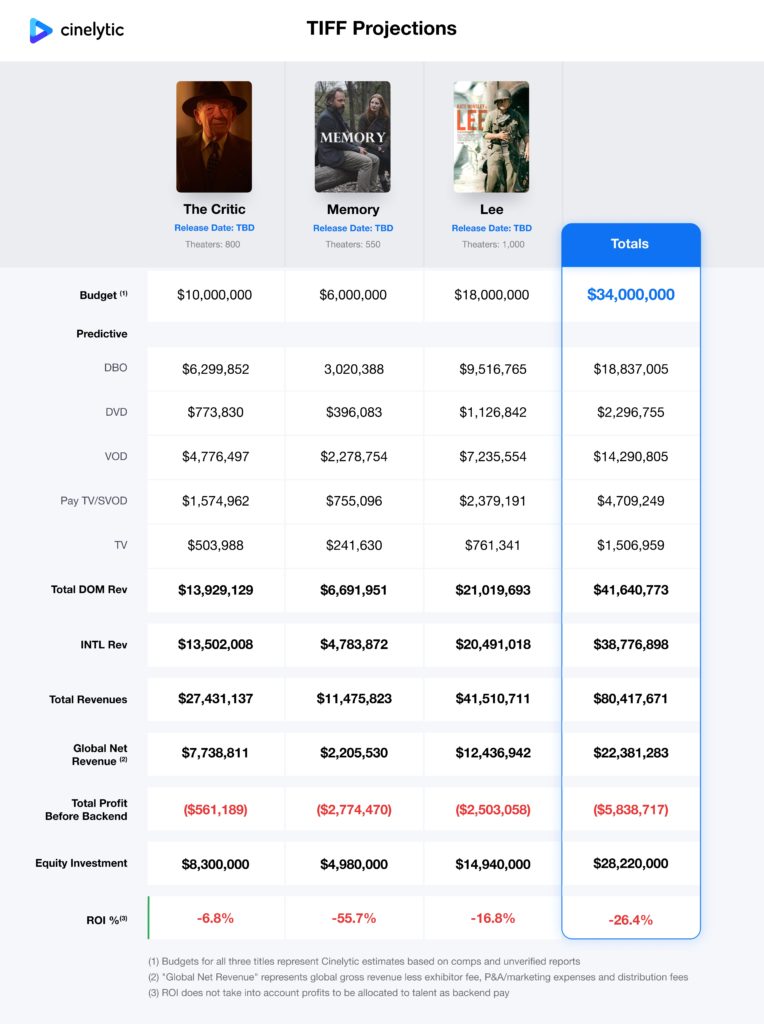

With the 50th annual Toronto International Film Festival (TIFF) just around the corner, we at Cinelytic are again putting our forecasting tools to work, this time spotlighting several upcoming releases attracting attention on the festival circuit as “hot sales titles” seeking US distribution at this year’s ceremonies: CHRISTY, THE CHRISTOPHERS, and NORMAL.

Our signature ROI forecasting, discussed later in these Insights, is particularly valuable for financiers, producers, and equity providers.

However, our sales estimates tool offers a different advantage that enables both buyers and sellers at festivals like TIFF to assess the per-territory value of a title across all media rights (box office, home video, TV, and ancillary).

As shown in the graphic below, this tool is especially useful for those in a market setting who are working to determine the appropriate price for each territory’s rights:

From acclaimed director David Michôd, CHRISTY is a biopic period sports drama starring Sydney Sweeney. Combining Michôd’s signature intensity with Sweeney’s rising star power, the film is positioned as one of the most closely watched titles of the festival.

Veteran filmmaker Steven Soderbergh returns with THE CHRISTOPHERS, a dark comedy expected to draw significant critical and commercial attention. Known for blending sharp storytelling with innovative production approaches, Soderbergh’s latest is already generating strong market interest.

The final intriguing upcoming projec is NORMAL, starring Bob Odenkirk and coming courtesy of the screenwriting and production team behind the JOHN WICK and NOBODY action franchises. With a mix of familiar creative DNA and Odenkirk’s proven versatility, the project has generated early buzz among buyers and audiences alike.

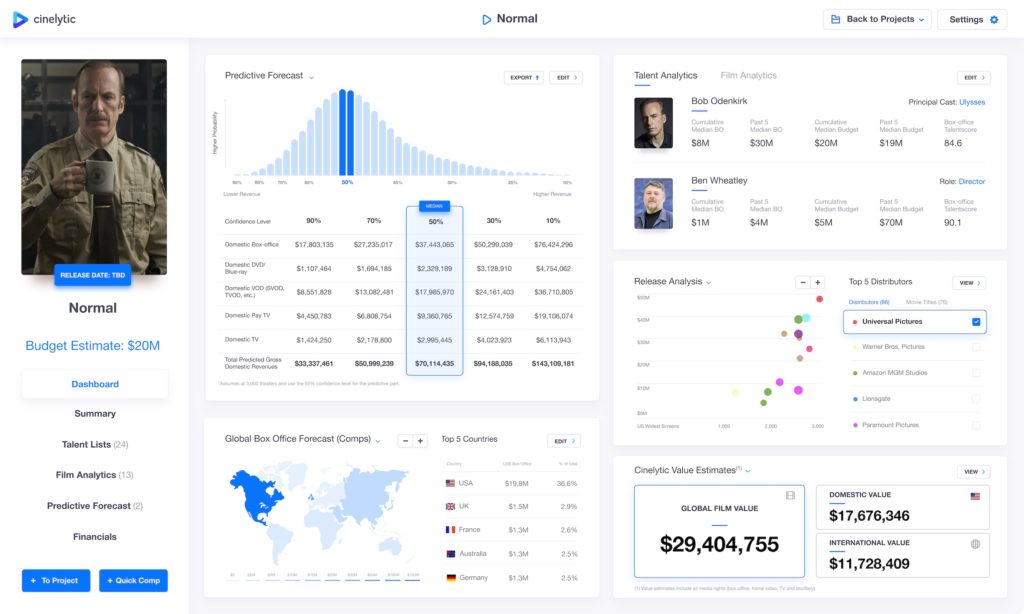

Revenue Forecasting: Spotlight – NORMAL

In order to provide sample of our detailed projections, we chose to highlight NORMAL and run it through our predictive tool to showcase what may lie ahead for these types of releases in terms of revenue.

This tool takes into consideration 19 material input attributes to determine a full-performance waterfall, P&L and ROI. We estimated a budget of US$20m, an additional US$43m in total P&A costs and proposed a theatrical release strategy of 3,000 screens with Bob Odenkirk in the lead.

The Cinelytic platform predicts a DBO of roughly US$37.4m, domestic gross revenues (BO, HV, TV) that total US$70.1m, and international gross revenues totaling US$43.6m:

Based on the anticipated global net revenues (including BO, HE, TV net of distribution fees and expenses), the film is expected to yield an ROI of 77.1% before the talent back-end, which can be substantial.

Streaming Success?

Box office potential is no longer the only driver of sales negotiations at festivals such as TIFF. With streaming platforms (VOD and SVOD) now serving as a major revenue source for festival titles, the focus has shifted toward understanding and analyzing audience consumption patterns.

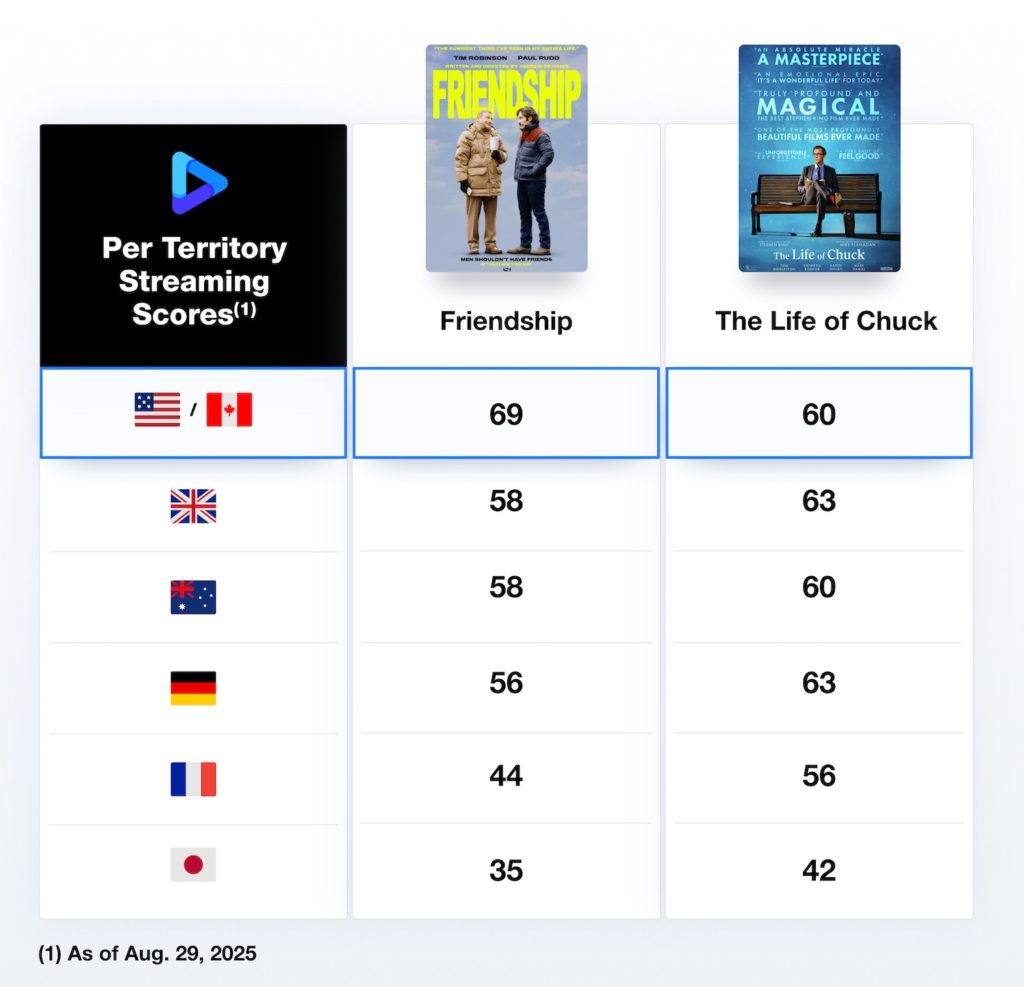

Specifically, we examined both the domestic and international streaming performance of two films that gained significant sales attention at last year’s TIFF: FRIENDSHIP and THE LIFE OF CHUCK.

To do this, we utilized our innovative “Cinelytic Streaming Store,” which illustrates digital content consumption on a per-title basis across various platforms and countries, offering valuable insights through a proprietary viewing score.

The graphic above shows that on streaming FRIENDSHIP performed strongest domestically, with the UK and Australia emerging as its next strongest territories. In contrast, THE LIFE OF CHUCK led in both the UK and Germany, with domestic performance close behind. Across most other major territories both titles maintained solid performance, though Japan remained a clear weak spot for each.

In terms of box office performance, FRIENDSHIP came out on top by a wide margin, grossing over US$16.2m in DBO, while THE LIFE OF CHUCK brought in just US$6.7m.

FRIENDSHIP’s comparative superiority regarding both theatrical and digital performance possibly came from its awkward but affectionate tone and strong word of mouth, paired with a breakout performance by niche TV star Tim Robinson.

The film opened in only six theaters with an average of US$75,000 per screen, making it the highest-grossing limited release of 2025, and it expanded with momentum into broader markets as audiences connected with its quirky and heartfelt take on adult male bonding.

THE LIFE OF CHUCK followed a very different trajectory. Although it won the People’s Choice Award at TIFF 2024 and drew consistent praise for its emotional storytelling, the release was caught between larger titles and could not generate comparable commercial energy.

All to Say…

Forecasting the performance of feature films will never be an exact science, but Cinelytic provides the tools to make decisions with far greater clarity and confidence. At TIFF 2025, projects such as CHRISTY, THE CHRISTOPHERS, and NORMAL highlight how each film presents distinct opportunities and challenges when it comes to release strategy. Our platform helps define the right valuation for a title while also optimizing P&A spend and distribution approach.

When these elements are aligned, the path to a stronger ROI becomes far more achievable. Whether the release strategy points toward a wide theatrical rollout or a direct-to-home debut, Cinelytic reduces the uncertainty by equipping industry players with reliable analytics and actionable business insights.

While it came as little surprise to us at Cinelytic based on projections made at the end of last year, domestic box office (DBO) performance in the first half of 2025 exceeded that of the same period in 2024, marking a 15% increase in theatrical revenue.

As has become increasingly common in today’s market, several major and high-budget releases including CAPTAIN AMERICA: BRAVE NEW WORLD, THUNDERBOLTS*, SNOW WHITE, and MISSION IMPOSSIBLE – THE FINAL RECKONING underperformed despite strong genre appeal, recognizable IP, large scale production, and star-powered casts.

Interestingly, some of these titles have gone on to find renewed success in the home entertainment market, a trend we’ll explore further in this edition of Insights.

Conversely, titles such as A MINECRAFT MOVIE, LILO AND STITCH, SINNERS, and FINAL DESTINATION BLOODLINES have delivered strong results at the box office. As we look ahead to the second half of the year, a steady stream of high-profile releases promises to keep studios alert and competitive.

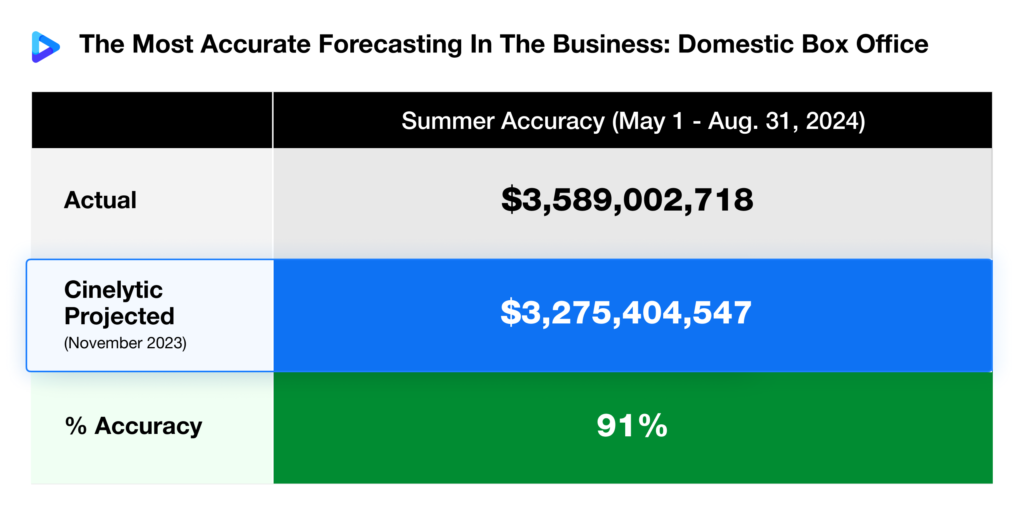

Fortunately, studios now have access to tools that can mitigate risk during green lighting. Using our predictive analytics platform, Cinelytic projected the entire 2025 film slate back in November 2024, estimating a total domestic gross of US$9.35b.

This early forecasting model enables accurate predictions not just for domestic and global box office, but also for home entertainment and television revenues, offering the industry a powerful and multifaceted decision-making tool. As the graphic below illustrates, our projections for the first half of the year have proven remarkably accurate:

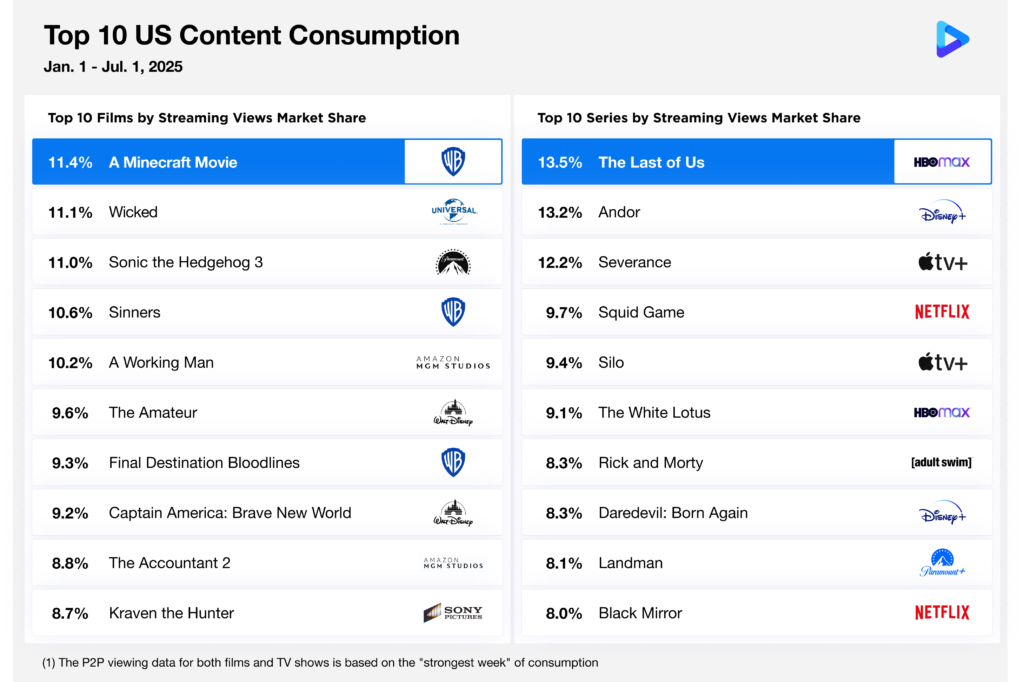

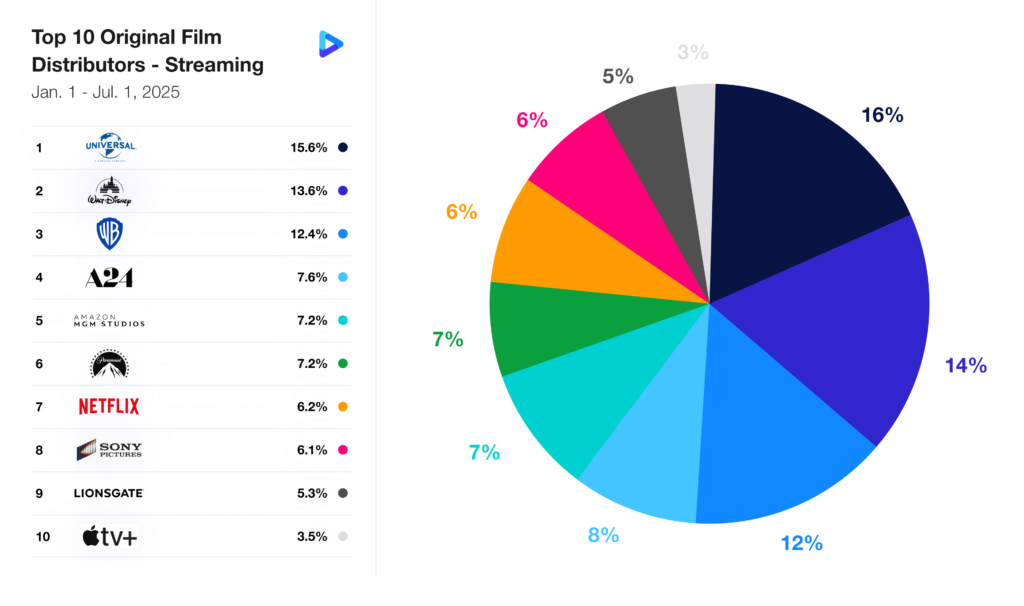

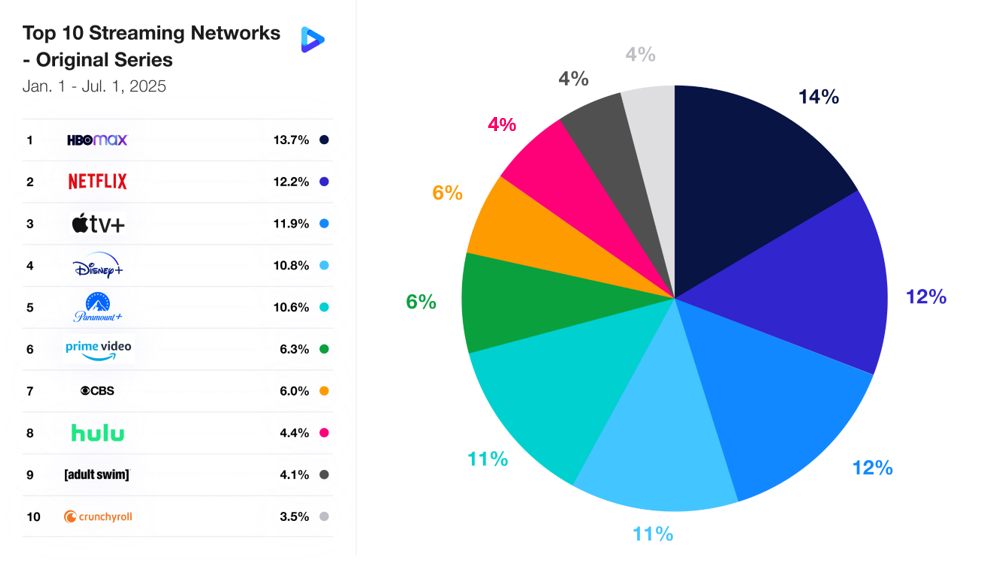

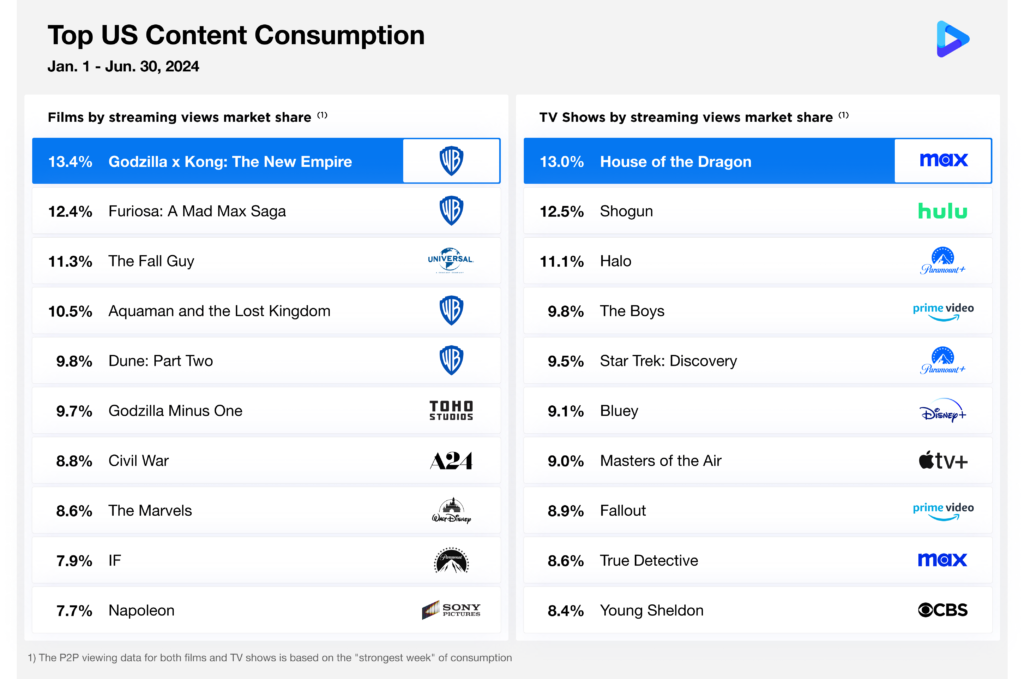

There have been some surprising films that contributed to this US$4.0b, along with varying degrees of follow up success on streaming. In the graphic below, we evaluated and compared the streaming performance of both films and TV series in 2025 using our proprietary OTT demand data.

This data captures 125m digital content consumption transactions per day across the world, aggregating to an annual total of 35b, illustrating consumer IP and content preferences on a global scale. For this exercise, we ranked the Top 10 most viewed movies and TV series through the end of June of this year.